What’s Ahead:

Smaller US corn and soybean crops along with possible higher US corn feed demand & soybean export demands (see tables above) could tight this year’s ending stock to 1.709 billion bu in corn and 391 million bu in beans. These stocks level could still rally values to our previous price points, but a collapse of the US/China trade deal would be major black cloud on US 2020 ag prices. .

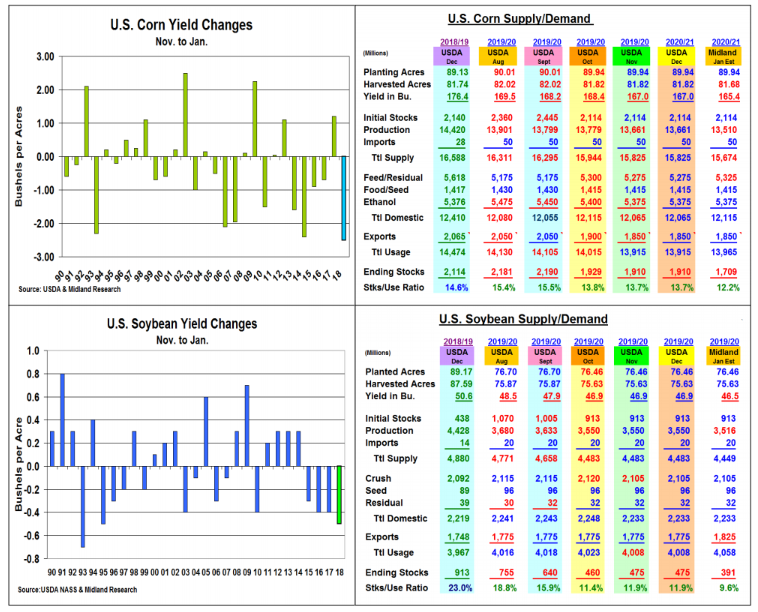

Market Analysis:

As the Ag markets enter 2020, the main focus has been on US/China trade deal and if it would be officially signed on January 15. The eruption of Mideast tensions after US took out an Iranian military general has now caused some doubt if China will sign the trade deal next week. This issue and the final US major row crop levels on the USDA’s January 10 report will be the market’s big factors going forward. Normally, these final US corn & bean output changes are modest. However, last year’s substantial yield changes and last fall’s delayed US harvest should make the market highly sensitive to these updates. In corn, 2019’s US yield estimate has been a moving target. A terrible Central US growing season began with heavy moisture & flooding delaying planting to the slowest level (67%) in early June since progress data began in 1970s. The ECB & the Dakotas were delayed the most. Modest heat & spotty dryness impacted the US crop during the summer. A wet/cold Oct & Nov slowed the northern US harvest leaving many cornfields unharvested when the snow arrived. Given the US corn yield tendency to drop 5 out the last 6 years from Nov. to Jan. & this year’s difficult northern harvest (140,000 less acres), a 1.6 bu lower US corn yield to 165.4 bu. and 151 million smaller crop to 13.51 billion bu. is expected. The US soybean output was also significantly impacted by 2019’s erratic weather. 12.7 million less acres were planted & the US average yield has likely declined to 5-year lows. The E Midwest output was impacted the most from delayed plantings while dryness limited the SE yields. Similar to corn, the US final bean yield has been lower than Nov for the last 4 years. Because of the N Plains Oct winter weather, we expect a 0.4 bu. lower US yield to 46.5 bu. & 34 million smaller crop to 3.515 billion bu. After the Small Grains & Nov spring wheat changes, no final US crop or stock changes are expected. Winter wheat seedings will be the trade factor.

Comments

Log in or sign up to join the conversation.