Painting is by my father, Naum Katsenelson. Prints available on Katsenelson.com

I wanted to send you this letter, spontaneously written on Sunday morning, sharing my thoughts on the market and your portfolio. I am on the flight from Denver to San Francisco with my twelve-year-old daughter, on a two-day father-daughter trip. I’ll try to compact my thoughts into the duration of the flight. I am only slightly apologetic for the pilot analogy, which the turbulence on this flight brought to mind.

I have been feeling very uneasy about the market and the economy (I wrote about it in the last letter). You can clearly see this in your portfolio. We have been trimming positions as they run up, buying smaller position sizes, and buying businesses that march to their own drummer and do not depend on the economy continuing to march higher as it has. Over the last two decades our economy has been acclimated to insanely low interest rates, and reacclimation to higher and rising rates is going to be difficult.

On the stock market.

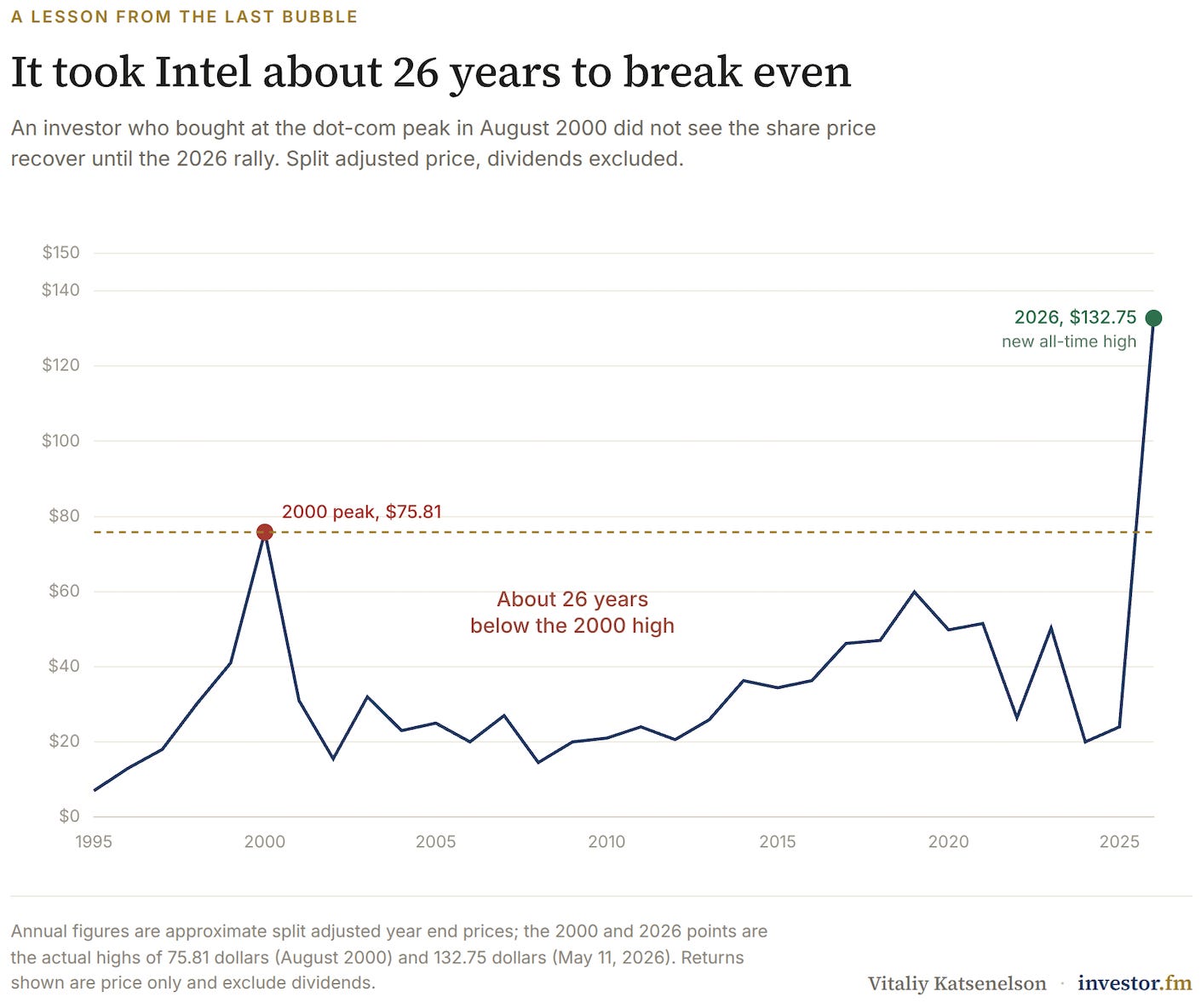

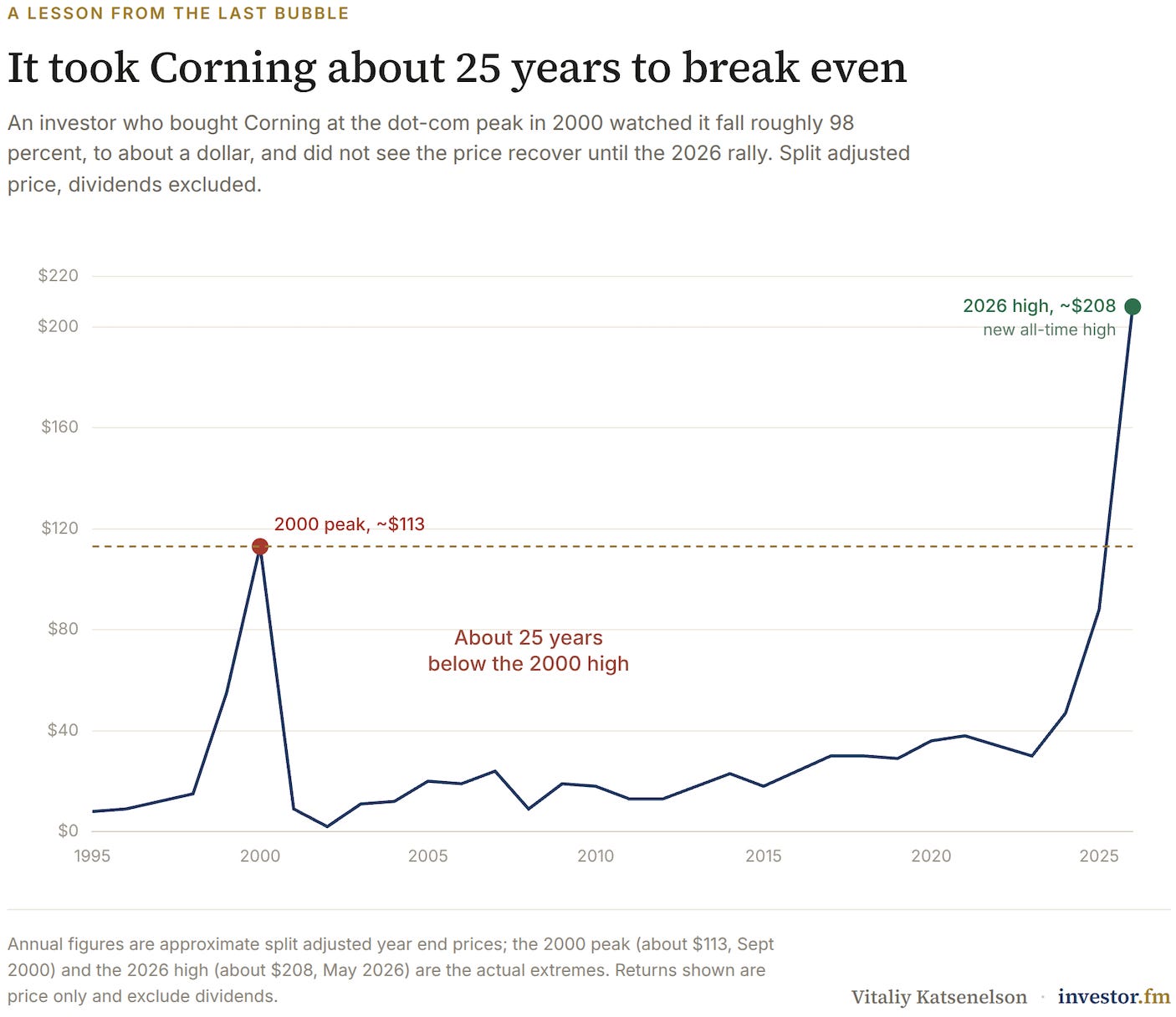

Calling the top of a bubble is difficult, and it is a fool’s errand. But this market is starting to feel incredibly bubbly, approaching circa 1999. There are so many similarities that it is eerie. I did not expect that Intel (INTC) and Corning (GLW), the darlings of 1999, would be at multidecade highs and trading at nosebleed valuations. It is rare for the darlings of one bubble to be the darlings of the next. They are great examples that the companies poised to be major contributors to a technological future are not always the ones that reap that future’s economic benefits. As the charts below show, if you bought them at the peak of their glory, it would have taken you two decades to get your money back.

This brings me to the next future casualty of today’s hysteria, Nvidia (NVDA), the most valuable company in the world, trading at 30 times 2026 earnings. That is not an insane valuation for a company growing very fast. But in the case of Nvidia, the E in the P/E will likely decline a lot in the future. Today, if you are building a data center, Nvidia is mostly the only game in town. Several things are likely to happen. There will be more competition. We are approaching peak demand. And capital markets won’t keep financing the customers who buy its chips. I could write a very long essay just about Nvidia.

Three of the biggies are going public: SpaceX (which owns xAI), Anthropic, and OpenAI. All of them are losing money. Together they spend hundreds of billions on data centers, the bulk of which went to Nvidia for AI chips. Meta (META) and Google (GOOG), cash cows in their own right, were subsidizing their AI spending from their core business. When that was not enough, they levered mildly and now, for the first time, they are actually issuing stock. Yes, they went from net buyers of their own stock to sellers.

You have two scenarios. In the first, these investments lead to such high returns that these companies end up swimming in cash and fund their future Nvidia chip purchases out of future cash flows. But please think about it. All of these companies collectively are throwing close to a trillion dollars, yes, a trillion, at AI. They feel like they are fighting for their survival, and that is exactly what creates a race to the bottom, where their future profitability gets competed away fiercely. And if these companies don’t spend a trillion dollars on data centers next year, Nvidia’s earnings will be a lot, lot less.

Nvidia and the semiconductor sector are a classic capital-cycle story: demand creates too much supply, and a boom leads to a bust. I have written about it many times before, from the railroads in Great Britain in the 1800s to telecom in 1999. I don’t know if it will be next week or next year, but this will predictably end in tears. Nvidia is unlikely to remain the most valuable company in the world, unless all the others become a lot less valuable. The signs of a bubble are everywhere. I am experiencing 1999 déjà vu.

Over the next few weeks the capital markets will be hit by three IPOs and two secondary offerings from Google and Meta, totaling multiple hundreds of billions of dollars. This alone will likely suck liquidity out of the capital markets and put a nice bow on the AI rally that drove the S&P 500 higher this year.

But the bubble is not just in tech stocks.

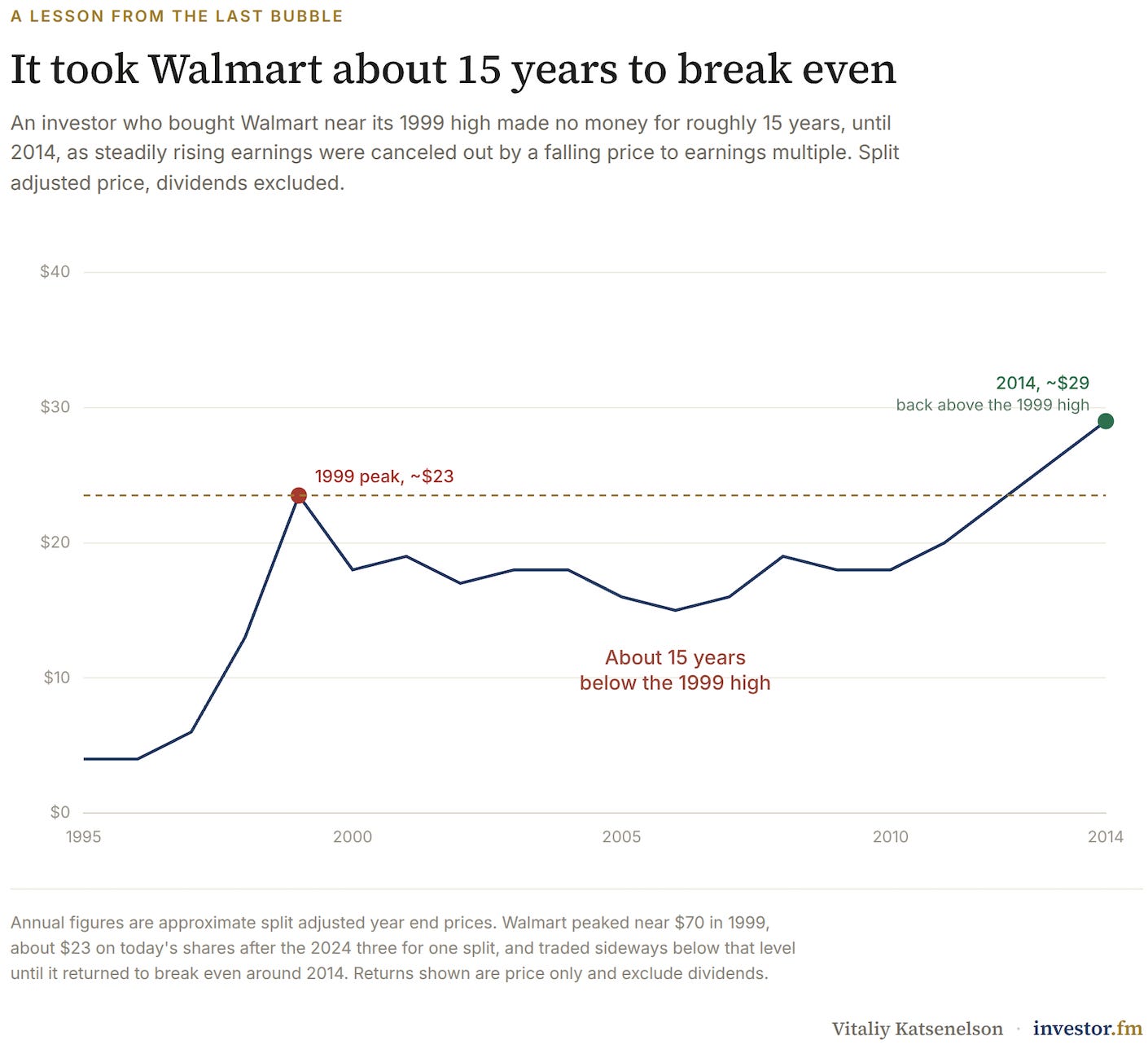

Walmart (WMT) is another bubbly stock from the 90s, and it has nothing to do with technology or the future. I vividly remember in the late 90s Fortune writing a glowing piece on Walmart, and my cousin reciting how great the company was after reading it. I was telling him that Walmart was trading at a very high valuation, 50 times earnings. He was telling me it didn’t matter; it was a great company.

The stock did not collapse, but it became the number one example I use to explain my thesis of sideways markets. Any earnings gains that Walmart dutifully manufactured over the next decade and a half were wiped out by price-to-earnings compression. Shareholders who bought this wonderful company in 1999 made no money until 2014, other than collecting pitiful dividends.

Today Walmart is trading at 50 times earnings again. Those who don’t study history…

I can feel the 90s in client cancellations.

We had an incredible year last year. But we already had a client cancel this year because he did not like our returns over the last three years which were ... {Legally, I am not sure I can discuss our returns here, but you can request to see ours here.}

Losing a client doesn’t bother me when we have made them money.

The reason I bring this up is that I remember something similar happening to us in 98 and 99. We were producing strong returns, but we underperformed our clients’ neighbors who had put their money in the aforementioned stocks, and we were losing clients. I remember a line from a value investor’s letter in the late 90s, from Jean-Marie Eveillard: “I would rather lose half of my clients than half of my clients’ capital.” I am actively trying to avoid the second, and I am really not worried about the first. If IMA managed half as much capital, my life and our employees’ lives would not change a bit.

This is not the letter of a value investor looking for excuses for his past returns. I am very proud of what we have achieved for our clients over the last decade. If we keep repeating what we have done, I’ll be a very happy investor. I cannot make any promises, because I don’t know.

We are not competing with index funds, “the market,” or the neighbors. Our number one goal is to avoid a permanent loss of capital. The firm manages all of my family’s liquid assets, so I don’t want to lose my retirement or my kids’ college funds in a race to beat crazy. The road ahead for the stock market may lead higher, maybe a lot higher first, but what happens after that is what shapes our strategy. Today the market is trading at one of the highest valuations in modern history. AI is promising nirvana, and it will be an incredible change, but the future will not be distributed evenly. There will be losers.

I am writing to tell you that our returns going forward are likely to underperform “the neighbors” for the foreseeable future, and we are not going to do anything about it. In fact, we are going to continue doing what we are always doing: being patient, process-driven, analyzing each investment on its own merit, focusing on the margin of safety, and not assuming the sun will shine 365 days a year in our forecasts. We are going to continue to be slightly overdiversified for the time being. (I explained this in the last letter.)

I think value investing will outperform the market over the next decade, not because we are so brilliant but because the market will make the returns of Walmart from 1999 to 2014 look like a dream. This is especially true once SpaceX, a multi-trillion-dollar company priced on a transgalactic opportunity set, joins the S&P 500 in a few weeks.

Value investing doesn’t do as well when the punch bowl is spiked with euphoria and everyone only looks up. It is when the punch bowl is taken away and investors start looking down that value investing, or simply common sense, does well.

I look at this relationship between you and me as the captain of the plane and the passengers. I am a nervous flier, and I become slightly religious during turbulence. The turbulence a few minutes ago was a good reminder of that. I once told a client who used to be a pilot about this. To my surprise, he told me that he is a nervous flier when he is a passenger, but he’s calm as a clam in the pilot’s seat. The reason is simple: pilots have full visibility, visual or through radar. They know what is going on, they have done it for a long time, and most importantly, they have control.

Passengers are unlikely to ever feel as comfortable during a bumpy ride as the pilot, unless you get drugged on booze (not something we advise). But I have found that I am a lot less nervous when the captain sets clear expectations.

Well, this is your captain speaking. The weather outside is going to get bumpy, but we are preparing for it. Our portfolio looks nothing like the bubbles we are flying through, and despite the low oxygen (euphoria), we are going to get through this together. Remember, neither I nor my family (wife, kids, my brother) have a parachute. We are on the same plane as you. Our goal is not to get to the destination fast, but to get there. At times it will look like we took a longer, more scenic route, and so be it.

Comments

Log in or sign up to join the conversation.