For anyone who remembers the dot-com boom, it’s hard to believe that former high-flying technology stocks have become today’s solid dividend payers.

But that’s precisely the case for companies like Apple (Nasdaq: AAPL), Microsoft (Nasdaq: MSFT) and Cisco Systems (Nasdaq: CSCO).

These companies (and others) were the clear winners when technology was exploding.

Over the years, they’ve generated so much cash, they’ve had no choice but to pay it back to shareholders in the form of dividends – usually after years of resistance from management.

For example, Cisco was founded in 1984, but didn’t begin paying a dividend until 2011… despite the fact that it’s generated more than $1 billion in free cash flow every year since 1997.

Obviously, the good times have continued for Cisco. Despite a growing list of competitors, it’s still the industry leader when it comes to networking equipment. Its products are the backbone of the internet.

Cisco pays a very respectable 3.4% yield. It’s raised its dividend every year since 2011.

But will it be able to continue to pay and raise its dividend?

A Perfect Track Record

The company’s fiscal year 2016 ended July 25. Results won’t be released until August 17, so let’s look at the prior year.

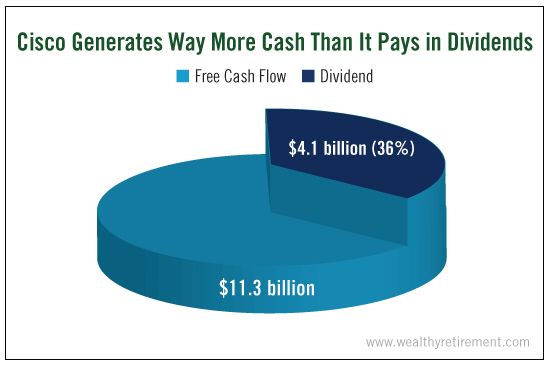

In fiscal 2015, Cisco generated $11.3 billion in free cash flow. It paid out $4.1 billion in dividends for a payout ratio of 36%. That’s well within my comfort zone.

I like to see companies pay shareholders less than 75% of their cash flow in dividends. That way, even if the company has a rough year, it should still have enough cash flow to pay its dividend.

Cisco’s cash flow is projected to rise to $11.6 billion in fiscal 2016.

Despite the higher dividend in the third and fourth quarters, Cisco’s payout ratio should still be well below 50%.

Though its dividend track record is short, it is stellar… annual raises and no cuts.

Cisco generates plenty of cash flow to pay the dividend. It has outstanding management and is expected to continue growing cash flow for years to come.

Not only am I confident that Cisco’s dividend is safe, but I would be stunned if it were cut. Cisco’s dividend is about as safe as you’re going to get.

Comments

Log in or sign up to join the conversation.