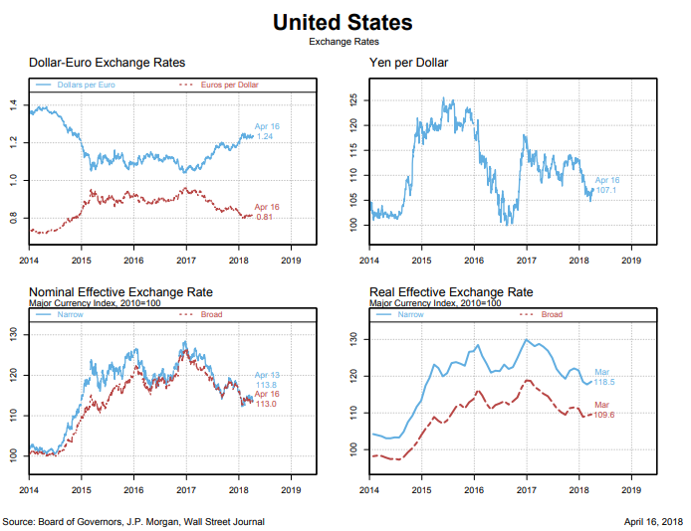

“The USD rout continues. The trade-weighted dollar’s depreciation in Q1 was the fifth in a row, with a cumulative 9% drop since the end of 2016. Foreign investors may be finding American assets unattractive amidst unsustainable U.S. budget deficits which have historically been correlated with a weakening greenback. Washington’s protectionist tendencies are also not helping America’s reputation globally and by extension the USD. Even world central banks seem to be losing faith in the big dollar.” (Krishen Rangasamy, National Bank Fiancial Hot Charts, April 3, 2018)

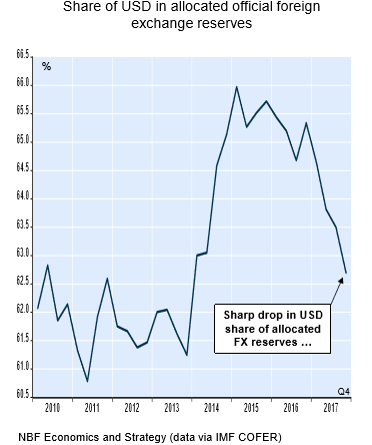

For the past 70 years, the U.S. dollar has been the world’s dominant currency, with two-thirds of the world’s allocated foreign exchange reserves held in U.S. dollars. However, this looks set to shift, with the Chinese yuan growing in prominence in the European market.

In 2016 the IMF decided to include the yuan among the currencies that make up the Special Drawing Right, an alternative reserve asset to the dollar. Then in June 2017, the European Central Bank announced it had exchanged €500 million ($611 million) worth of U.S. dollar reserves into yuan securities. More recently the German Bundesbank said it would include the yuan in its reserves for the first time, resulting in the yuan hitting a two year high against the dollar after this was announced. Following this, the French central bank then revealed that it already held some reserves in yuan.

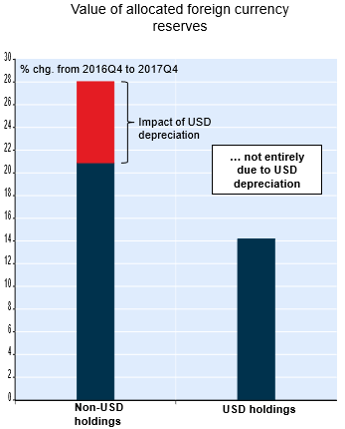

Obviously, since most central banks hold their reserves in U.S. dollars, even a marginal shift to the yuan, or any other currency, will impact the U.S. dollar adversely.

The Global Economy’s Strength Also Explains The Recent Weakness In The U.S. Dollar

The U.S dollar has been weakening this year and the U.S. economy has been growing quite well. Nonetheless, despite his "America First" agenda, Donald Trump said on several occasions in 2017 that he thought the dollar was too strong and wouldn't mind if it lost some of its value.

Of course, a weaker dollar lifts the value of foreign sales and profits for U.S. multinational companies once they are translated back into dollars.

Probably the main reason for the recent weakness in the U.S. dollar is continued robust global growth, which tends to support commodity prices and the currencies of commodity producing countries (e.g. the Canadian dollar) and in effect imposes downside pressure on the U.S. currency.

i.e. The strengthening of the 'rest of the world's economy (RoW) relative to the U.S. should continue to weaken the U.S. dollar.

Ironically, the strengthening of the rest of the world effect should outweigh any offsetting impacts of future interest rate hikes on the dollar. U.S. interest rates rose faster than those of most other countries during 2017 and this will clearly continue this year, since policy interest rates will likely rise at least three times this year.

Normally rising interest rates are a positive driver of currency appreciation because they attract inflows of foreign capital due to the higher returns on offer, but BMO does not see this happening in 2018.

Comments

Log in or sign up to join the conversation.