Many analysts say this 8-year-old bull market is "overextended," or "overbought." In saying this, they are measuring this bull market from its birth date (March 9, 2009) rather than over a longer period of time, including market ups and downs. Market returns since both 2000 and 2007 have been sub-par so it stands to reason that the current market has a long way to go to "catch up" to its historical (60 year) average compounded growth rate of 6.9% per year.

Written by Gary Alexander

...According to Bespoke Investment Group, April is the best stock market month in the last 50 years and 20 years - by a long shot. April has risen in 16 of the last 20 years (80%), the highest success rate of any month in the same time period.

Why? Perhaps it's:

- the spring weather,

- or tax refunds,

- or the funding of retirement plans...

- or perhaps it's because most of the top earnings analysts see 10% - 14% earnings growth (year-over-year) in the first quarter. (Earnings announcements will run from April 10th to about May 15th.)..Part of the rise comes from:

- weak comparisons from a year ago,

- a return to profitability in the energy sector,

- rising profits in the financial and tech sectors,

- a U.S. dollar that had been generally weak in the first quarter (the WSJ dollar index is down 3%), removing a major headwind to earnings for large multinational exporters and

- the U.S. dollar is down sharply vs. some key trading partners:

- down 9.7% to the Mexican peso,

- -7.5% to the South Korean won,

- and -4.8% to the Japanese yen.

- ...improving economic growth in Europe, Japan, China, and many emerging markets increasing demand for many U.S. products...This tends to favor large multinational companies

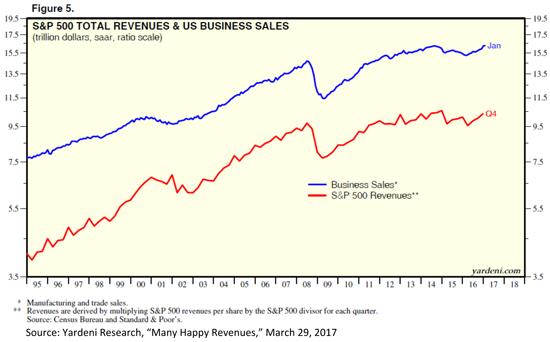

- and a projected rise in Q1 revenues of about 7%...[and] an increase in the volume of U.S. business sales naturally tends to parallel the rise in S&P 500 revenues (see chart, below):

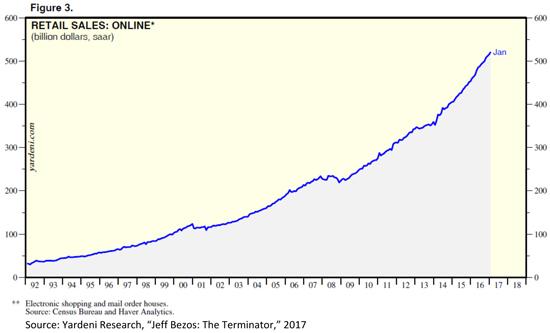

This recent growth in sales isn't evident at your local malls, as super-sellers on the Internet are generating the lion's share of revenue growth in recent years. Last month, the U.S. Census Bureau reported that online shopping rose to a record $521 billion (annual rate, seasonally adjusted) in January, representing a record 29% of total retail sales (combined online and in-store sales). This trend shows no sign of ending:

This Market Still Has Some "Catching Up" to Do

Many analysts still say that this 8-year-old bull market is "long in the tooth," or "overextended," or "overbought." In saying this, they are measuring this bull market from its birth date (March 9, 2009) rather than over a longer period of time, including market ups and downs.

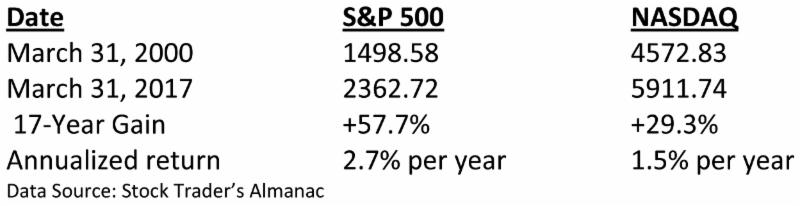

- If you go back 17 years to the birth of the new Millennium in early 2000, the annualized stock market gains have been well under 3%:

This comparison, of course, is just as unfair as measuring from the bull market's birthday. As I wrote in these pages back in May, 2009, a bear market of historic proportion (2007-09) implies a bull market of equally historic proportions - since the market, over time, tends to revert to its mean growth rate.

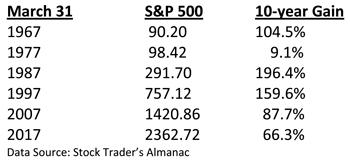

- Taking decades at random, we can compare the last 10 years to the previous five decades and see that the S&P's gains since March of 2007 are historically weak - the second worst decade of the last six decades.

- Measuring from 60 years ago, March 31, 1957, when the S&P 500 stood at 44.11, the S&P 500 has risen by 5,256%, which works out to an average compounded growth rate of 6.9% per year, or 95% per decade.

Market returns since 2000 or 2007 are clearly sub-par, so it stands to reason that the current market can continue to "catch up" to its historical norms of about 7% annual growth, or nearly 100% per decade.

.webp)

Comments

Log in or sign up to join the conversation.