One of the most common and misleading stock market metrics is the Price to Earnings or P/E ratio. Value investors frequently focus on this metric in their search for cheap stocks. Indeed, too many investors put too much emphasis on this metric and it causes them to make mistakes.

Nobody knows this better than me because I made this mistake for a long time. I frequently bought stocks because they had low P/E ratios and shorted stocks with high P/E ratios only to find the former go down over time while the latter frequently went higher. Why?

The basic reason that the P/E ratio can be misleading is that it focuses on only one year of earnings. Every introductory finance student knows that the intrinsic value of a stock is all of its future earnings discounted back to the present using an appropriate discount rate.

In other words, you need to take a long term perspective when valuing a business rather than focusing on only one year as the P/E ratio does. Failing to do so can cause you to overlook some of the more substantive factors that make up a stock’s intrinsic value.

One common mistake a low P/E ratio causes value investors to make is to invest in value traps. A value trap is a stock trading at a low P/E for a good reason: its business is in permanent decline.

I learned this lesson the hard way a number of times, including failed investments in Tailored Brands – owner of Men’s Warehouse and Joseph A. Abboud – as well as generic drug maker Teva. While these stocks looked cheap on current year earnings, they were actually value traps because the businesses were in decline resulting in lower earnings in the out years not considered by the P/E ratio.

The corollary mistake is to assume that a stock with a high P/E ratio is expensive or overvalued. Certainly this is the case sometimes. But sometimes a high P/E ratio is due to the company having a lot of growth ahead of it and/or a high quality of earnings. By a high quality of earnings, I’m talking about a company with a durable competitive advantage that results in sustainable earnings power over a long period of time. Growth and quality are frequently worth paying up for.

One stock I made this mistake with over the years was Palo Alto Networks. PANW always looked expensive when I focused on the current year P/E but because of its high growth and the quality of its business it more than grew into its valuation and its stock has been a big long term winner.

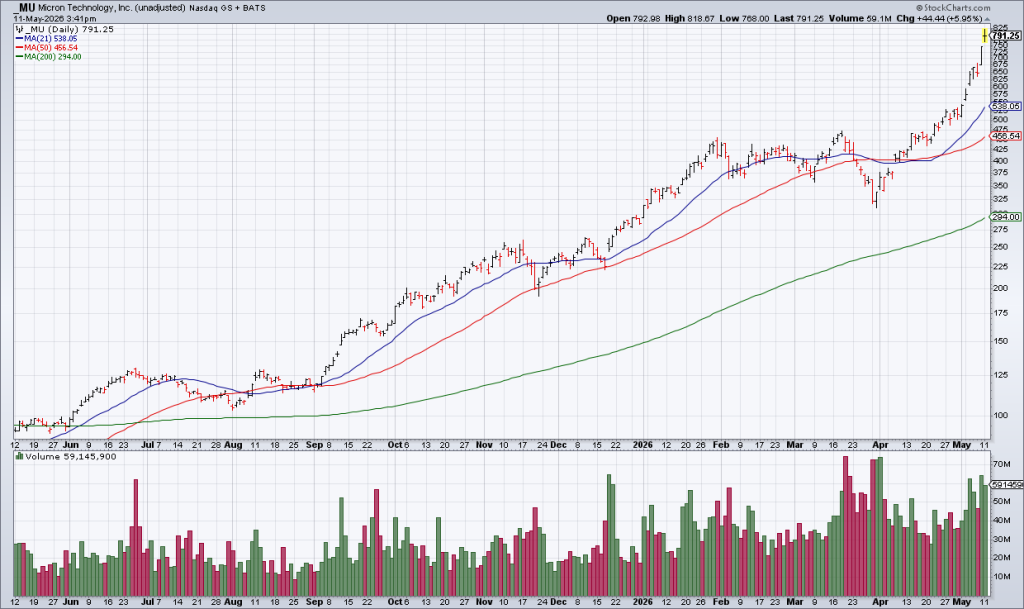

Which brings me to the hottest and most seductive stocks in the market right now: the memory chip makers Micron (MU) and Sandisk (SNDK). I see a lot of investors on Twitter arguing that these stocks are cheap even after the massive runs they’ve had. The argument is that the P/E ratio is still in the single digits.

What this argument ignores is the cyclicality of their businesses. These companies are notoriously cyclical but investors are acting like peak earnings are sustainable over the long term. If this time is really different and they can maintain – and even grow – their current earnings over the long term, then they are in fact cheap.

More likely, however, is that the high prices for their products will result in new supply as well as customers finding substitutes which will lead a significant drop in their earnings. In other words, current earnings are not sustainable and, if history and the laws of economics are any guide, are likely to fall off a cliff sometime soon. Such an eventuality would reveal the shallowness of arguments that rely solely on the P/E ratio.

That’s not to say that these stocks can’t continue going up. Stock prices frequently diverge from intrinsic value. But to argue that they are cheap requires more than pointing to a low P/E ratio. Many will learn this the hard way – just like me.

Comments

Log in or sign up to join the conversation.