Market Analysis

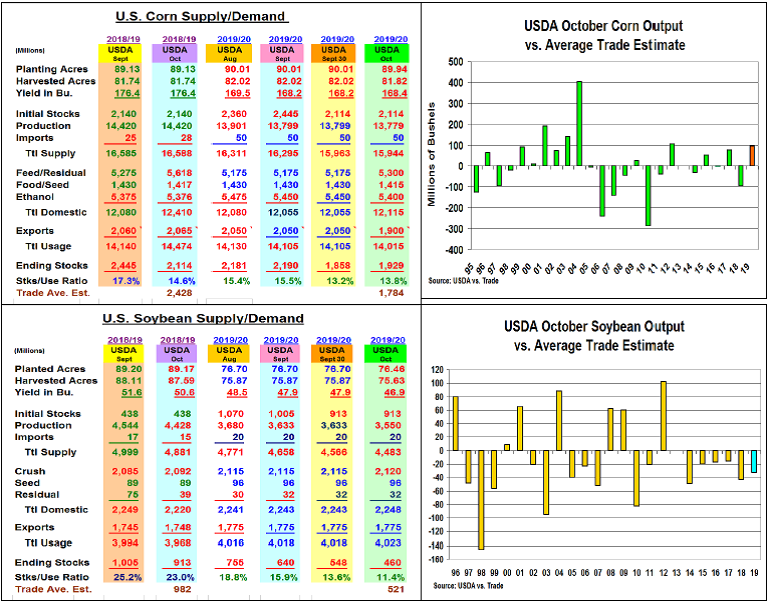

The USDA again provided some curves in this month’s crop report. US corn output was higher than expected while beans were lower than expected. Given 2019’s early country reports & limited US harvest progress through Oct 6th (15% - corn/14% - beans), smaller outputs were expected. Corn’s 0.2 bu. higher yield and 20 million smaller 2019 crop became the dominant-negative factor despite beans 1 bu. lower yield vs last month. The USDA’s aggressive demand cuts in both corn and wheat balance sheets added to the grains weakness despite the nasty winter storm impacting the N. Central US currently.

With the trade expecting 115 million bu smaller corn crop on a 0.7 bu lower yield & 368,000 smaller harvested area, October’s 13.779 billion bu crop was 95 million bu. higher than expected. This was the highest plus deviation since 2012. Yield increases across the US (MN, OH & TX +2 bu. and IA, IN, ND and KY +1 bu.) were behind this limited decline along with just a 202,000 smaller har-vested area vs. expectations. Lower exports because of 2019’s slow start & a larger feed/residual level after last month’s lower stocks were expected. But, slicing industrial demand 65 million bu (50 from ethanol) helped push corn’s stocks 145 million bu. over the trade average.

This month’s soybean yield was cut 1 bu to 46.9 bu, but October’s 240,000 smaller US harvested acres also helped shrink this crop’s output 83 million lower to 3.55 billion bu. This month’s 33 million lower output vs. the trade followed the previous 5 years trend of a smaller crop than trade average. This month’s smaller crop and beginning stocks reduce this year’s ending stocks to 460 million bu., 61 million bu below expectations.

Wheat’s US stocks were also upped by 29 million bu. to 1.043 billion this month. Despite 18 million lower Small Grains output, a 30 million cut in feed & 25 million bu. lower exports prompted these unexpected higher stocks.

(Click on image to enlarge)

What’s Ahead

Given this year’s erratic growing season weather and limited yield knowledge because of 2019’s delayed harvest, the market’s crop report reaction seems overdone. The current cold weather could reduce corn and bean crop sizes, but it will also slow dry down. This could potentially cause further field losses. Given these unknowns, hold for $3.95-$4.10 Dec and $9.40-50 Nov for your next 15% sale.

Comments

Log in or sign up to join the conversation.