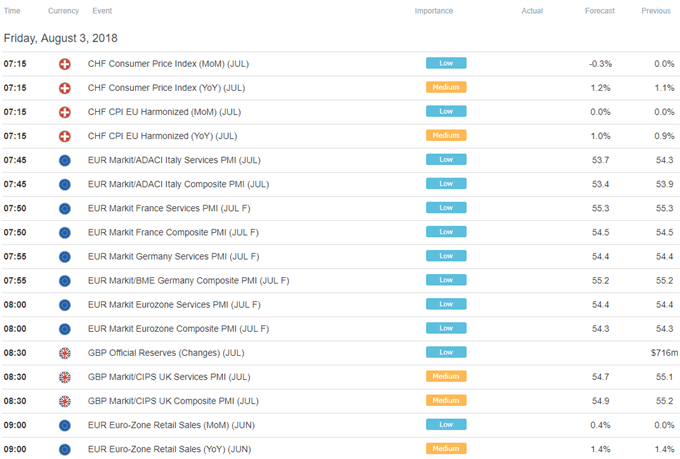

A steady stream of PMI surveys are unlikely to inspire significant reactions from the Euro and the British Pound considering their limited implications for near-term ECB and BOE policy implications. The former central bank appears to be on auto-pilot at least through year-end while the latter signaled just yesterday that its responsiveness to incoming economic data has been tempered by Brexit-linked uncertainty.

That puts July’s US employment report firmly in focus. A broadly on-trend set of outcomes is expected, with a 193k gain in nonfarm payrolls accompanied by steady wage inflation at 2.7 percent on-year and a slight downtick in the jobless rate to 3.9 percent. To the extent that these results mark continuity, they also endorse the Fed’s hints at two more hikes are appropriate this year. That bodes well for the US Dollar.

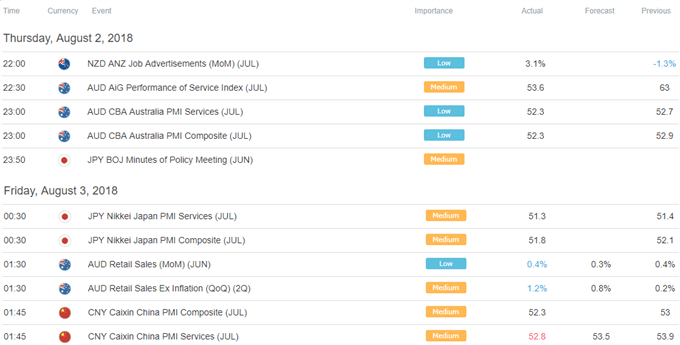

The New Zealand Dollar underperformed in otherwise muted Asia Pacific trade. The move tracked a dovish shift in the priced-in RBNZ policy outlook (as reflected in 30-day bank bill futures). As it stands, markets envision a rate hike no sooner than the fourth quarter of next year. The Australian Dollar edged up after local retail sales data topped economists’ forecasts.

ASIA PACIFIC TRADING SESSION

EUROPEAN TRADING SESSION

** All times listed in GMT. See the full economic calendar here.

Comments

Log in or sign up to join the conversation.