Most investors with a fundamental bent focus on the income statement. We want to know how fast a company is growing, what its margins are and how much money it’s making. This makes perfect sense.

But the income statement consists of a number of accounting estimates – most importantly depreciation. This is an estimate of the cost to place on the wear and tear on capital equipment used in production. It’s not a cash number.

Capital expenditures are depreciated over time as rather than expensed immediately. This is completely appropriate as fully expensing capital expenditures when they are made would result in lumpy earnings and not accurately reflect the nature of the expenditure.

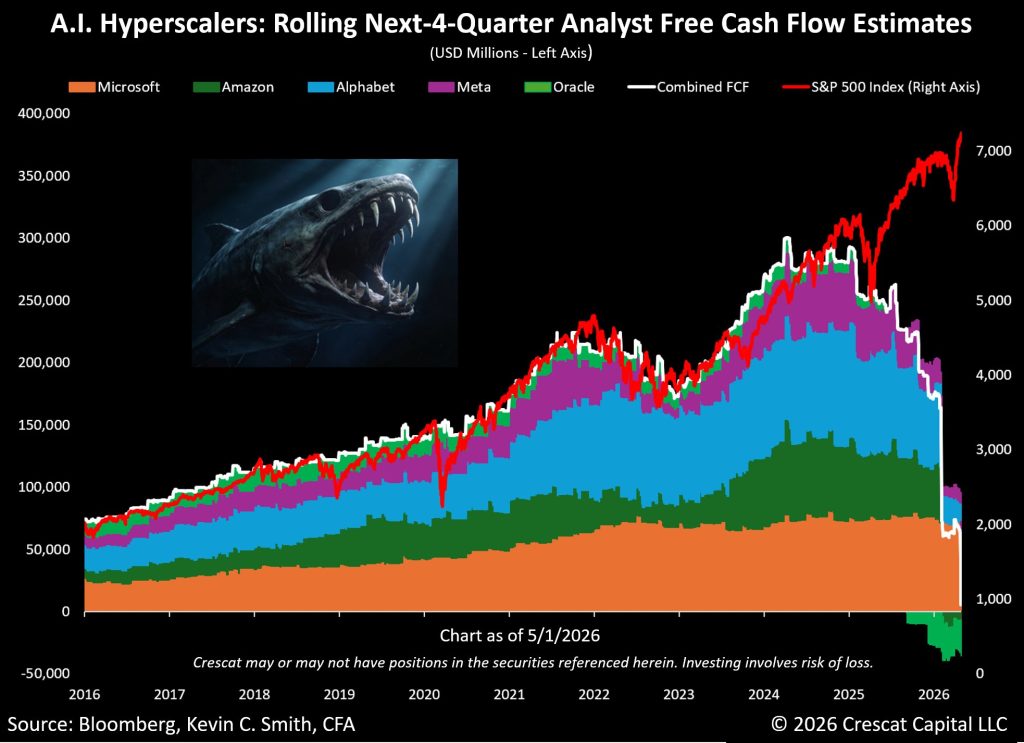

However, in a time of enormous capital expenditure to build out the infrastructure for AI, the income statement provides an especially incomplete picture of the business.

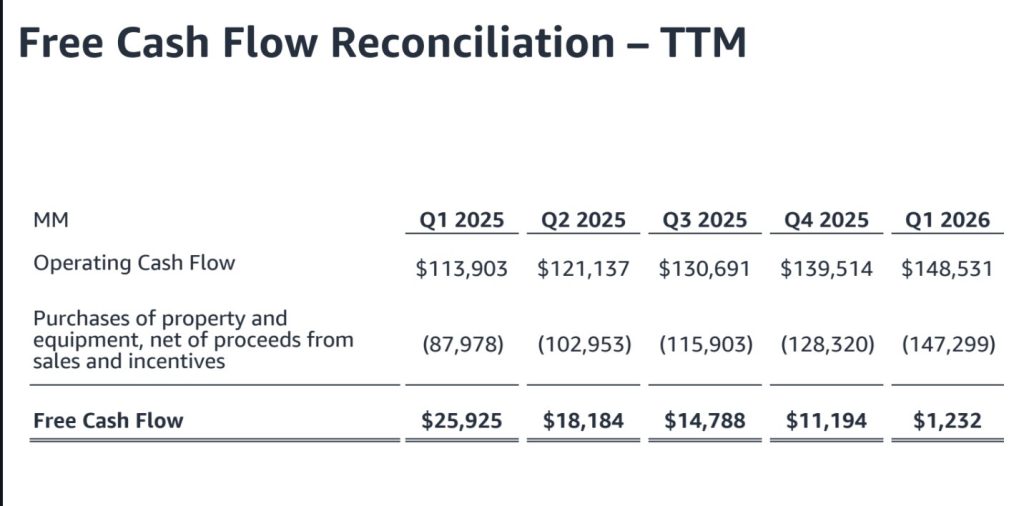

Take Amazon for example. AMZN just reported one of the best quarters in its history: Revenue was +17%, Operating Margin 13.1% and EPS $2.78. Operating Margin and EPS were the best in the company’s entire history. The retail business and AWS are both firing on all cylinders. If you only looked at the income statement, it would be difficult to find anything to worry about.

But what the income statement doesn’t tell you is that all of this money is currently going to capital expenditures to build out AI. AMZN’s CapEx in the quarter was $44 billion and they are guiding full year CapEx to $200 billion. For perspective, AMZN’s net income for all of 2025 was $78 billion. In other words, AMZN is making an enormous bet.

This bet may well pay off with a massive return on investment down the road as CEO Andy Jassy told Jim Cramer on Mad Money Monday afternoon. But that’s to be determined.

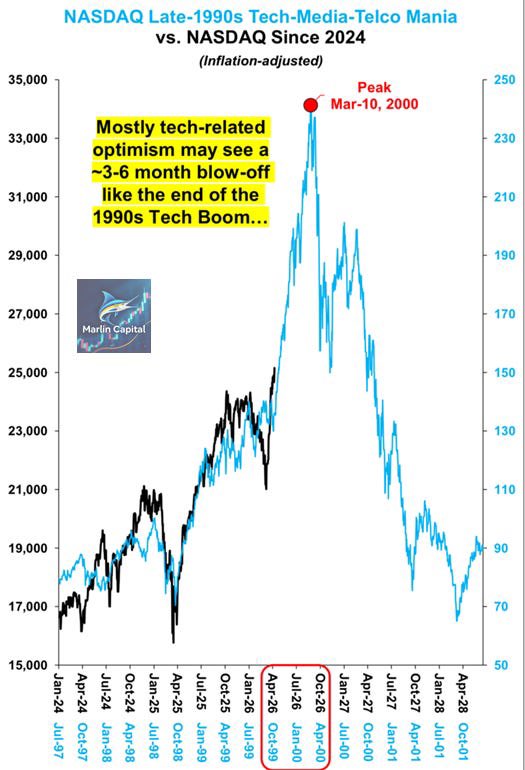

At the height of the Dot Com Bubble, the companies spending all that money to build out the infrastructure for the internet expected the same thing. While the internet ultimately did become a game changer, much of that initial CapEx turned out to be malinvestment and the companies who made it didn’t realize the ROI they expected. In fact, the massive amount of malinvestment tanked the entire economy and led to a nasty recession.

My concern is that we are seeing a repeat of that cycle today. While AMZN is investing the most aggressively among the hyperscalers, the same argument applies to each of them: GOOG, MSFT and META.

While the stock market can continue to surge higher as it did in the late 1990s, that doesn’t tell you if it’s a rational move based on fundamentals or a bubble. Perhaps we are on the verge of an age of unprecedented abundance ushered in by superhuman intelligent machines. On the other hand, this time might not be different.

Comments

Log in or sign up to join the conversation.