Photo Credit: StockMonkeys.com

Box, Inc. (BOX) Information Technology - Internet, Software & Services | Reports June 1, After Market Closes

Key Takeaways

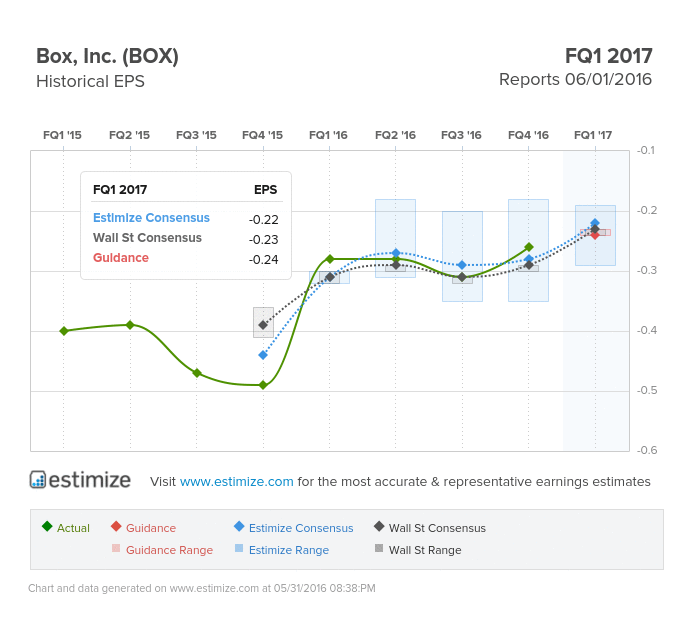

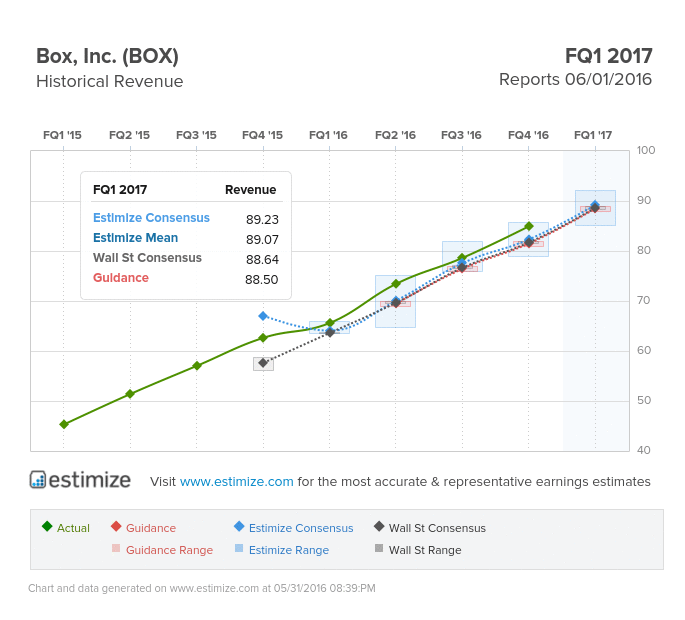

- The Estimize consensus is calling for a 22 cent loss per share on $89.23 million in revenue, 1 cent higher than Wall Street on the bottom line and right in line on the top

- Despite strong earnings growth over the last several quarters, Box stock is typically a big loser during earnings season, experiencing 10% declines in the month following a report

- Box has invested heavily in new initiatives such as security and administrative technologies

- What are you expecting for BOX? Get your estimate in here!

Enterprise technology has been one of the more volatile sectors today. Many of these names consistently post strong earnings and revenue growth but have watched share prices plummet. The primary causes of sinking share prices has been decelerating growth and weak forward guidance. Recently public company, Box, has suffered this very same fate in the past year and a half. When the company reports first quarter earnings tomorrow, investors will be glued to future guidance rather than the actual numbers.

The Estimize consensus is calling for a 22 cent loss per share on $89.23 million in revenue, 1 cent higher than Wall Street on the bottom line and right in line on the top. Compared to a year earlier this reflects a 19% increase in earnings and 36% revenue growth. Still the stock is a notorious loser during earnings season. In the day following its report, shares have historically fallen by an average of 4%, only to plummet 10% over the next 30 days. Shares are currently down 27.8% in the past 12 months, so any additional declines will be troubling for investors.

Box is best known for its cloud storage services, similar to Dropbox, but has also began to position itself in new ventures including security and administrative technology. These investments put Box in a favorable position to gain from the increasing adoption of cloud computing technologies. Moreover, the company’s partnerships and cross selling opportunities should bode well in the near future.

On the downside, Box continues to see decelerating growth. In Q1 2015, the company saw earnings grow 30% coupled with 45% sales growth. This quarter should almost certainly come in lower. As growth continues to slow down, share prices will likely also drop. Meanwhile, continuous investments into sales personnel and new technologies could take its toll on margins and profits.

Comments

Log in or sign up to join the conversation.