When it rains it pours for Valeant VRX. CVS CVS and Express Scripts ESRX dropped Philidor from their pharmacy networks due to noncompliance with provider agreements. Valeant promptly cut ties with Philidor, citing a loss of confidence in the specialty pharmacy group's ability to operate in a manner acceptable to patients and doctors. Now Standard & Poor's has lowered the company's credit rating to "B+" from "BB-" with a negative outlook:

Valeant severed ties with its affiliate, specialty pharmacy network Philidor RX Services, after leading pharmacy benefit managers ("PBMs") terminated their relationships with Philidor ... We view the abrupt nature of this separation as likely to exacerbate the loss of revenues and profits we already anticipated from the reduced visibility of that channel.

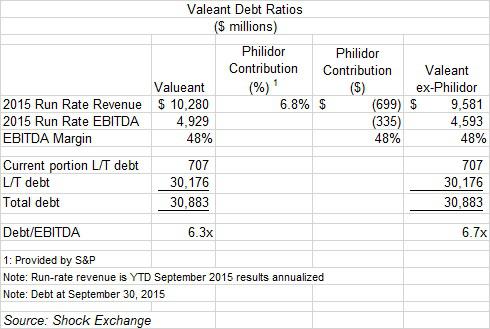

While this channel represents only a modest amount of Valeant's revenues (6.8% of its third quarter revenues), we believe these developments further harm Valeant's already tarnished reputation. We believe this could compromise the company's ability to effectively market its products to doctors through its sales force. We also believe these developments further increase potential legal, regulatory, and reputational risks to the company.

The Situation

Last week short seller Citron Research questioned if Valeant was stuffing its Philidor distribution channel with invoices to deceive auditors and book revenue. The smoking gun appeared after the Wall Street Journal divulged Philidor's aggressive sales practices. Such practices included Philidor's use of another pharmacy's identification number in order to get an insurer to reimburse claims. This information set off a chain of events that led to major pharmacy benefit managers and ultimately, Valeant, cutting ties with Philidor.

Valeant has grown its operations by acquiring drug makers and raising target companies' drug portfolios to prices that Valeant thinks the market would bear. The current loss of its reputation due to the Philidor debacle could prompt doctors and/or pharmacies to tamp down the use of its products. Secondly, politicians have looked askance on Valeant's practice of raising drug prices. Historically, drug companies have justified price increases in order to recoup R&D costs needed to launch drugs. Lastly, with its debt considered "highly speculative" by S&P, Valeant may find the debt markets closed to it; thus, its strategy of employing debt for acquisitions could be null and void.

Despite the potential for Valeant to lose revenue and earnings, its $32 billion in debt still needs to be repaid.

The above chart highlights the company's debt ratios. Based on run-rate EBITDA of $4.9 billion, the company's $31 billion debt is as 6.3x run-rate EBITDA. This would be considered "junk" levels by the rating agencies.

- Run-rate revenue and EBITDA are based on results through year-to-date September 30, 2015, and annualized. EBITDA was calculated based on [i] operating income, plus [ii] add backs for depreciation & amortization, restructuring costs, in process R&D impairments and other expense (income).

- Debt is at September 30, 2015.

- The Philidor contribution to revenue of 5.9% was derived from the Financial Times. For Q3 2015 6.8% of Valeant revenue was derived from products distributed through Philidor. However, since January about 5.9% was distributed through Philidor.

- I assumed Philidor also represented 5.9% of the company run-rate EBITDA, and it would go away once the company cut ties with Philidor.

If revenue and EBITDA generated by products sold through Philidor do not return, the company's debt/run-rate EBITDA would be at about 6.7x. Revenue and EBITDA could deteriorate further if doctors or pharmacies are reticent to prescribe Valeant products due to its loss of reputation in the marketplace. This scenario represents the "perfect storm" for Valeant. It amassed $31 billion in debt for acquisitions. The cash flow generated from those acquired companies could fall sharply, yet the debt still has to be repaid.

We have seen the "perfect storm" play out with Molycorp (OTCPK:MCPIQ), and now with Weatherford (NYSE:WFT). Molycorp raised debt to fund the $1.2 billion acquisition of Neo Materials Technologies. Shortly thereafter, rare earth prices tumbled. Molycorp defaulted on its debt and is eventually went bankrupt. Weatherford has amassed $7.7 billion in debt for acquisitions in the oilfield services space. Now that oil prices are 60% off their 2014 peak and oil & gas E&P has been cut, Weatherford's debt has been junked by Moody's.

Conclusion

The potential loss of revenue and EBITDA represented by products sold through Philidor could come at an inopportune time. If the company loses additional revenue and earnings due to the diminution of its reputation amongst doctors and pharmacies, its $31 billion debt load could become untenable. Principal repayments of $1 billion are due through 2016. After that, I believe the company could have trouble making principal and interest payments. Avoid VRX.

Comments

Log in or sign up to join the conversation.