Market Analysis

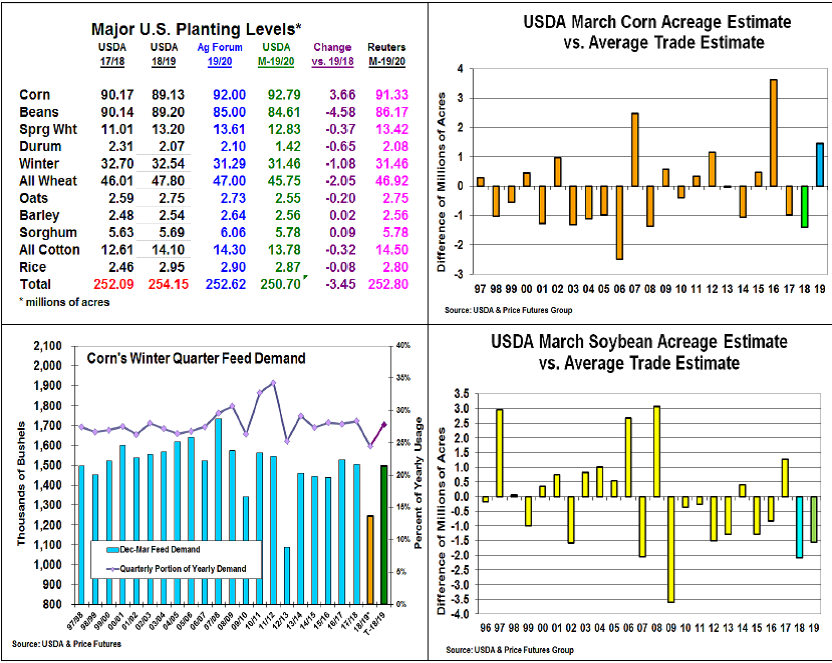

The USDA provided surprises in both US planting intentions & their quarterly stocks reports. Their producer survey revealed higher corn plantings & smaller soybean and spring wheat seedings than the trade expectations. Interestingly, corn’s 92.79 million acres were 1.46 million above the trade & 3.663 million above 2019. Higher seedings occurred across the Central US. Surprisingly, the Plains jumped their plantings by 1.95 million with ND +900,000 & SD +600,000. the big adjusters. From Iowa to Ohio planting rose just 750,000 vs. 2018. 2019’s soybean plantings were 1.55 million lower than estimates at 84.62 million acres (-4.58 million than 2018). Planting intentions were virtually lower across the US with the major Midwest states down 2.85 million acres (MN -500 mil-lion, IA -600, ND -400, SD -450 IL -300 million).

Not surprisingly, corn weakened on this 2019 planting intentions while soybean prices were steady to slightly higher for most of the session. With the survey period beginning on Feb 27, the impact of this spring’s WCB flooding likely wasn’t picked up in the survey numbers. Recent strong cotton prices could also reduce corn seedings.

The USDA’s quarterly stocks had a mixed output with corn higher than expected while beans were less. In corn, its 8.605 billion bu. level was 270 million higher than trade average. Using exports and industrial usage, this level projects corn’s winter feed/residual demand at 1.245 billion bu., down 17% from 2017/18. This may prompt another 150-200 million drop in corn’s feed usage. But, given this past quarter’s weather & high live-stock numbers, this feed level seems quite illogical.

Soybeans March 1 stock at 2.716 billion bu. were 33 million bu. higher than trade’s average estimate. This suggests a possible 25-30 million increase in beans residual use. Wheat’s 1.591 billion bu. stocks suggest 15-20 million drop in feed use.

(Click on image to enlarge)

What’s Ahead

The trade’s focus was on the US planting levels. However, corn’s higher quarterly stocks added to the dynamics. An underestimated 2018 crop, an overestimate of on-farm stocks or a 17% yearly drop in the US winter feed usage are all possibilities, no answer until June 28 stocks. Spring US weather remains the biggest price factor along with US/China trade news. The current cold/wet spring outlook suggests holding sales.

Comments

Log in or sign up to join the conversation.