Shipping stocks have felt the meltdown in energy prices. Teekay Corp. (NYSE: TK) is down 80% over the past year. Overseas Shipholding (NYSE: OSG) has fallen by more than a third. And Frontline (NYSE: FRO) has been cut in half since its high late last year.

One shipping company that has not been hurt nearly as badly is Ship Finance International (NYSE: SFL). That’s likely because the Bermuda-based company ships things other than oil, including cars, dry bulk and chemicals.

The stock sports an attractive 11.7% yield and has paid a dividend every quarter for the past 12 years.

But can investors rely on that dividend?

Ship Finance is interesting to look at because things at the company aren’t necessarily black and white.

For example, in the past 10 years, Ship Finance has cut its dividend three times. There was a $0.78 payment in late 2012, and then the next dividend was $0.39 in 2013. But that’s because Ship Finance paid what would have been the first quarterly dividend of 2013 at the end of 2012. It made this decision as a result of the widespread belief that U.S. taxes on dividends would increase substantially in 2013 (they didn’t).

In February 2012, Ship Finance reduced its quarterly dividend to $0.30 from $0.39. For that full year, the total dividends per share received actually rose, but I still consider it a cut. If an investor counted on dividends to pay the bills, that 23% haircut in February 2012 would have caused problems – even though the dividend returned to previous levels the next quarter.

Ship Finance cut the dividend for the first time during the Great Recession; the quarterly dividend dropped 50% in the first quarter of 2009, from $0.60 per share to $0.30.

Those are two real cuts in the past seven years, and that’s something I have to consider.

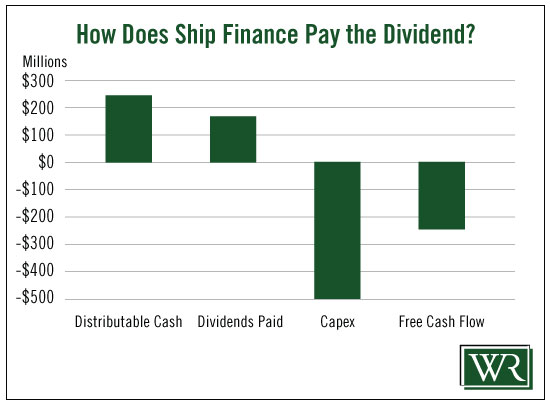

In Ship Finance’s fourth quarter earnings report, it said distributable cash was $244 million. Meanwhile, the company paid out $165 million in dividends. That’s a payout ratio of 68%, which would put it well within my comfort zone.

As you know, I like to see stocks with payout ratios of 75% or lower.

But Ship Finance’s distributable cash doesn’t tell the whole story.

The company calculates distributable cash as revenue plus profit share – minus operating expenses, interest expense and loan amortization. It leaves out capital expenditures, which is normally used in the equation for free cash flow.

In order to determine if a company generates enough money to pay its dividend, you usually consider capex.

A company could make a jillion dollars in profit or operating cash flow, but if it spends a jillion and one dollars in capex, that doesn’t leave anything to pay the dividend. And it’s important that an investor understand whether or not the company generates enough free cash flow to fund the dividend.

Ship Finance doesn’t.

While distributable cash was an impressive $244 million in 2015, capex was a whopping $497 million, which means the company burned through $253 million in order to operate and invest in its business.

The only way to pay the dividend if a company has negative free cash flow is to sell stock, borrow the money or pay it out of cash on hand.

The good news is that capex is expected to fall to $190 million this year and $101 million in 2017. That will give the company positive free cash flow, though it may be a while before the figure is high enough to comfortably pay the dividend.

A history of dividend cuts and negative free cash flow are a slam dunk for a low Safety Net rating. The good news is that as free cash flow improves, the company could see an upgrade. But I suspect that’s at least a year or two away.

Dividend Safety Rating: F

Comments

Log in or sign up to join the conversation.