Market Analysis

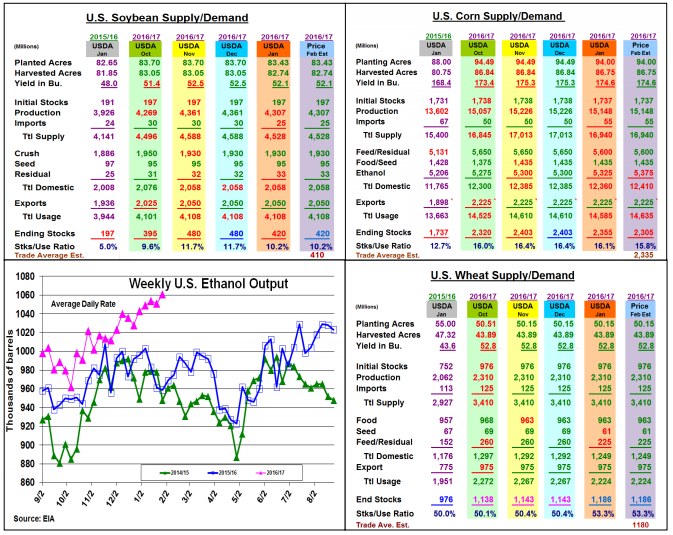

The USDA's upcoming February World Production and US/World Supply/Demand revisions will be released at 11 Am on Thursday. Traditionally, the Ag Department doesn't make a lot of changes in their US and World Supply/Demand levels and ending stocks on this report after finalizing their US production numbers last month. Many times in the past, the USDA's World Board has decided to wait and see how US demand and Southern Hemisphere crops turn-out. However, S. America’s January weather was quite volatile.

Excessive rains in central Argentina prompted exchange crop estimates in the 53 mmt area vs. the USDA’s 57 last month, but good early harvest yields from Mato Grasso has Brazilian analysts upping their crop ideas by 1-2 mmt from January’s 104 mmt level. Despite current US sales at 90% of yearly total, similar to 3 out of the last 4 years, this year’s shipments have slipped to the 4th slowest of past 5 year on a percentage basis for this date. This sluggishness and no relative change in S. America’s exports could prompt the USDA to leave the US 2016/17 foreign outlook level and soybeans ending stocks unchanged this month.

Another factor that has impacted this year’s export shipments has been the N. Plains excessive snow levels. With the region’s normal export pattern to utilize the PNW, logistical train issues getting sales moved to ports and returned to shippers for reload has impact corn, wheat and soybeans from this region. With corn & wheat both needing to average their highest shipment paces of 45.3 and 18.8 million bu. per week in 5 years for rest of the season, these two crops’ overseas demand may also be left unchanged until NC train movement improves this spring. The one factor likely to change corn’s ending stocks is the current record US ethanol output which should up this usage by 50 million bu. this month.

What’s Ahead

Despite the NC US transportation problems that have stalled shipments, the current sales will likely remain on books since the need for both grain and oilseed protein remains great and S Am corn exports aren’t likely until mid-to late summer. S. America’s growing season will continue to be a market factor, but utilizing March rallies to $10.60-$10.80 & $10.25-$10.40 in Nov to have 90% & 20-25% sold seems prudent.

Comments

Log in or sign up to join the conversation.