Market Analysis

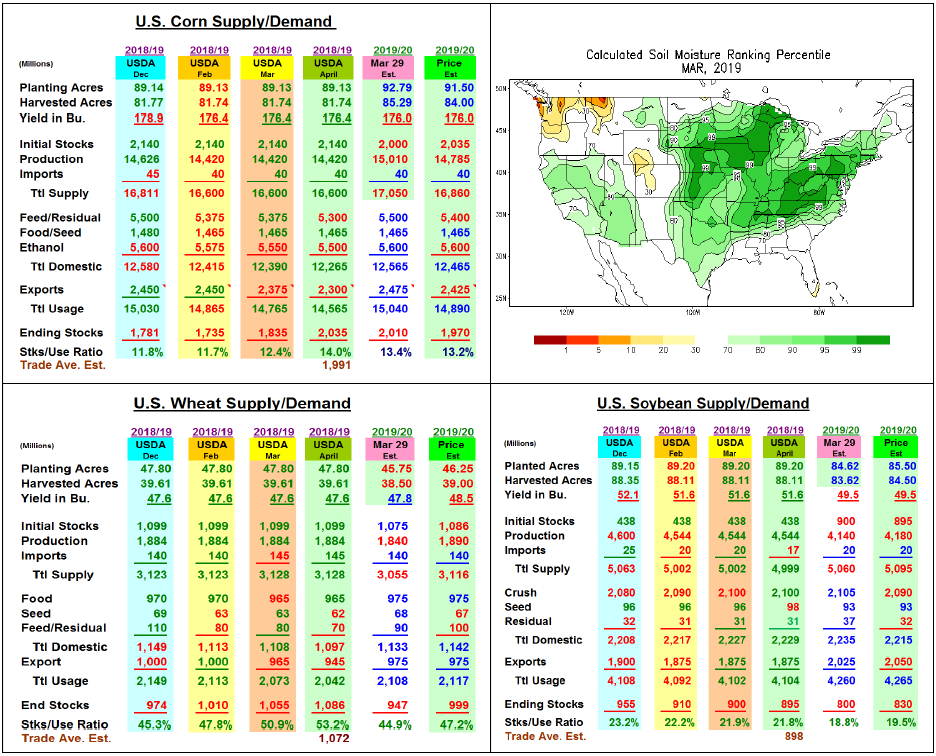

The markets were on the defensive ahead of the USDA’s April reports this week. After the March Quarterly Stocks Reports revealed some startling higher levels, particularly in corn, the trade was bracing for some sharp adjustments in the US grain supply/demand tables. Changes were made, but the overall adjustments weren’t significantly different from the trade’s average expectations. South Ameri-can corn and soybean crop changes also seemed modest.

In corn, March’s higher quarterly stocks did prompt the USDA to cut its feed demand, but by just 75 million bu. vs. ideas of 150 or more million reduction. Corn exports were also lowered by 75 million because of sales being behind the 5-year seasonal pace & both Argentina (+1 mmt to 47 mmt) and Brazil (+1.5 mmt to 96 mmt) corn crops being increased. The World Board also shaved 50 million bu. from corn’s ethanol demand because of weather problems. Overall, April’s 2018/19 stocks were upped 200 million to 2.035 billion bu.-- near the trade’s average estimate.

In soybeans, the USDA left the major demand forecasts for the old-crop year unchanged at 2.1 billion for crush and 1.875 billion bu. for exports. Despite some concerns about overseas demand and the USDA raising Brazil’s crop by 500,000 tons to 117.0 mmt, the World Board sliced just 5 million from US stocks to 895 million. Three million lower imports and 2 million smaller seed demand were the changes. Despite a stock residual issue, the USDA decided to wait to see the June stocks before making any big changes in the 2018 US crop size.

In wheat, the USDA sliced US feed demand by 10 million bu because of last month’s higher than expected stocks and its price relationship to other coarse grains in the US. Wheat’s slow export shipments vs. its seasonal pace also prompted the World Board to slice 20 million off exports. Overall, 2018/19’s old-crop stocks were raised by 32 million to 1.086 billion bu.

(Click on image to enlarge)

What’s Ahead

After retesting the recent March 29 lows, the market’s focus could be switching to the upcoming US planting season & final stages of US/China trade negotiations. Given the 90-99%% saturation level of Central US soils, it will take an extensive period of dryness before widespread plantings begins. This could strengthen corn & wheat prices while capping beans, but trade results will help beans. Hold sales.

Comments

Log in or sign up to join the conversation.