The great Austrian Economist Ludwig von Mises was the first to pinpoint the cause of the business cycle: overexpansion of credit by the central bank. The difficulty for investors has always been in applying his insight in a pragmatic way (see “Macro: The Holy Grail of Investing”, Top Gun Financial, March 22, 2026). When does the boom crescendo and turn into a bust?

As the economy has become more financialized, the stock market has become less a barometer of the real economy and more a major part of the economy itself. This is George Soros’s concept of “reflexivity”. My contention in this blog is that a constellation of catalysts combined with an overvalued and complacent market that has ripped for 17 years is setting the stage for a devastating crash.

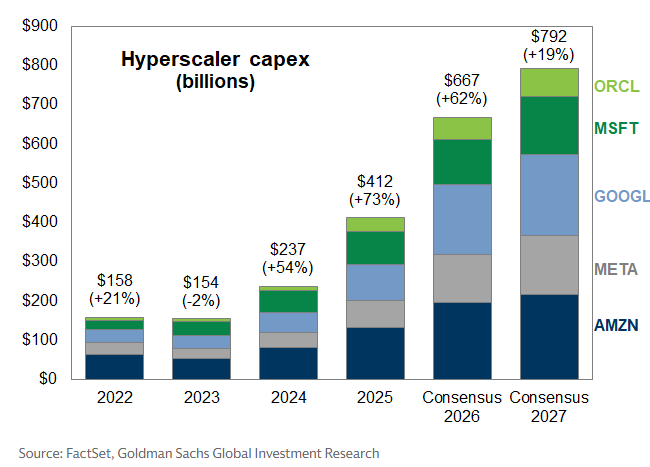

Let’s start with AI. Perhaps the most important pillar propping up the market is the belief that AI is about to revolutionize the economy by massively increasing productivity. Based on this premise, the four hyperscalers – Google (GOOGL), Amazon (AMZN), Facebook (META) and Microsoft (MSFT) – are forecast to spend nearly $700 billion this year on CapEx (see Dan Gallagher “The AI Spending Spree Is Far From Over” [SUBSCRIPTION REQUIRED], April 23).

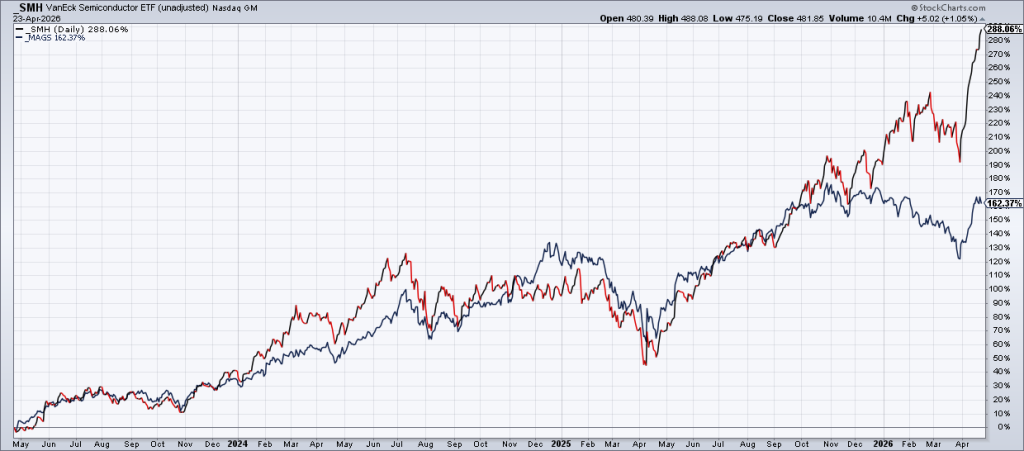

That money is flowing into the coffers of Nvidia (NVDA) and other leading semiconductor firms, which are leading the market. But all that CapEx will eventually have to be depreciated on the income statement. In other words, if AI doesn’t pan out the way Panglossian optimists seem to think it will, a lot of this CapEx may be malinvestment. The divergence between the semiconductor stocks (SMH) and The Magnificent 7 (MAGS) suggests to me that the market is starting to be concerned about this possibility.

Jim Chanos tweeted that a similar thing took place during the Dot Com Bubble when companies poured money into building out the infrastructure for the web which propped up the market until it became clear that much of the investment wasn’t going to have the expected return – and then the market collapsed. (For an excellent recounting of the Dot Com Bubble and Bust see John Cassidy Dot Con).

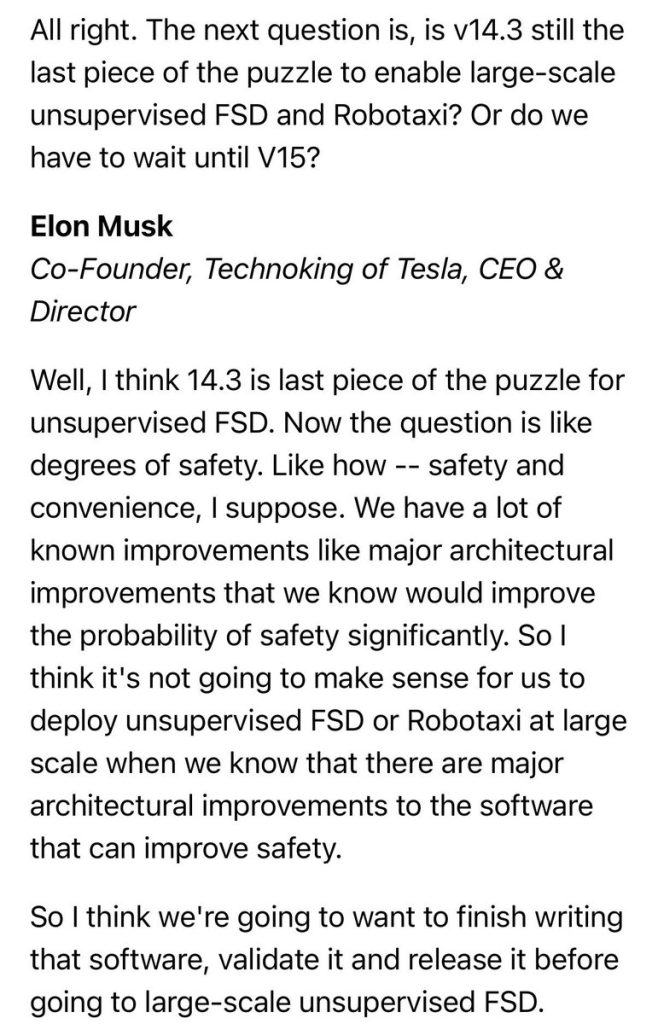

Tesla (TSLA)’s (TSLA) 1Q26 earnings report Wednesday afternoon may be the tip of the iceberg. When the numbers came out, the market sent shares up on a “double beat”. But after Elon Musk pushed back the timeline for Full Self Drive (FSD) on the conference call, the stock reversed course.

While the stock was only -3.56% Thursday, I think this could be a bigger problem than the market realizes because TSLA is a story stock with all its valuation based on promises about FSD, robotaxis and Optimus robots that are not producing much revenue at the moment. If the story starts to come apart, the stock has a lot of room to fall as the current EV business is only worth a fraction of the stock price.

Third, bulls aren’t much worried about the Iran War but I think this is a mistake. While the American public has little appetite for this war, for the Iranian regime it’s life or death. Their resolve may be more than Trump bargained for when he impulsively began the war (see “How Trump Miscalculated In Iran” [SUBSCRIPTION REQUIRED], WSJ, April 10). The market isn’t pricing in the risk of high oil prices for an extended period of time or the potential for escalation.

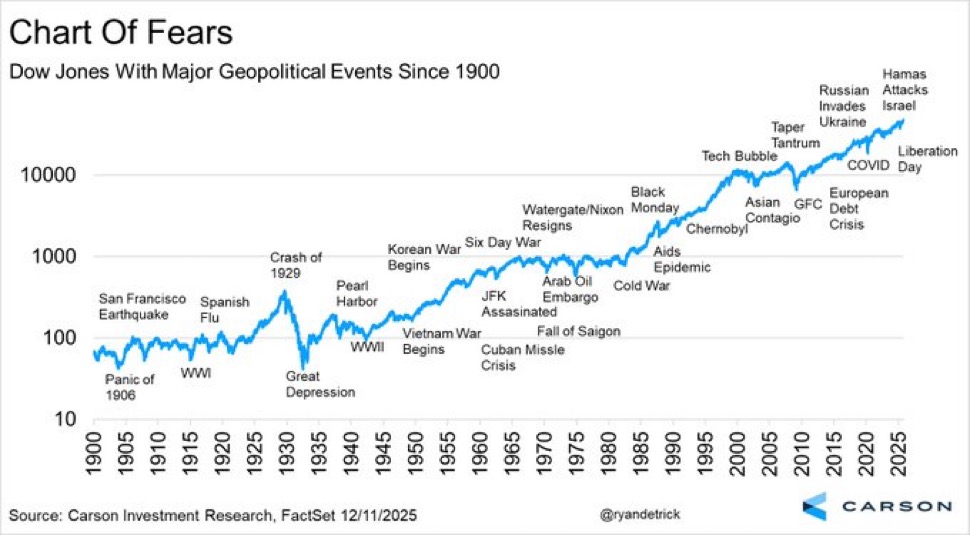

Last, the Chart of Fears posted by permabull Ryan Detrick points to complacency in market psychology. The market hasn’t experienced a nasty bear market since The Great Recession almost 20 years ago. Buying the dip has always been rewarded since then. Many investors have never lived through a real bear market; it’s just been easy money for them. All you had to was put money in an index fund and hold. They’re not prepared for hard times.

Comments

Log in or sign up to join the conversation.