Netflix (NFLX) granted Warner Bros. Discovery (WBD) a limited seven-day waiver, to allow it to reopen discussions with Paramount Skydance (PSKY) over its enhanced buyout bid for the movie studio and entertainment company.

This move comes after PSKY's hostile takeover attempt, which has intensified pressure on the pending $82.7 billion merger, including debt, between Netflix and WBD, announced late last year. For Netflix investors, who've watched their stock plummet over fears of ballooning debt from the acquisition, this could be a pivotal break. The deal would saddle Netflix with nearly $10 billion in assumed debt, raising concerns about financial strain in a competitive streaming landscape.

By permitting WBD to explore PSKY's new offer, Netflix may avoid a risky overcommitment, potentially preserving capital for growth initiatives like content expansion and ad-tier scaling.

The Competing Bids

Netflix's proposal focuses on acquiring only WBD's core assets: the iconic Warner Bros. movie studio, HBO Max streaming service, and related entertainment divisions, in an all-cash deal valued at $27.75 per share. This targeted approach allows Netflix to bolster its content library while avoiding WBD's linear TV networks, which are set to spin off as Discovery Global. The offer aims to create a streaming powerhouse, but it excludes WBD's cable-heavy operations.

In contrast, PSKY's aggressive bid targets the entire WBD company, offering $31 per share in an all-cash deal that includes a $1 per share termination fee to compensate for breaking the Netflix agreement. It also includes a "ticking fee," essentially a quarterly penalty if the deal drags beyond 2026, underscoring PSKY's commitment to a swift closure while covering the $2.8 billion breakup fee owed to Netflix.

Led by David Ellison's Skydance Media, PSKY envisions a merged entity with Paramount's assets, potentially creating synergies in film production and distribution. However, WBD's board has labeled PSKY's proposal deficient, citing financing uncertainties and regulatory risks that could lead to over-leveraging with $84 billion in pro forma debt.

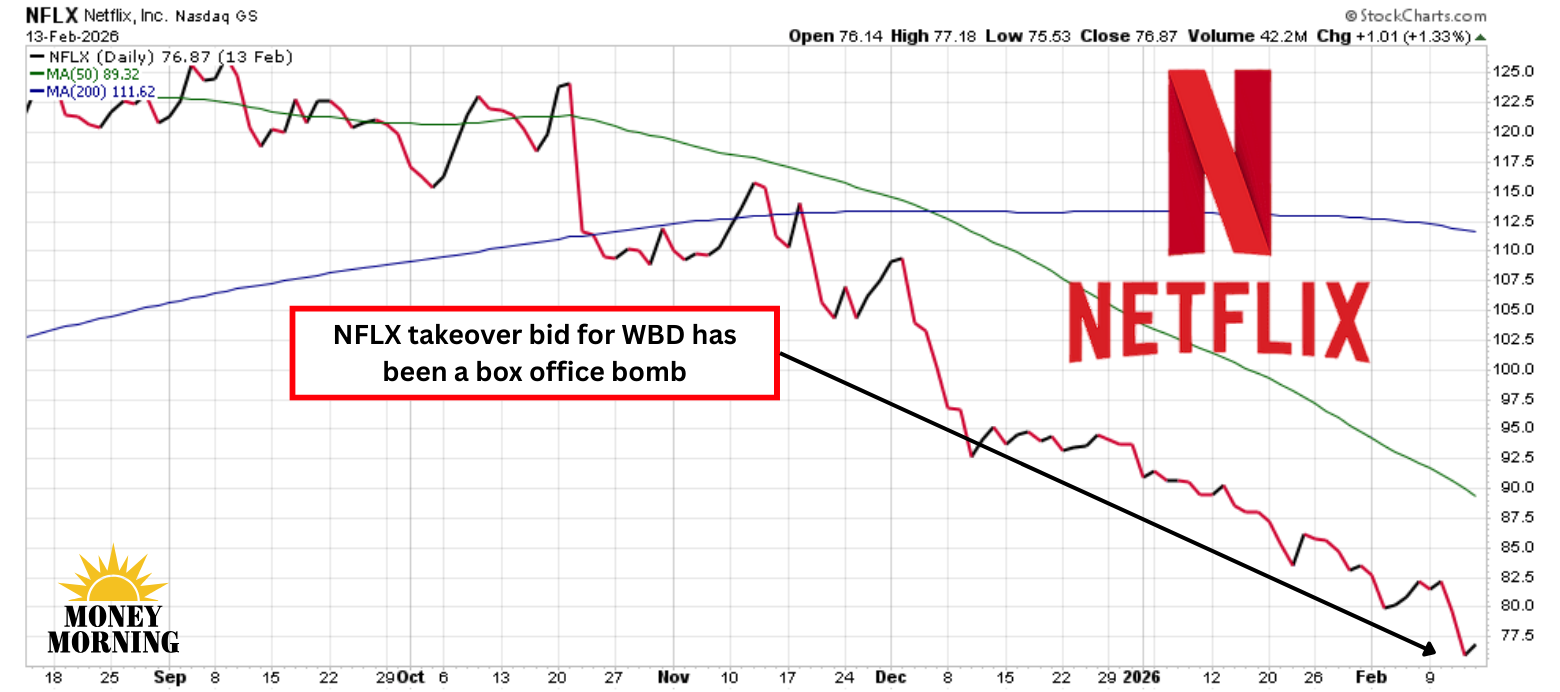

Investor Concerns and Market Reaction

The anxiety Netflix investors have stems from the merger's debt load, which could strain its balance sheet as subscriber growth slows and competition from Disney (DIS) and Amazon (AMZN) intensifies. Analysts worry that assuming $10 billion in obligations might limit investments in original content or international expansion, especially as Netflix's revenue growth tapered to 16% in 2025 despite hitting 325 million subscribers.

This has hammered NFLX stock, which has tumbled nearly 43% from its 2025 high of $133.91 per share. The decline reflects broader market skepticism about the deal's value, with shares dropping 16% in the past three weeks alone amid the takeover drama.

PSKY's assertion that its $31 per share offer isn't its "best and final" hints at room for sweetening the offer, possibly pushing the bid higher to sway WBD's board and shareholders ahead of the Mar. 20 vote. If increased sufficiently, it could prompt WBD to pivot, relieving Netflix from the acquisition's burdens and allowing investors to refocus on core strengths like ad-supported tiers and live events.

Bottom Line

Should WBD accept PSKY's offer, Netflix retains matching rights and will likely counter with a revised bid, perhaps aligning with PSKY's terms to secure the assets. This deal is far from sealed, with regulatory scrutiny and financing hurdles looming.

Yet, with PSKY's camel putting its nose under the tent, it might force a reevaluation, offering Netflix investors the salvation they've been looking for.

Comments

Log in or sign up to join the conversation.