- Why do pundits misread the interest rate market?

- Is Fed liftoff the leading indicator it is often made out to be?

- Saudi Arabia severs diplomatic ties with Iran and oil climbs above $38.

- Puerto Rico defaults on some interest payments, but expected to pay G.O.s

Numbers:

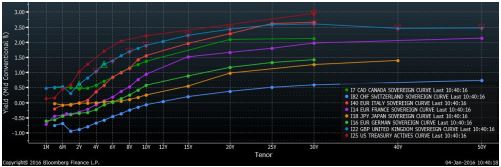

Yield Curves:

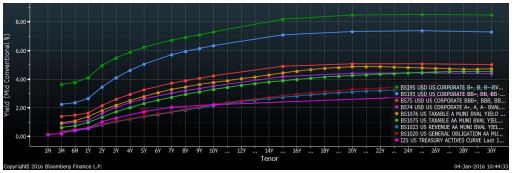

Credit Curves:

Major Currency Exchange Rates:

Making Sense:

Welcome to 2016. As the year begins China economic data disappoints, there is turmoil in the Middle-East and the U.S. Treasury Yield Curve continues to flatten. In other words: Same as it ever was.

The Talking Heads

I could write an entire report discussing the lack of fixed income knowledge in the financial media. However, it really comes down to this: Few in the financial media (or among portfolio strategists for that matter) understand the interest rate market. I have lost count of the occasions that some among the financial punditry latched on to the Fed’s policy rate forecast (a dubious indicator to begin with) to extrapolate where the 10-year UST note might trade later this year, in 2017 and beyond. To assume that the shape of the yield curve will remain largely unaltered as the Fed tightens (to whatever extent it can) is to display one’s ignorance regarding the interest rate market.

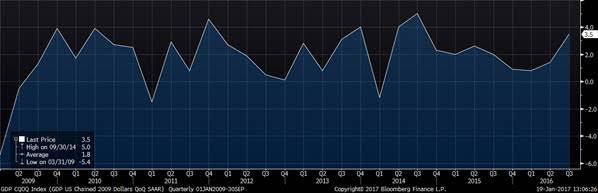

In my view, the Fed has lagged conditions. The Fed is not the dog wagging the tail. It is the tail. Rather than the Fed liftoff marking the time when the economic cycle is on firm footing and ready to accelerate, economic data observed during the past year indicate that the economic cycle is probably past peak. As such, rather than being a leading economic indicator, the Fed is probably behind the economic curve.

I expect the UST yield curve to flatten with short-term yields rising much more than long-term rates. However, as the Fed is unlikely to raise rates far or fast, this means that long-term rates might not move much at all. Keep your eyes on central bankers in 2016. Over the weekend, Fed vice chair, Stanley Fischer stated that the Fed could use interest rate policy to combat “overheated” markets. By stating this, Mr. Fischer is apparently firing a shot across the bows of risk markets. Also, Sweden’s Riksbank warned markets that it is willing to intervene to prevent the Swedish krona from strengthening precipitously versus the euro. Several Scandinavian banks opined that the Riksbank could intervene as long as the krona exchange rate versus the euro is above 9.00. It was about 9.18 at the time of this writing. Stay tuned.

Comments

Log in or sign up to join the conversation.