Image Source: Pixabay

Introduction

Stock prices vacillate up and down. This price movement may be rooted in the company's fundamentals, the Street's sentiment, or as is often the case: a combination. The best investors do not focus on price: they focus on value. The value of equity represents what an investor believes it is worth based on intrinsic or theoretical value. Using fundamental inputs and methodologies, an investor can reasonably determine the Fair Value of a given security.

What Is Fair Value?

I define a stock's Fair Value to be the price whereby I am indifferent to owning it. My FVE is based on an assessment of the company's current and future valuation metrics. By definition, Fair Value is an interpretive judgment; though it's underpinned by data.

A Fair Value Estimate is not the same as evaluating whether a given company is fundamentally a good or bad business. That's a separate exercise.

Here's an analogy:

By most measures, a Lexus is a fine automobile. Many consider it a best-in-class vehicle. However, a Lexus is not a good value at any price. Let's say my Fair Value Estimate for a base Lexus ES350 is $40,000. If I was offered a brand-new base 2024 Lexus ES350 for $80,000, I would very likely walk away. If I was offered the exact same car for $20,000, I might ask if I could buy two. Indeed, the reverse is also true. If I kept my car tip-top and some guy offered me $50,000 for one of my $20,000 Lexus' a year after I bought it, there's a high probability I would sell.

This kind of thing happens on Wall Street every day.

How May I Determine Fair Value?

IMHO, this depends upon a few factors.

- within what stock sector or industry does the stock reside?

- what works? (this one seems simple, but I've seen many who get tripped up on it)

The process for determining the FVE for a stock is not a cookie-cutter exercise. In my experience, the majority of stocks may be valued using the basic toolkit. However, there are some general exceptions. These exceptions include:

- banks

- regulated utilities

- start ups

- extremely fast growers

- highly cyclical companies

This article focuses on the first category: bank stocks.

Note: While I believe using technical analysis may be helpful when attempting to determine price level support or resistance, this article concentrates on bread-and-butter fundamental valuation metrics.

Example: Bank of America

Let's look at determining the FVE for Bank of America (BAC). BoA just reported 4Q23 and FY2023 earnings last week, so there's up-to-date financial data available.

For banking stocks, here are three useful FVE indicators:

- historical price-and-earnings

- the Graham Number

- CAPM bank stock valuation formula

Notably, when generating FVEs for bank stocks, I do not rely upon GAAP cash flow or EBITDA. I believe it's best to consider value as a function of earnings, returns, and book value.

Historical Price-and-Earnings

Let's begin with two overarching investment philosophies. 1) Over time, price follows earnings, and 2) Over time, a stock reverts to its mean.

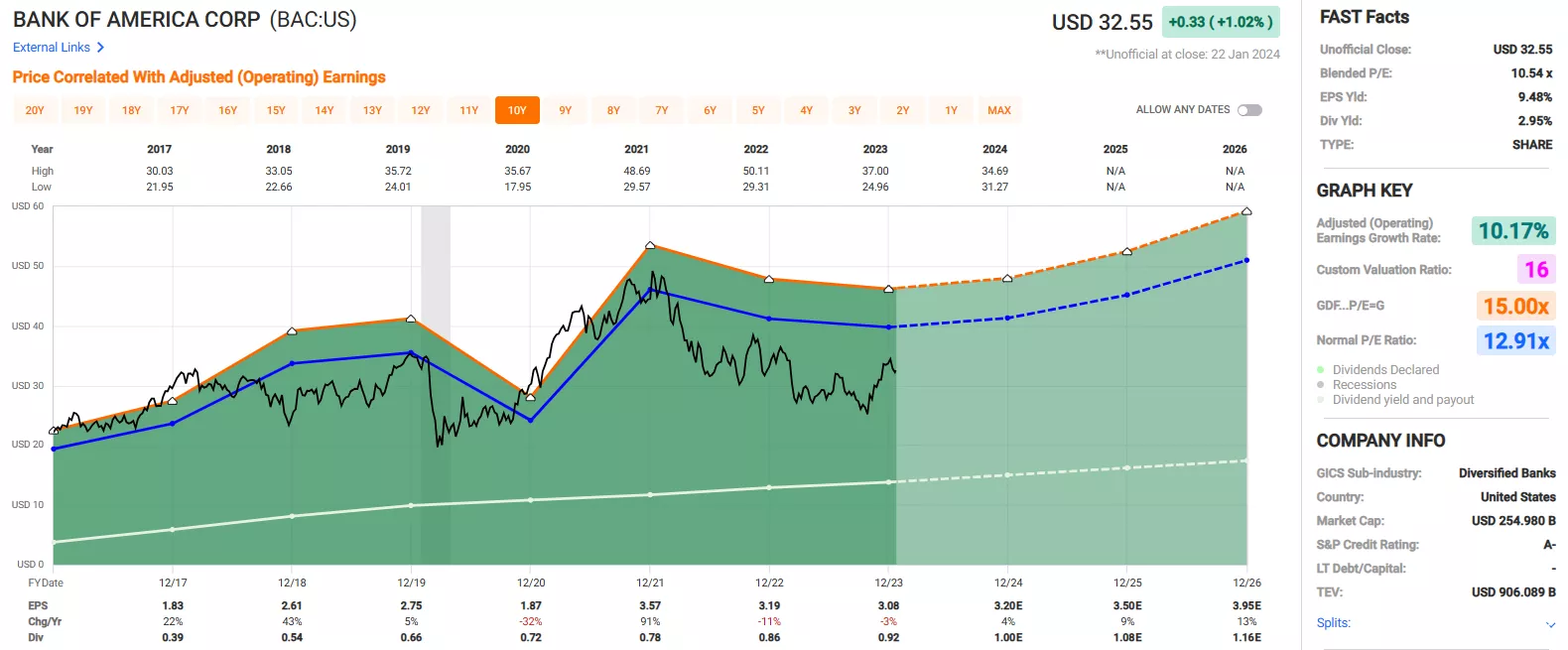

Let's begin by looking at a ten-year FAST graph illustrating Bank of America's stock price and earnings.

source: fastgraphs.com

In this case, after reviewing the long-term and medium-term charts, I utilized the ten-year chart indicating a trimmed average 13x P/E. While the stock price rises above and falls below PE13, over time it reverts to this mean.

Applying the current 2024 $3.20 EPS estimate to a 13x multiple, I obtain ~$42 FVE.

The Graham Number

The Graham Number (or Benjamin Graham's number) was created by Benjamin Graham, the godfather of fundamental investing. This formula measures a stock's fundamental value by taking into account the company's EPS and book value per share. Here is the formula:

![]()

grahamvalue.com

The Graham Number is the highest price an investor should pay for the stock. According to the theory, a stock price below the Graham Number is considered undervalued.

The formula represents a general valuation test when seeking to identify stocks that are currently selling for a good price. The 22.5 figure is included in the calculation to account for Graham's belief that the P/E ratio should not be over 15x and the BVPS (book value per share) should not be over 1.5x (thus, 15 x 1.5 = 22.5). Graham was a genius at providing investors with simple “rules of thumb” to boil down investment concepts into easy-to-understand nuggets.

From Graham's book, “The Intelligent Investor,” I offer you some additional parameters he referenced in conjunction with the formula:

- not less than $100 million of annual sales

- current assets should be at least twice current liabilities. (this may be interpreted for financial stocks)

- long-term debt should not exceed the net current assets

- some earnings for the common stock in each of the past 10 years

- uninterrupted dividend payments for at least the past 20 years

- minimum increase of at least one-third in per-share earnings in the past 10 years

- current price should not be more than 15 times average earnings of the past three years; therefore, the past three years' EPS should be averaged

- current price should not be more than 1½ times the book value.

Bank of America 3-year average EPS = $3.35

12/31/23 book value per share = $33.34

Running these inputs through the formula, the resultant FVE is ~$50.

Bank Stock Internal Valuation Formula

The third bank stock valuation methodology is one I've used for many years. I would like to introduce it to you.

Here is the workup:

A = Rf + b (Re – Rf)

then

B = RoTCE / A

then

FVE = B x TBV

where,

Rf is the risk-free return, usually the 10-year U.S. T-note

b is the beta for the bank stock

Re is the expected rate of return

RoTCE is the bank's return on tangible common equity

TBV is the bank's tangible book value per share

Here are the inputs for Bank of America:

Rf = 4.0%

b = 1.39

Re = 7%

RoTCE = 13.5% for FY2023

TBV = $24.46 as of 12/31/23

After inserting inputs into the formula, the resultant FVE = $41

Summary

Using P/E 13x and current 2024 EPS estimates, FVE $42

Using the Graham Formula, 3-year average EPS, FVE $50

Using the Bank Stock Internal Valuation Formula, FVE $41

Considering all the inputs and ancillary data, my current Bank of America Fair Value Estimate is ~$42.

A recent BAC bid is ~$33.60. Therefore, I believe the stock is significantly undervalued.

More By This Author:

"Buy When There's Hate In The Streets" - Interview

What Every Aflac Investor Needs To Know

Comments

Log in or sign up to join the conversation.