Not long ago, someone I know paid $7 a gallon for gas. (They live in Washington state, not France.)

The cost of nearly everything is going up, and sky-high oil prices are only going to make it worse. It’s not surprising that everyone is looking for ways to boost their income.

The financial services industry is very happy to provide products that do just that. The problem is these products are usually expensive and underperform the market. In many cases, they are also very illiquid, meaning you can’t get your money out of them easily.

There are three products in particular that I despise and think are traps for retirees and pre-retirees.

1. Annuities

I want to share my favorite statistic about annuities, because it tells you everything you need to know about these products.

In 2016, the Department of Labor passed a rule that all financial representatives would be considered fiduciaries. That means they must act in their clients’ best interest. When that rule was passed − before it had even been implemented − variable annuity sales fell 22%.

Two years later, the Trump administration killed the rule, and annuity sales soared 40%. They hit a record of $461 billion in sales in the U.S. in 2025.

Think about that. When financial representatives knew they would get in trouble for selling products that were not in clients’ best interest, they stopped selling annuities. When there were no longer legal consequences for doing so, sales of annuities skyrocketed.

Now, it’s easy to understand why annuities are popular − especially fixed annuities. Fixed annuities offer a fixed payment over a certain number of years (or a lifetime) after the buyer has made a lump sum payment. The buyer knows that there will be a specific amount of income coming in, nearly guaranteed.

Variable annuities have fluctuating payments based on a variety of factors, depending on the exact product. They are often tied to some sort of market index. If the market is strong, you get paid more, though there is usually a ceiling. If the market is weak, you either lose less or don’t lose anything at all.

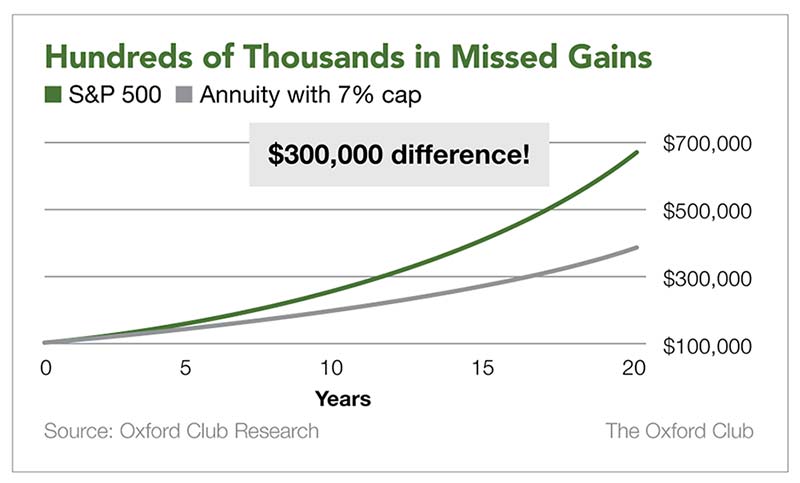

For example, you could buy an annuity where, if the market falls 0% to 10%, you won’t lose anything. If the market falls more than 10%, your maximum loss will be 10%. However, your gains are usually capped, so if the annuity in our example has a maximum gain of 7% and the market goes up 20%, you only make 7%.

Here’s the difference over 20 years if you earned 10% annually in the S&P 500 versus 7% from an annuity. Even if you assume the best-case scenario each year for the annuity (and exclude the thousands it’d cost you in fees and commissions), you’d miss out on nearly $300,000.

Variable annuities are the worst of the worst. They have high commissions (usually around 5% to 7%), are very complex, and charge high fees if you want to take your money out early.

I strongly recommend avoiding variable annuities.

Fixed annuities are bad, just not as bad as variable. Their costs are still high − especially if you want your money early − and you’d be locking in today’s low rates for the long term.

2. Whole/Universal Life Insurance

The “Bank on Yourself” movement was very popular a number of years ago. The idea is that you buy a whole or universal life insurance policy, stuff it full of cash, and then borrow against it if you need money. In the meantime, your cash grows along with the market (depending on how you have it invested).

Like annuities, these policies are expensive. Between 5% and 10% of your premium will go toward commissions, including 60% to 80% of your first year’s premium.

Furthermore, the remainder of your premium doesn’t all get invested for your benefit. A portion of it goes toward the insurance coverage you get along with the investment product.

Lastly, if you miss your premium payments, you’re screwed. The idea behind these policies is to build up the cash in the policy for as long as possible. But 75% of policies are eventually surrendered, meaning the policyholders do not benefit from long-term capital appreciation, they no longer have the death benefits that they paid dearly for, and, depending on when they surrendered their policies, they may have incurred steep penalties.

If you need life insurance, you are usually better off getting a term policy and investing in the market for the long term. It will be way cheaper. In fact, whole life policies cost around eight times as much as term life. You’ll also have access to your funds whenever you want or need them.

But if your family would be okay financially if you were to pass away, you probably don’t need life insurance. Life insurance really should only be used to replace the income that you generate.

3. Reverse Mortgages

These financial products are often peddled on TV by handsome, older male actors like Henry Winkler, Tom Selleck, and Robert Wagner, because the banks are marketing to mostly older women who are in bad financial shape.

A reverse mortgage is when the bank gives you money to live on based on the equity in your house. You never have to pay it back − as long as you live in the house for the rest of your life.

You do not make payments to the bank while you’re living in the house. If you die while still living there and your heirs don’t pay back the loan, the bank gets the house, so you have to be okay with that arrangement.

If you move to a relative’s house or to a senior living situation, you must pay back the loan. You may be able to do that by selling the house, but if you can’t pay back the loan, your house belongs to the reverse mortgage lender. (If your spouse is a co-borrower and remains in the house, you may not have to pay back the loan at that time.)

As with annuities and whole life policies, the rules are complicated and the fees are high.

A reverse mortgage should only be used by someone who is in need of funds to survive, has no other options, and is comfortable with their heirs either having to pay back the loan or losing ownership of the house.

It can be a lifeline, but it should only be used by those who are desperate for one.

Always Weigh the Cost

The financial industry knows that times are tough, and they will gleefully offer you so-called solutions to your cash flow problems. Just remember there’s a steep cost for all of the bells and whistles they offer.

You will usually do much better by choosing the cheapest and simplest alternatives, such as investing in stocks and individual bonds on your own.

What’s your experience with these three investments? Are there other investments or products that you think investors should avoid? Let me know in the comments section below.

Comments

Log in or sign up to join the conversation.