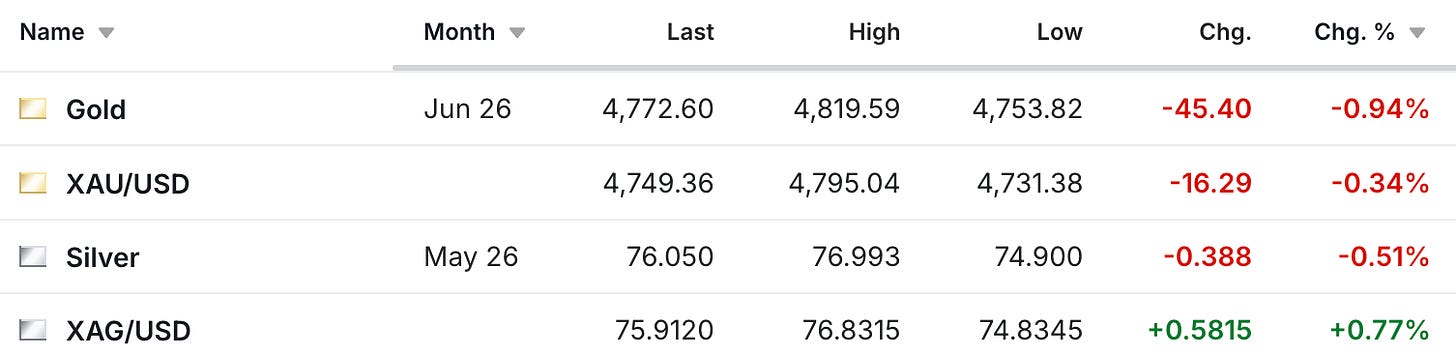

One of the more chaotic weeks I can remember in my lifetime ended with a somewhat quiet day in the gold and silver markets, as after everything that happened, amazingly, we’re right back where we started the week, with the Strait of Hormuz largely closed.

Which means that all of the issues that were a big concern last week are once again being magnified, although so far it seems as if the financial markets are sleepwalking through it.

Maybe it’s not entirely fair to phrase it that way. Perhaps the markets aren’t sleepwalking through it, but rather just exhausted trying to figure out what the world’s economic future looks like, which is going to be heavily impacted by what happens with the war. Yet at the moment, I don’t know that there’s anyone on the planet who really knows how this will all play out. And as a result, I think most investors are not in a rush to trade, and at this point are resigned to just waiting to see what develops next.

Metals Focus had a note out this week about the official sector gold sales that have taken place since the war began, which I found interesting given everything that’s currently taking place.

Gold prices have come under significant pressure following the US–Israel strikes on Iran. In addition to a rapid shift in US interest rate expectations, a pick-up in official sector sales and reports of potential further disposals have also weighed on investor sentiment.

The recent increase in central bank sales is likely to prove temporary. Indeed, even accounting for these sales, provisional data suggest that the official sector has remained a net bullion buyer this year-to-date. Elevated geopolitical risks should, if anything, reinforce the case for central banks to hold gold as a means of diversifying away from dollar-denominated assets.

That’s the same Metals Focus that compiles the data for the Silver Institute’s World Silver Survey, which will be released this coming Wednesday at 8:15 a.m. Eastern.

You can expect the reported deficit number to be substantially lower last year than in previous years. Although if you dig beneath the headline number, you’ll see that the deficit changes substantially when you factor in the ETFs (although their report refers to them as ETPs).

The other major change was that even though solar installations rose more than expected in 2025, heavy thrifting resulted in a lower amount of silver consumed than in 2024. But we’ll certainly go through the report more once it’s released.

So perhaps to wrap up a rather emotionally intensive week, I’ll reiterate what I’ve been saying ever since the sell-off began during the onset of the war, that as tragic as it is that once again the world only seems to be able to address its differences via conflict, I don’t know how much the ups and downs change the long-term outcome of what needs to happen to the gold and silver prices.

There’s still going to be the economic adjustment caused by AI, which will create some great productivity gains, but also necessitate a reshuffling in the composition of the labor force. And the necessity of reshoring manufacturing is being made even more apparent by the recent events in the Middle East, and that’s also going to require an increase in labor costs, as well as the increase in commodity pricing, to actually have the people and materials to rebuild our manufacturing sector.

Also, at the end of the day, just in case you needed to be reminded, you saw once again that no matter what the fiscal position, when the politicians decide they want war, more money gets spent. And if it ultimately comes down to the Fed monetizing the balance, that’s simply what they’re going to do.

You could also say that gold isn’t in a two-year rally, but is actually still in a 25-year rally. When you think about what’s happening, and what’s likely to happen in the years and decades ahead, there’s a darn good chance that the rally continues for the next 25 years, or even longer, unless humankind eventually figures out how to break the centuries-old pattern of governments spending more than they have, and resorting to inflating the balance.

So get some rest, take a break from the computer, and make sure to hug someone you love this weekend. The markets will be back open soon enough, and when they are, I’ll see you back here on Monday.

Comments

Log in or sign up to join the conversation.