Learning From a Closed Market “System”

Let us start this article with a simple hypothetical example of 2 market participants which will demonstrate the importance of understanding money in relation to markets. First, some background information:

-

Bob’s portfolio consists of $10,000 in cash (checking deposit), 100 shares of IBM (IBM), and 100 shares of JPMorgan (JPM).

-

Mary’s portfolio consists of $15,000 in cash and 10 Caterpillar (CAT) bonds maturing in 2023.

-

IBM and JPM are both currently trading for $100 per share. Caterpillar’s bonds trade for $100 (or $1,000 per bond).

-

The total value of Bob’s portfolio is $30,000 and the total value of Mary’s portfolio is $25,000.

-

The aggregate portfolio value of market participants is $55,000 and total available market liquidity (cash) is $25,000.

Okay, let’s get started …

JPM has a good earnings release due to consumer lending expansion and Mary wants to buy 50 shares. Bob offers 50 of his shares at $110 and Mary accepts the offer. Assuming IBM shares and CAT 2023 bonds are still trading for $100, this is how things change:

-

Bob’s portfolio consists of $15,500 in cash, 100 shares of IBM and 50 shares of JPM.

-

Mary’s portfolio consists of $9,500 in cash, 10 2023 CAT bonds, and 50 shares of JPM.

-

Bob’s total portfolio is valued at $30,500 and Mary’s total portfolio is valued at $25,000.

-

The aggregate portfolio value of market participants is now a little higher at $55,500 and total available market liquidity is still $25,000.

The Federal Reserve (“Fed”) announces that large banks can resume share repurchases so Mary wants to buy another 50 shares of JPM. Bob offers his remaining 50 shares of JPM at $120 and Mary accepts the offer. Assuming IBM and CAT are still trading for $100, this is how things change:

-

Bob’s portfolio consists of $21,500 in cash and 100 shares of IBM.

-

Mary’s portfolio consists of $3,500 in cash, 10 2023 CAT bonds, and 100 shares of JPM.

-

Bob’s total portfolio is valued at $31,500 and Mary’s total portfolio is valued at $25,500.

-

The aggregate portfolio value of market participants is now higher at $57,000 and total available market liquidity is still $25,000.

The Fed announces a program to start buying corporate bonds. They offer $105 for 2023 CAT bonds and Mary sells all 10 of hers. Assuming JPM is trading for $120 and IBM is trading for $100, this is how things change:

-

Bob’s portfolio consists of $21,500 in cash and 100 shares of IBM.

-

Mary’s portfolio consists of $14,000 in cash and 100 shares of JPM.

-

Bob’s total portfolio is valued at $31,500 and Mary’s total portfolio is valued at $26,000.

-

The aggregate portfolio value of market participants is a little higher at $57,500 and total available market liquidity rises to $35,500.

IBM signs a giant new cloud computing contract. Mary offers to buy 50 shares for $120 and Bob accepts the offer and sells her 50 shares. Assuming JPM is trading for $120, this is how things change:

-

Bob’s portfolio consists of $27,500 in cash and 50 shares of IBM.

-

Mary’s portfolio consists of $8,000 in cash, 100 shares of JPM, and 50 shares of IBM.

-

Bob’s total portfolio is valued at $33,500 and Mary’s total portfolio is valued at $26,000.

-

The aggregate portfolio value of market participants is now higher at $59,500 and total available market liquidity remains at $35,500.

This simple hypothetical scenario which portrays the markets as a closed “system” teaches us several things:

-

Stock prices and stock market capitalization can rise without new money being added to the (closed) market system. If stock prices rise over time for sound economic reasons, then real wealth is created.

-

Within a closed system of investor portfolios (e.g., stocks and bonds) there is no such thing as “cash on the sidelines” being able to fundamentally drive aggregate portfolio values higher since the amount of aggregate cash in investor portfolios stays the same regardless of whether bond and stock prices are rising or falling.

-

The Fed’s bond buying programs, the workings of which I will explain in detail later, is an outside force that can add liquidity to the markets and incremental demand for stocks and bonds.

It is not part of this example, but new debt or equity issuance (new bonds or shares being added to the market) reduces aggregate investor portfolio cash because the cash leaves the system and moves on to the balance sheets of corporations or governments. This means that Fed bond buying, by adding additional money to the market system, can support additional debt and/or equity issuance without aggregate liquidity having to be drained from the market system.

Stock prices can rise for fundamental economic reasons but they can also be influenced higher when new money (liquidity) enters the market system from the broader economic sphere. New money can come from two places: the Fed and commercial bank lending. It is imperative that investors understand how this works.

How The Credit System Works

The accounting equation is:

assets = liabilities + equity

In our double-entry bookkeeping and accounting system, every financial transaction requires an entry on both sides of the equation. To reinforce this, I will refer to these as double-sided accounting entries throughout the remainder of this article.

If I put 20% down to buy a $400,000 house, then my personal balance sheet would look like this after this transaction:

$400,000 (fixed asset) = $320,000 (mortgage) + $80,000 (owner’s equity)

Over time, as I earn income and pay down the mortgage, the asset side of my equation will stay the same (assuming the market value of my home remains the same), my mortgage liability will decrease, and my owner’s equity will increase.

At a high level, the process works the same for a business. Capital is raised for the business in the form of borrowing (debt liability) and equity (owner capital contributions). The business operates to generate returns on this capital.

We have to think about this accounting equation differently for banks. For banks loans are assets and deposits are liabilities. People think when they put money in a checking or savings account that the bank segregates their account and their money just sits there, perhaps earning interest, until they want it. In reality, their deposits are loans (capital) for the banks to extend credit against. This is why banks advertise gift cards, higher rates, etc. for people to deposit money with them. This is a low cost form of capital for them. To understand how modern banks operate it must be clear in our minds that deposits are liabilities.

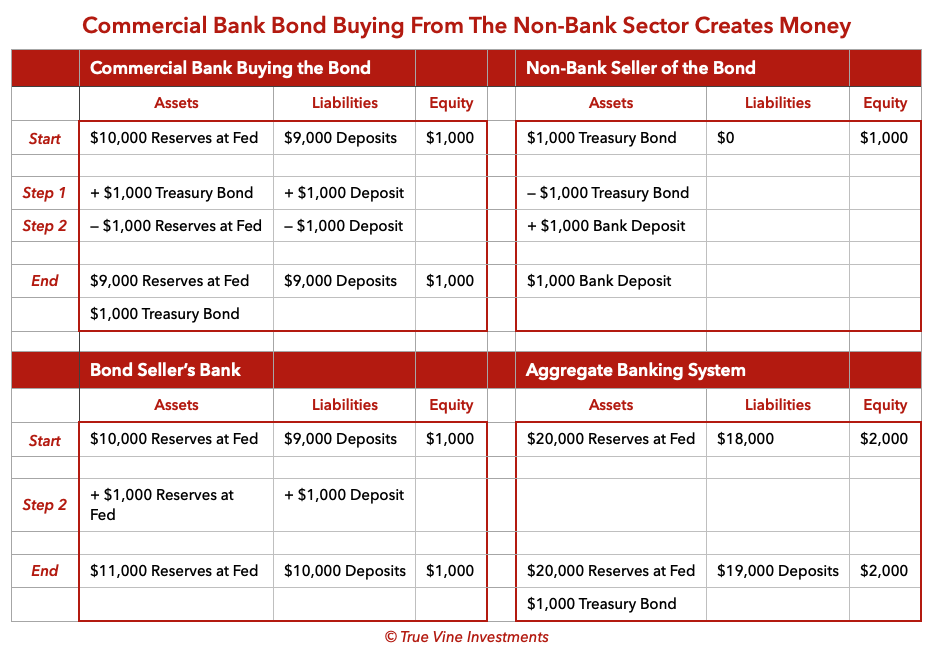

When a bank makes a loan or buys securities from the non-bank sector an electronic double-sided accounting entry is made that literally creates money out of nothing. When a bank buys a U.S. Treasury bond this becomes an asset on its balance sheet. The bank does not transfer its own cash to pay for this bond. The double-sided accounting entry creates a new deposit liability for the seller of the bond. Let me explain how this works using the example of a bank buying a $1,000 Treasury bond from a non-bank seller. The table below is a companion to this explanation.

Step 1

Upon buying the bond, the buying bank adds the $1,000 Treasury bond to assets and creates an offsetting $1,000 deposit liability for the seller.

Step 2

Assuming the seller of the bond banks elsewhere and thus wants the proceeds in his existing checking account, the bond buying bank will transfer $1,000 of Reserves at the Fed to the bond seller’s account at his bank.

(Click on image to enlarge)

Here we can see that by buying this bond, the aggregate banking system expanded its balance sheet and created $1,000 of bank deposits out of nothing.

When a bank makes a loan. It credits the asset side of its balance sheet with a loan receivable and creates an offsetting deposit liability for the borrower. The amount of the loan is electronic money that is literally created out of nothing. If the borrower is immediately using the funds to make a purchase, such as a home or car, or simply banks elsewhere as in the previous example, then the lending bank would transfer Reserves at the Fed to the bank of the person selling the home or the car dealer selling the car and their bank would take on the deposit liability. Here we see that by making loans, the aggregate banking system expanded its balance sheet and created the amount of the loan in new bank deposits out of nothing.

If this bank accounting and credit creation process is all new to you, then you can now begin to understand why banks are so heavily regulated. The power to create money out of nothing is a public trust.

Before moving on, it is important to point out that these credit creation processes also work in reverse. If a bank sells assets or if a loan is partially or fully repaid, then money will be destroyed (removed) from the banking system.

An Effective Definition of Money

The Federal Reserve issues coins and paper money to the commercial banking system but this amounts to less than 5% of the overall money supply. As you learn how the banking system operates, you come to realize that it is really a system of electronic accounting credits. Physical money is becoming extinct. This is what some expert economic commentators mean when they say that we really do not have money anymore.

Contrast the following two quotes which occurred almost 100 years apart and both before the U.S. Congress:

“Money is gold, nothing else.”

—John Pierpont Morgan (before Congress in 1912)

“No. It’s not money, it’s a precious metal …”

—Ben Bernanke (before Congress in 2011) when asked, “Do you think gold is money?”)

J.P. Morgan understood that only gold is really money because everything else is a claim against someone else’s liability. J.P. Morgan would have probably acknowledged silver as money also, but the wealthiest, like King Solomon, only concern themselves with gold. (A neat example: we read “A Christmas Carol” to our children at Christmas time. J.P. Morgan read to his from Dickens’ original manuscript.) Ben Bernanke is a priest of the modern temple of electronic credits. I have argued that only gold and silver are true money because the supply was determined by God. J.P. Morgan would have probably agreed with me.

The problem with our modern monetary system of electronic credits is that we are all forced to participate in it to conduct commerce and doing so means a loss of economic freedom and privacy. This is the path that the Bible has already forecasted.

While understanding the inherent flaws of this system we are forced into, it is needful to have a workable definition of modern “money” as an investor. Thus, I view money as (1) the remaining physical stuff circulating in the economy (not held by the Fed) and (2) the deposit liabilities of the commercial banking system that are immediately available for use (not time deposits like CDs). This is essentially the same as the Fed’s M1 monetary measure also referred to as “narrow money.” This definition embodies money in its narrowest sense—a medium of exchange geared toward transactions that is not savings or investment. It is a good measure for analyzing economic activity. It is also a good measure for contrasting money with securities that trade in the markets.

Savings deposits are included in the Fed’s broader M2 measurement. One can make a strong case for including savings deposits in my money definition since payments can be made from savings deposits (with some restrictions) and they can also be withdrawn for physical cash. I really have no argument with this. The strongest case for this is the fact that they do not have to be sold to be used as money. That is, no one else has to give up money for savings deposits to be used as money. I prefer to exclude them though because I believe they still have more of a savings component to them, especially when we actually have interest rates, and are thus longer term in nature. My financial advisor experience confirms that these are genuinely viewed as savings in the sense that they are a safer investment alternative to stocks. Backing this up is the fact that there is now almost $12 trillion in savings deposits. This is not “money” that individual Americans or businesses are using for everyday transactions. When they are employed for everyday transactions—withdrawn as cash or transferred to a checking account—then they are captured in my money definition.

It is also tempting to include short-term money market securities, held by market participants as an alternative to interest bearing deposits, as money, however, in order for holders of these securities to use them as money someone else has to give up their money to buy them.

This last point embodies my thinking on money. I prefer to separate it from savings or investments (financial assets). This helps aid the important understanding that increases in financial assets (namely, stocks and bonds) withdraw liquidity (money) from the markets. Markets are driven by liquidity. This takes us back to the example at the beginning of this article and the conclusions I made there. Markets are influenced up and down by the addition and subtraction of liquidity (money as I defined it).

I have now laid the foundation for us to understand the impact of Federal Reserve bond buying on the markets.

Federal Reserve Bond Buying

In its last Federal Open Market Committee (FOMC) meeting statement, this important Fed committee noted the following:

In addition, over coming months the Federal Reserve will increase its holdings of Treasury securities and agency mortgage-backed securities at least at the current pace to sustain smooth market functioning and help foster accommodative financial conditions, thereby supporting the flow of credit to households and businesses. (emphasis mine)

It is critical to understand what this Fed bond (security) buying means for the economy and markets. There is broad confusion amongst the professional investment community regarding the details of just what exactly this entails and the impact it has on the economy, money supply, and markets.

Fed bond buying is conducted by the New York branch through a number of authorized Primary Dealers. The NY Fed sends its instructions to these Dealers who act as intermediaries to source the bonds from banks and non-bank financial institutions, such as mutual funds, hedge funds, life insurance companies, pension funds, and other large institutional investors. It is necessary to specifically distinguish between banks and non-bank financial institutions because the effect on the economy, money supply, and markets can differ depending upon who is selling their bonds to the NY Fed (through the Dealers).

Before continuing, let me just pause to point out that U.S. commercial banks are “connected” to the Federal Reserve branches around the country (what we call the Fed is really the aggregate of a network of branches). By connected, I mean that commercial banks hold reserve balances (deposits) with the Fed that are used to settle payments between banks. For example, if JPMorgan Chase’s customers have net intraday demand of $10 million from Bank of America (BAC), Bank of America can simply transfer $10 million of their reserves at the Fed to JPMorgan Chase’s reserve account at the Fed. The Fed also supplies coins and currency to banks so commercial banks can exchange some of their reserves at the Fed for additional amounts of coins and currency that they may need to satisfy customer demands.

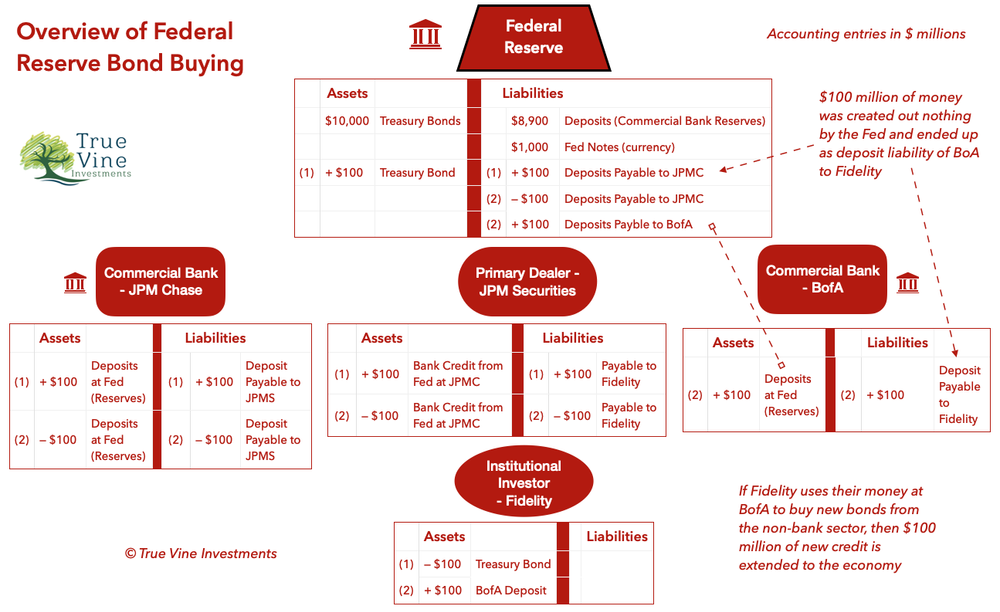

I am going to now take readers through an example of what happens when the Fed buys a $100 million Treasury bond that ultimately comes from an Institutional Investor and not a bank. In this example, JPMorgan Securities (JPMS) is the Primary Dealer. JPMorgan Securities’ bank is JPMorgan Chase (JPMC). The Institutional Investor is Fidelity and Fidelity’s bank is Bank of America (BofA). This example is detailed in the “Overview of Federal Reserve Bond Buying” diagram below. It shows the impacts on the balance sheets of the different entities and from this we can begin to understand the impacts or potential impacts to the economy, money supply, and markets. (Note: the diagram shows some hypothetical initial balance sheet accounts for some of the entities as a reference. These initial amounts are not mentioned in the example explanation.)

Step 1

The NY Fed contacts JPM Securities (a Primary Dealer) and tells them they want to purchase $100 million of U.S. Treasury bonds. JPMS corresponds with its customers and ends up finding a seller in Fidelity. Upon confirmation from JPMS, the Fed creates an asset entry on its balance sheet for the $100 million Treasury bond and then adds a corresponding $100 million deposit payable to JPMC (JPMS’ bank) on the liability side of its balance sheet. JPMS gets a $100 million deposit account credit from the Fed but it also has a $100 million liability to Fidelity for the Treasury Bond.

Step 2

JPMC transfers $100 million of its reserves at the Fed to BofA’s reserve account at the Fed. To complete the double-sided accounting entries at JPMC and BofA the $100 million deposit liability moves from JPMC (for JPMS) to BofA (for Fidelity).

(Click on image to enlarge)

To summarize this example, there are essentially 2 main steps to the Fed’s bond buying. In step 1, the Fed literally creates money out of nothing and credits the Primary Dealer’s bank account at the Fed. In step 2, the Primary Dealer’s bank transfers the proceeds of the sale to the bond seller’s bank (assuming it is a different bank).

What then is the net result of the Fed buying a $100 million U.S. Treasury bond from Fidelity? $100 million of new commercial bank deposits are added to the aggregate banking system. If Fidelity uses the $100 million to buy another bond, such as a corporate bond, then $100 million of new credit is extended to the economy.

If Fidelity just continues to hold the bank deposit and does nothing with it, then no new credit is extended to the economy. The money supply will have expanded by $100 million but there is no impact on the economy if Fidelity does not do anything new with the proceeds of its bond sale.

In this example, the Fed purchased the bond from a non-bank entity, Fidelity. The Fed buys bonds through the Primary Dealers from the broader market so some purchases also come from the banking sector which holds a lot of Treasury bonds. If a commercial bank, like Bank of America, would have sold the $100 million Treasury bond to the Fed, then the net effect would have been that the money supply would not have increased. In exchange for its bond, BofA’s deposits at the Fed (Reserves) balance would have increased by $100 million but aggregate commercial bank deposit liabilities apart from the Fed would not have. If Bank of America replaced the $100 million Treasury bond by purchasing a $100 million Treasury bond from the non-bank sector, then $100 million of new credit would have been extended to the economy.

We can thus see that Fed bond buying extends new credit to the economy and increases the M1 narrow money supply when any entity the Fed buys the bond from replaces it with another bond from outside the commercial banking system.

Alternatively, as long as the bond buying stays within the commercial banking system, then new credit is not extended to the economy. Furthermore, commercial banks can make loans as they see fit as long as they stay within their regulatory thresholds. They do not need more Reserves (deposits with the Fed) to be able to make more loans. Actually, the amount of Reserves at the Fed is really determined by the amount of daily interbank settlements which are in turn driven by the amount of new loans being made by the commercial banking system (remember, new money is created when banks make loans).

Addressing Misunderstandings

At this point, I must address several common misunderstandings about what the Fed is actually doing by buying bonds.

#1 - Quantitative Easing (QE) is just a commercial bank asset swap increasing useless Reserves

This argument is right when it says more Reserves at the Fed for commercial banks is not a stimulative policy but wrong in that U.S. Fed bond buying is limited to the commercial banking system.

The commonly used term for Fed bond buying is Quantitative Easing. This term was invented by Richard Werner. The book, Where Does Money Come From?, which he co-authored with Josh Ryan-Collins, Tony Greenham, and Andrew Jackson, explains that Werner originally defined Quantitative Easing as expanding credit creation, however, the well-known Japanese use of the policy which started in 2001 was only one of expanding bank reserves. The authors explained:

This policy was also ineffective, but thanks to using a label originally defined as expanding credit creation—’quantitative easing’—it caught the imagination of investors and commentators. Thus today often monetarist reserve or base money expansion is referred to as ‘quantitative easing’, or QE.

Unlike the Bank of Japan, the Federal Reserve implemented a policy more directly aimed at expanding bank credit creation, as explained by Chairman Bernanke. This paid off in 2012 as bank credit growth recovered.

The Fed’s bond buying is actually the real credit creating Quantitative Easing that Werner originally defined. However, what has apparently happened though is that market commentators are wrongly comparing it to the failed “QE” policy of the Bank of Japan but it is not exactly the same policy! Fed bond buying frequently goes directly to the non-bank sector and actually does what the last FOMC statement says by “supporting the flow of credit to households and businesses.” A more appropriate name for the Fed’s bond buying policy would be “Credit Expansion”.

#2 - The Fed is printing money

When most people refer to “printing” money they are talking about the Fed creating new electronic money. The Fed is not printing physical dollars, however, over time the effect of its bond buying could result in increased demand for physical currency.

Is the Fed really printing money like Jay Powell told 60 Minutes this year? The answer is nuanced. Using my definition of “modern” money which matches the Fed’s M1 narrow money definition, the Fed is technically sometimes creating new electronic money when it buys bonds from the non-bank sector. When they buy bonds from the commercial banking sector and those banks subsequently buy new bonds from the non-bank sector, then those banks are creating new electronic money. So the Fed is sometimes creating new money but not always creating money and some of the new money is being created by the commercial banking system and not the Fed.

If the Japanese policy was or still is indeed strictly limited to creating bank Reserves, then the Bank of Japan is not printing money at all. However, I would assume that the Japanese commercial banks were replacing bonds from those outside of the banking sector (held by the non-bank sector) which would create new money.

Comments

Log in or sign up to join the conversation.