The household savings rate represents the proportion of personal disposable income that remains after spending.

We always expected the household savings rates in both countries to decline following the end of the global financial crisis more than a decade ago.

In other words, households in the US and Canada began feeling more secure and even wealthier as their economies recovered from the deep downturn, helped along by record low-interest rates.

Nonetheless, the savings rate in Canada recently declined to its lowest level in more than a decade, while the American savings rate remains considerably higher. As the following two charts illustrate, in the past, Americans used to save less that Canadians, but circumstances have dramatically changed.

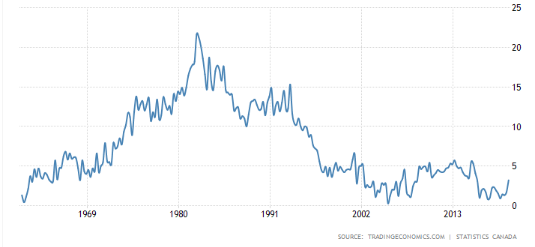

Canada’s household saving rate reached a 4-year high of 3.2% in the third quarter of 2019 from 1.7% in the previous quarter. But as the following chart illustrates, personal savings as a percent of disposable income has averaged much higher in the past.

Between 1961 and 2019, the Canadian savings rate averaged 7.59%, reaching an all-time high of 21.6% in the first quarter of 1982 and a record low of 0.3% in the first quarter of 2005. But over the past 25 years and longer, the basic trend was for a quite low savings rate.

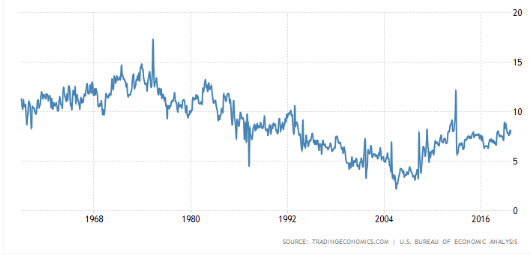

The current household saving rate in the United States is much higher than in Canada. The US saving rate was 7.8% in October compared to 8.1% in September of 2019.

It is interesting that despite considerable volatility in the savings rates in both countries, the longer-term US average was not much different than Canada’s.

According to Trading Economics, personal savings in the United States averaged 8.83% from 1959 until 2019, reaching an all-time high of 17.3% in May of 1975 and a record low of 2.2% in July of 2005.

There is possibly a scary implication in all of this for Canada’s economy going forward since the economy’s recent growth has been heavily dependent on consumer spending rather than business investment.

That is, in Canada, a low savings rate could signal that consumption-driven economic growth may be nearing an end.

As well, a low household savings rate also leaves Canadians more vulnerable to an economic shock and could signify that families aren’t building enough of a buffer for future bad times.

In conclusion, Canada’s low personal savings rate is a dilemma that is not going away.

Canada’s Household Personal Savings Rate

The US Personal Savings Rate

Comments

Log in or sign up to join the conversation.