The intermediate-term correction in precious metals is getting long in the tooth—but it is not over yet.

We are finally seeing the kind of cleansing you want to see after a major breakout: sentiment has cooled, positioning has washed out, and participation has thinned. But when you line up the historical analogs and drill into breadth, the message is clear: this move likely needs a bit more time and a bit more downside before it fully resets the runway for the next leg higher.

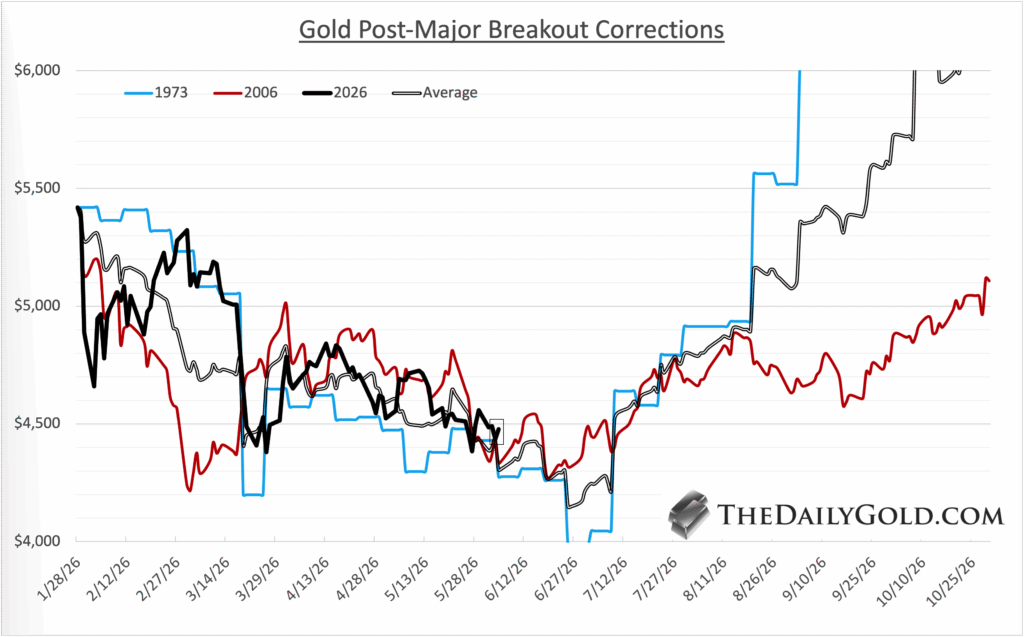

After a major breakout, Gold’s first significant correction has historically followed a clear pattern: a strong impulse higher, followed by a choppy, draining pullback that resets sentiment and positioning without breaking the larger uptrend.

This one is right on script. When you compare it to past episodes, the current move looks like a textbook post-breakout digestion phase that likely needs a bit more time and a bit more downside to fully run its course.

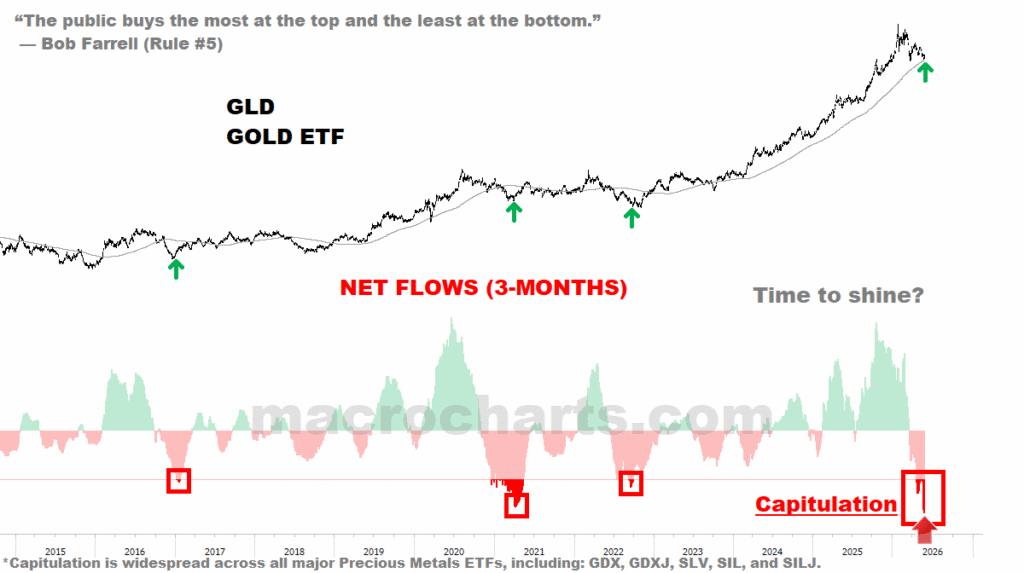

Sentiment is already in the process of resetting. GLD has seen notable outflows in recent months, which is what you want to see during a corrective phase, not at a long-term top.

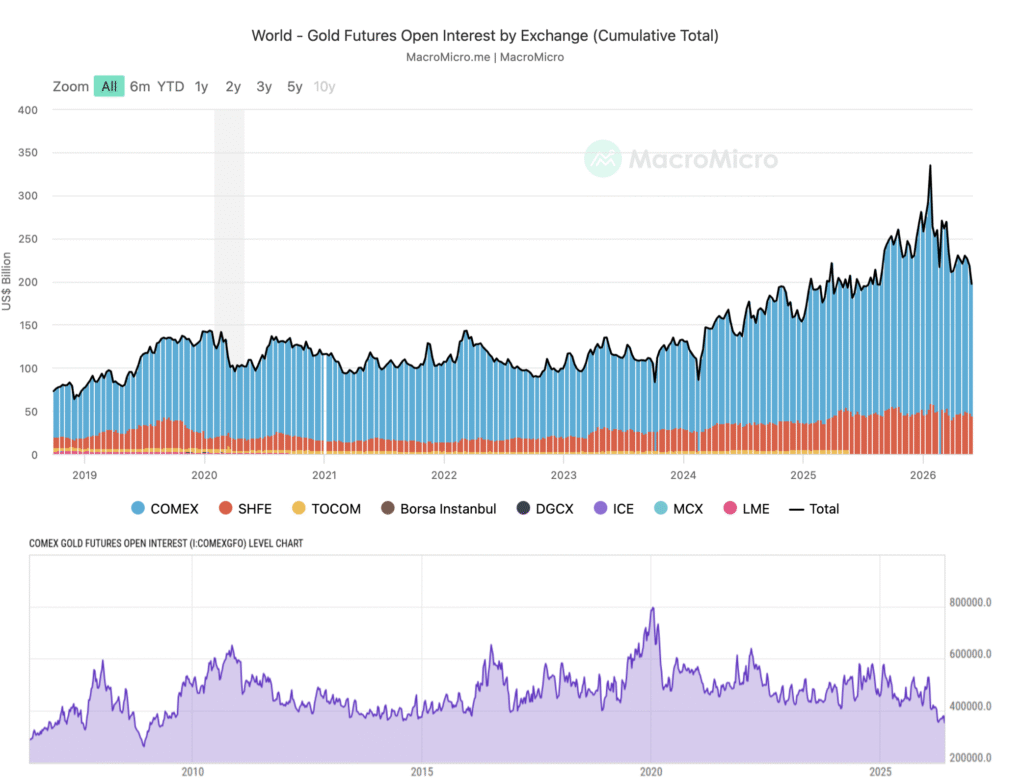

At the same time, open interest has been washed out.

On the Comex, open interest has plunged to a 17‑year low, and even when you adjust for the shift in trading to global exchanges, total global open interest by dollar value has dropped sharply and sits near a one‑year low. That kind of collapse in participation usually reflects speculative money being forced out—important fuel for the next advance.

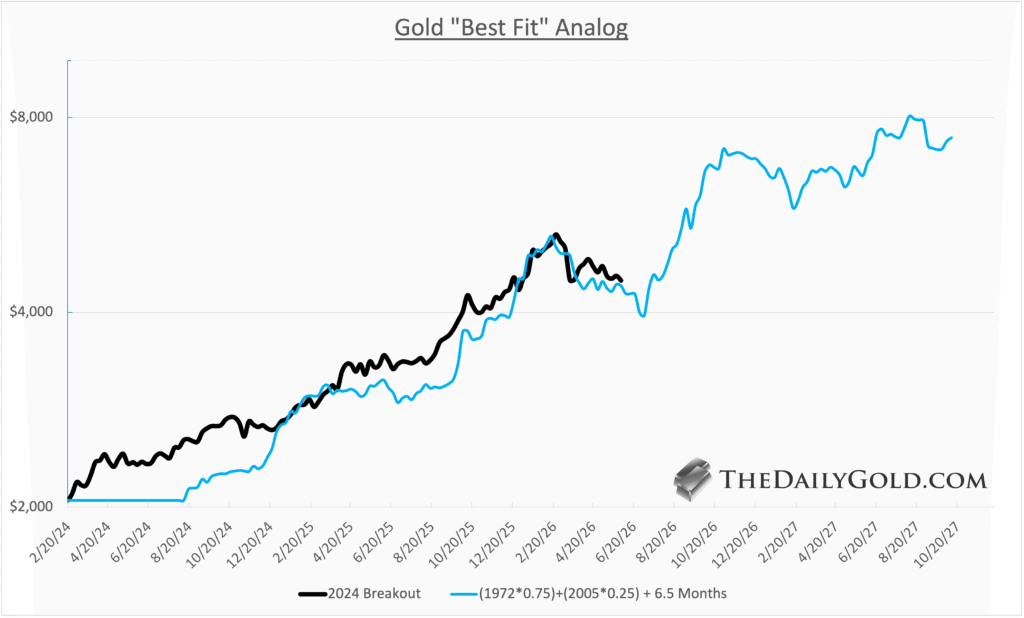

When I map the current breakout move in Gold (which began in February 2024) against history, the “best fit” analog is a weighted composite of the 1972 and 2005 breakouts, shifted forward.

That roadmap easily allows for another leg down—on the order of roughly 10% in Gold—while still preserving the structural bull case.

In other words, more weakness from here would not invalidate the breakout; it would be part of the normal post-breakout process.

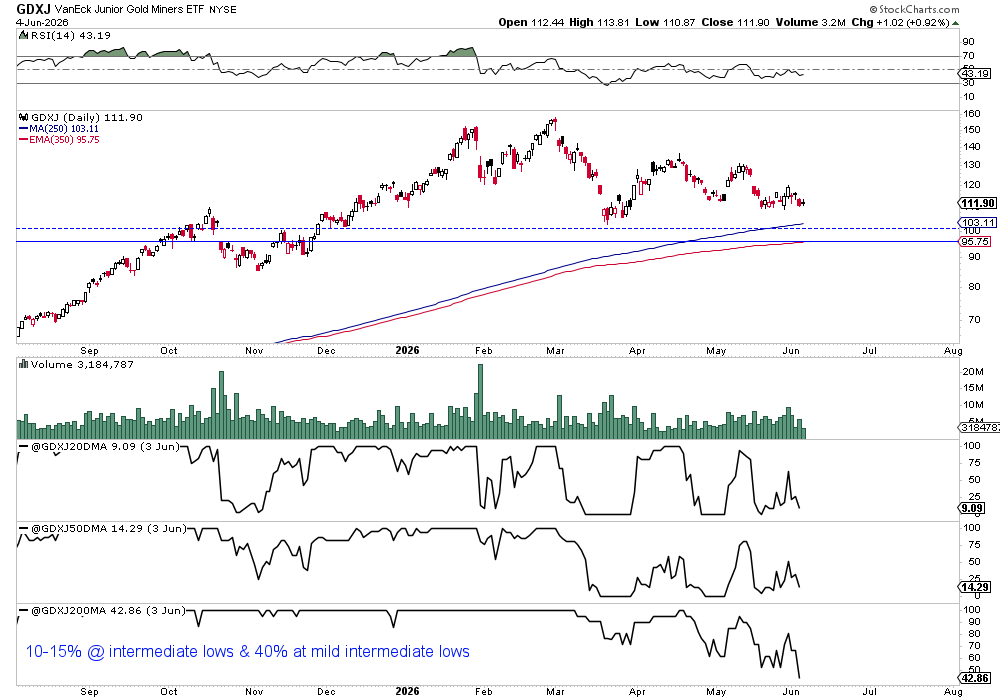

The miners add an important piece to the puzzle.

I track GDXJ alongside breadth data: the percentage of stocks above their 20‑, 50‑, and 200‑day moving averages. The shorter moving averages help with short-term swings, but during maturing, intermediate-term corrections, the 200‑day is the key tell.

In the 2000s, significant lows often formed when less than 20% of names were trading above their 200‑day moving average. Recently that figure was still in the low 40s, suggesting the breadth washout in the juniors is underway but not yet at the kind of washed-out levels that have historically marked the best buying opportunities.

Gold’s correction continues to track prior post-breakout analogs.

Sentiment is resetting, participation has been washed out (open interest collapse), but miner breadth and price action argues for a bit more downside.

Structurally, the backdrop remains firmly bullish. Tactically, though, the evidence still points to an ongoing correction rather than a completed one.

Comments

Log in or sign up to join the conversation.