That didn’t take long. The Fed’s unpaid PR flack at the Wall Street Journal, Jon Hilsenrath, was out with hardly an hour to spare after the August jobs report—relaying word from the Eccles Building that ZIRP is in no danger of being rescinded early.

When at the July meeting our monetary plumbers saw “significant underutilization of labor resources”, which is code for continued zero interest rates, they were looking at an unemployment rate in June of 6.1%. So according to Hilsenrath, today’s weakish jobs report is good news for Wall Street’s free money crowd.

The fact that unemployment hasn’t fallen since the July meeting —and that job growth slowed in August— suggests Fed officials won’t make big changes to their policy statement and the signal they’re sending about rates when they meet Sept. 16 and 17.

Indeed, the Fed’s other unpaid spokesman, Steve Leisman at CNBC, had already made the point within minutes of the release. ZIRP will now last until next July, he opined. The danger that money market rates would rise, to say 40 bps, as early as March has been alleviated by the “disappointing” 142,000 print for August. Whew!

These people are counting angels on the head of a pin. Like Draghi’s 10bps cut yesterday, a potential delay in baby-step rate increases by three months next year is a meaningless irrelevance. That such microscopic moves could be treated with dead seriousness by the financial media and players in the casino is simply evidence of how deep the cult of Keynesian central banking has insinuated itself into the warp and woof of the financial system.

The truth is, labor market “slack” is a red herring. The problem of tepid growth in jobs and incomes is structural, and tweaking the monetary dials by a tick or two will not alleviate it in the slightest. Compared to 25bps from zero, consider what has really happened to the labor market since the Fed went all-in for money printing after the dotcom crash. Back then there were 75 million adults (over 16 years) who didn’t have jobs; today’s report shows that there are about 102 million jobless adults.

And, no, that 27 million gain in adult dependency is not due to well-deserved baby boomer retirements on social security. There are only 7 million more recipients of old age and survivors benefits today than there were in the year 2000. The remaining 20 million are on food stamps, welfare, disability, veterans benefits or are living in their parents’ basement or on the streets.

They have been made jobless first and foremost by a financialized economy that does not invest in productivity and growth, but mainly chases financial bubbles inflated by ZIRP and the Fed’s insensible pursuit of “wealth effects” and stock market props and puts. And that monumental deformation has been exacerbated by the “off-shoring” of a huge swath of the tradable goods economy. The latter is a direct result of 25 years of easy money and massive middle class borrowing that has resulted in $8 trillion of cumulative domestic consumption in excess of domestic production, and bloated domestic wages and costs that are not competitive in the world economy.

Finally, throw in the disincentives to work from a massive income transfer payment system and safety net that encompasses 110 million citizens who live in households with means tested benefits, and 150 million with government benefits of all kinds including social insurance. Now you have tidal forces operating on the labor market that shrink the impact of 10 or 25 bps from zero on overnight interest rates to the equivalent of economic white noise.

Since Greenspan launched the cult of Keynesian central banking and the financialization of the American economy in the late 1980s, the balance sheet of the Fed has grown from $200 billion to $4.4 trillion—or by 22X. The S&P 500 is up 10X notwithstanding three thundering booms and busts in the interim. Along the way, the great financial markets of American capitalism have been destroyed as agents of productive capital formation, efficient resource allocation and honest price discovery. The have simply become a giant, central bank operated and funded casino where the 1% gamble with make-believe money.

Meanwhile, consider the four charts below about the real main street economy. Real median family income is down 12 percent from its unsustainable 2007 housing bubble peak; more importantly, it was no higher in 2013 than it was way back in 1989 when the modern age of central bank money printing was just getting underway.

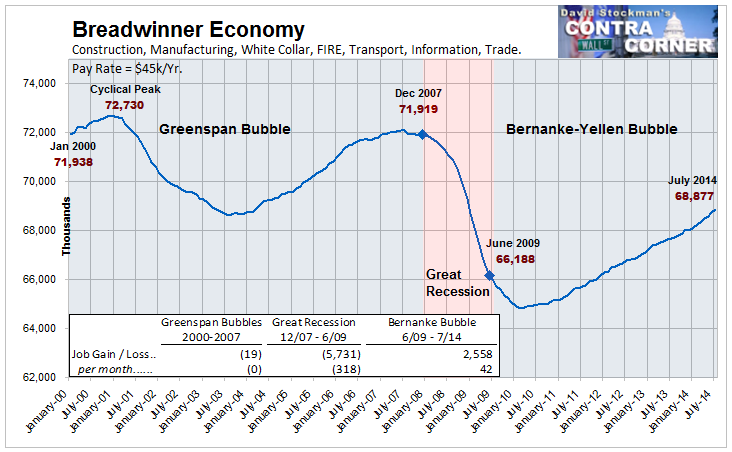

Likewise, the count of breadwinner jobs is still 4% lower than it was when the dotcom bubble crashed and real net capital investment is down 20% during the same 14 year period..

Breadwinner Economy

Real Business Investment

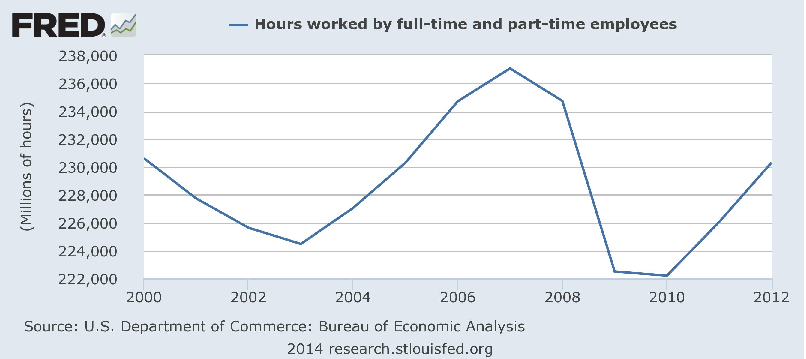

But the most stunning comparison of all, is between the balance sheet of the Fed and total labor hours generated by the non-farm economy. Even as the former has soared since the turn of the century, actual hours worked in the American economy have flat-lined for 15 years.

Someone should tell the monetary politburo that this isn’t working!

Comments

Log in or sign up to join the conversation.