The American housing industry was at the center of the last financial and economic crisis in the in 2008 and 2009. Of course, rapidly rising housing prices leading up to a 2007 housing peak together with the subprime mortgage fiasco contributed heavily to the massive economic downturn in 2008.

Nonetheless, since 1980 and except for the Great Recession in 2008, the US housing market apparently weathered all recession quite well.

Indeed, in mild recessions, housing prices tend to hold up and even rise modestly during the downturn as mortgage rates fall in tandem with interest rates. If the recessions are mild, home prices often continue to rise because interest rates fall, job losses are limited, and household formation continues to expand.

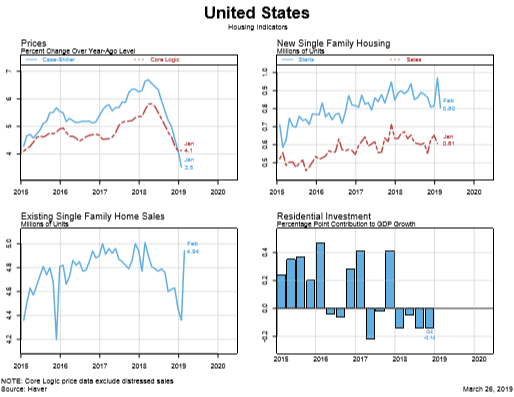

Currently, most economic indicators of housing activity — sales, starts, and inventories — are trending lower. Since a downturn in housing often precedes the onset of a US recession, some investors are seeing these events as a prelude to a major economic slowdown in 2019-2020.

The real question is if the US slips into a recession in 2020 or 2021, will the housing market be a safe haven and/or will it revert into a major collapse such as occurred in 2008-09?

Although the housing industry has been slowing, prices are still rising, and unlike 2008, the current housing market is not being driven by homeowners who are the highly leveraged.

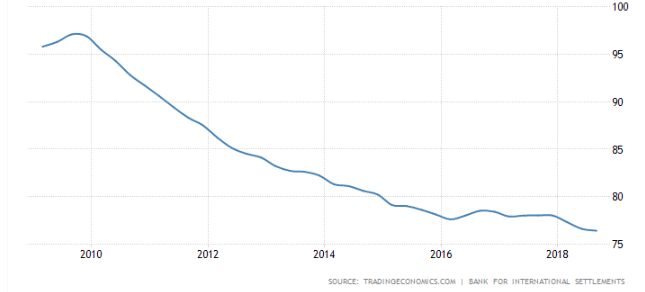

In fact, the household debt to GDP ratio has been decreasing since the Great Recession ended in 2018. Household debt fell to 76.4 of GDP in the third quarter of 2018 from its all-time high of 98.6% in the first quarter of 2008. In plain words, American households are far less indebted today than they were during the Great Recession.

Moreover, there seems to be a scarcity of inventory in the housing market, which suggests that housing prices would either be stable or modestly increase in a mild recession.

Finally, there is the whole issue of interest rates and housing affordability to consider.

A common measure of broader interest rates, the yield on ten-year treasuries, was 2.4% at the beginning of 2018 and rose to a peak of 3.2% in October of last year. Since ten-year treasury rates have dropped to about 2.4% as of Mach 18. The drop is significant, and also will favorably affect mortgage interest rates.

As the following chart illustrates, residential investment can play an important role in the growth of the economy. At its recent peak, residential spending accounted for about 0.5 percent of total GDP growth. Nonetheless, in 2008 housing construction actually reduced American GDP growth in every quarter. At the same time, US real estate prices in the US decelerated through all of 2018, a process that carried over into early 2019.

(Click on image to enlarge)

(Click on image to enlarge)

United States Household Debt To GDP (%)

(Click on image to enlarge)

US Treasury 10 Year Yields

Comments

Log in or sign up to join the conversation.