Valuation doesn’t matter; until it does. The path to being a great investor is to ignore the short-term and focus on long-term risk and reward. The markets don’t always correct immediately, but over the long-term, gravity can knock high-flying stocks out of the sky.

Netflix is in a giant bubble right now. I feel 100% confident making that assertion. The upside to owning the stock at this point is virtually nil. There’s almost a 0% chance the company could conceivably meet the market’s current valuation for it. Conversely, the downside risks are huge. In a pessimistic scenario, the stock could lose 80% - 90% of its value. Netflix is a great company. I can sing the praises of Reed Hastings all day long. As a stock, however, buying NFLX in March 2018 is insane.

How overvalued is NFLX? Even with a 50% haircut, there’s still a compelling argument that it would be extremely overvalued. NFLX is in 1990’s Tech Bubble territory. Buying Netflix in 2018 is like buying Microsoft or Oracle in 1999. If you buy-and-hold for 20 years, it’s completely possible that the 2038 stock price is the same as the 2018 stock price. That’s how big of a bubble this is.

To showcase how absurdly priced Netflix is at the current levels, let’s try to reverse engineer NFLX’s current valuation.

US Revenue Growth

As I write this article, the current NFLX stock price is at $322 and the Enterprise Value is at $148 billion. In order to value NFLX, there are two huge questions we have to answer:

(1) How many subscribers will NFLX have in 10 years?

(2) What will NFLX’s profit margins be in 10 years?

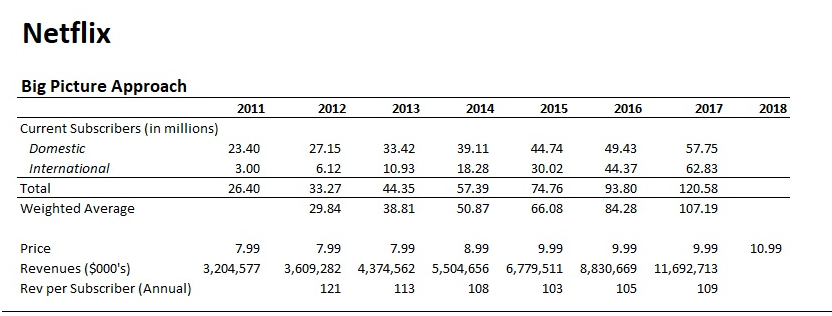

To examine the first question, let’s first look at subscriber growth. Over the past 6 years, NFLX has grown US subscribers from 23 million to 58 million. International subscribers have increased from 3 million to 63 million.

(Click on image to enlarge)

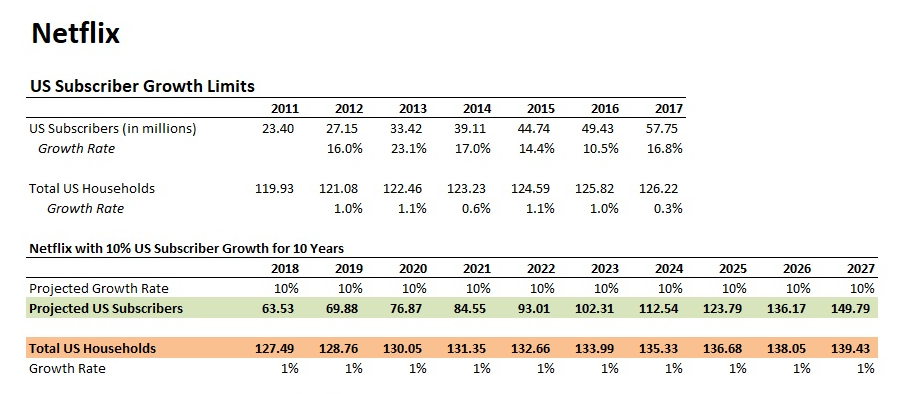

Those are impressive numbers, but where’s the saturation point? I have to assume we’re closing in on it in the US. According to the US Census Bureau, there are about 126 million households in the US. Netflix has already captured almost 50% of the American market! While NFLX had mid double-digit growth for 2017, it’s difficult to imagine this trend lasting too much longer. You can see this showcased dramatically in the chart below that projects a 10% US subscriber growth rate versus a 1% US household growth rate (in line with levels over the past decade). By 2027, with a projected 10% growth rate, NFLX’s projected subscribers would actually exceed the number of US households!

(Click on image to enlarge)

Needless to say, NFLX’s US growth will have to slow down sometime soon. There’s no realistic case where a large number of households are subscribing to NFLX twice. For US growth, it’s best to make an estimate of penetration level NFLX can achieve over the next 10 years and estimate revenues based on that. In an optimistic case, I think we could assume that eventually 80% of US households have NFLX. This would put us at about 110 million US subscribers by 2027. In a more pessimistic case, we might say 70%, which would give NFLX 98 million US subscribers. Either way, the US subscriber picture is relatively straight-forward. The bulls and bears probably aren’t that far apart on this particular assumption.

International Revenue Growth

International growth is much trickier to forecast. As the US market becomes saturated, international is clearly NFLX’s best avenue for growth, but what are the limits? The data for international households is less reliable. Based on data (some of which is outdated) on Wikipedia, I’m estimating somewhere in the realm of 1.5 billion households (outside of the US) globally.

It should immediately be noted that around 40%+ of those households are split between China and India. You can get Netflix in Bosnia-Herzegovina, but statistically speaking, with about 1 million households in Bosnia, the growth is going to be limited from these smaller countries like Bosnia, Azerbaijan, and Uruguay. Netflix is already in India, but without China, that leaves about a quarter of international households outside of NFLX’s reach. Many international markets are also going to be much more difficult for NFLX to win or obtain rights in, so we know that NFLX will never achieve an international household penetration rate anywhere close to the US rate, but predicting the “upper bound” is a tricky task.

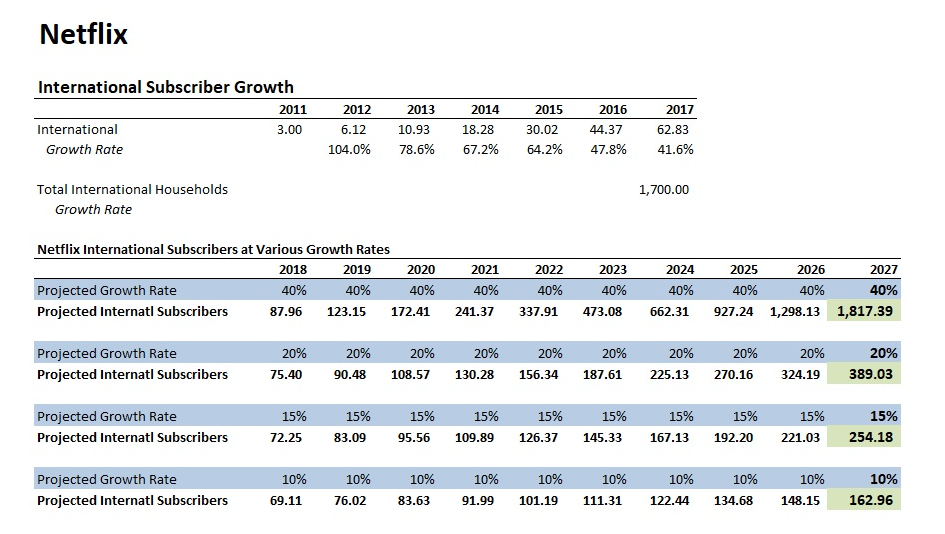

Instead of trying to find a “saturation point”, I think it’s best to apply various growth rates to the current international subscriber numbers and forecast out for 10 years. The current international growth rate is around 45%, but this is unsustainable, as quickly becomes apparent in the chart below. With a 40% international growth rate over the next 10 years, NFLX will eventually surpass the number of international households. So once again, we have to assume that NFLX’s growth rate will taper off significantly since it’s statistically impossible for it to continue at the current rate for another 10 years.

(Click on image to enlarge)

While it’s extremely difficult to project NFLX’s international growth rate out a decade, let’s go with an optimistic 20% growth rate. That would put it at 390 million international subscribers in 2027, which would be somewhere in the realm of a 20% - 25% penetration rate for households outside of the US. This strikes me as optimistic, but since we’re looking for the “best case scenario” assumptions, we’ll go with it.

In a more moderate-case and pessimistic-case scenario, we might go with a 15% and 10% growth rate, respectively, but I don’t have huge qualms with projecting anywhere from a 15% - 20% international growth rate for NFLX over the next decade.

Total Revenues

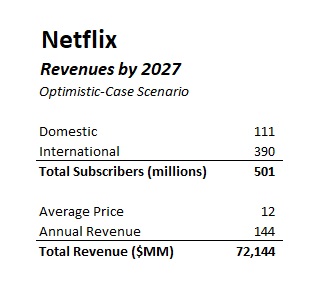

With all that information, we can look at a best-case scenario for Netflix on revenues. With approximately 500 million subscribers, Netflix would generate somewhere in the realm of $72 billion in revenues in 2027 in our optimistic-case scenario. For comparisons’ sake, NFLX generated about $11.6 billion in 2017, so we are assuming that revenues will increase 6-fold in 10 years under this scenario.

(Click on image to enlarge)

Now it’s time to look at costs, which continue to be a major issue for Netflix.

The Cost Picture

Few would doubt that NFLX has strong revenue growth prospects over the next 10 years. The “bear case” isn’t really built around revenues, albeit, revenues could still underperform expectations. Rather, the bear case is centered more on NFLX’s troubling cost picture.

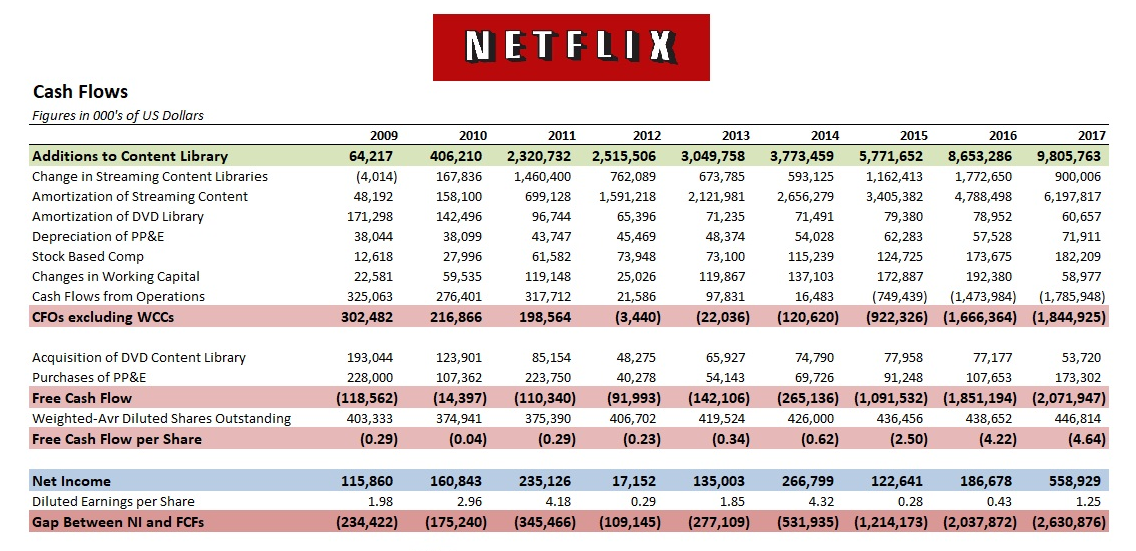

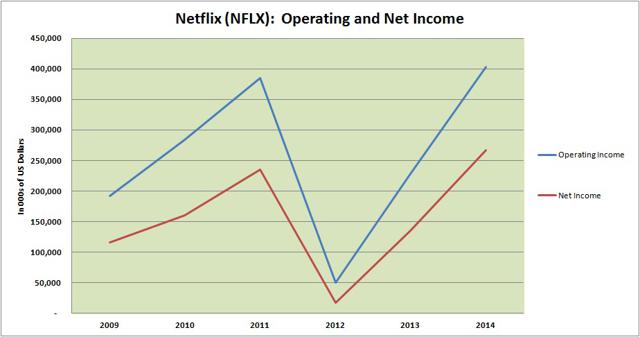

Below you can see Netflix’s cash flow statements over the past 9 years. While NFLX’s Net Income has continued to increase over the past few years, its cash flows have been in a rapid decline. NFLX’s Net Income was $559 million for FY2017, but Free Cash Flows were $2.1 billion in the red. The gap between Net Income and Free Cash Flows is now over a quarter of the size of NFLX’s entire revenues and is largely explained by “Content Library Additions.”

(Click on image to enlarge)

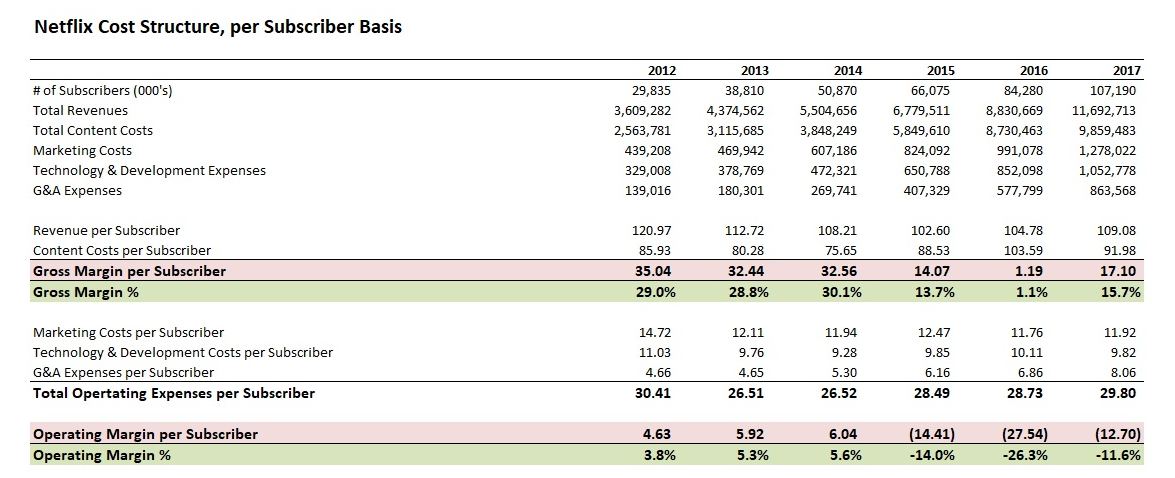

Moreover, there’s increasing evidence that streaming has become a less profitable endeavor for NFLX over time. In the table below, I examine the revenues and costs on a per subscriber basis. In 2012, NFLX generated about $35 in gross margin per subscriber. In 2017, that number had fallen to $17. This is merely looking at content costs; once you factor in operating costs such as marketing, technology, and G&A, NFLX’s operating margin per subscriber has fallen from $4.63 in 2012 down to -12.70 in 2017.

(Click on image to enlarge)

There is, of course, the argument that NFLX has to spend more money as it grows its subscriber base and the costs will become more controllable once NFLX becomes a more mature company, but I have difficulty fully buying into that argument. If anything, it appears that content creators (e.g. film and television studios) significantly underestimated the value of their assets during the early days of streaming. While there’s a lot of volatility in the numbers, the overall trend is that NFLX is paying more for content costs per subscriber than they were in the past. Content creators demanding a bigger share of the pie is a major reason why NFLX’s cash flows have fallen deeper into the red over time.

The Full Picture: An Optimistic Valuation

I’m reasonably optimistic about NFLX’s revenue prospects, but somewhat pessimistic about its cost structure. This isn’t merely an issue of “economies of scale” where NFLX will exceed a certain threshold and everything is pure profit. Rather, the content creators will continue to demand a bigger share of the pie as NFLX’s revenues continue to increase.

That said, this is our “Optimistic Case Scenario”, so we need to come up with something like a best-case scenario for NFLX on costs. Even during “the best years”, NFLX’s profit margins were in the 6% - 8% range. Let’s say NFLX could somehow find a way to generate 20% operating margins; factoring in taxes that comes out to about 15% profit margins. I don’t believe this will happen, but for argument’s sake, let’s see what a valuation might look like.

If we assume NFLX generates $72 billion in revenue in 2027 with 15% profit margins, its Net Income would be about $10.8 billion. If we apply a P/E multiple of 20x to that Net Income, we come up with an Enterprise Value of $216 million for 2027. Netflix’s current EV is $148 million. If we subtract out the debt, that would be a 4.0% annual return on the stock.

4.0% annually is not horrendous, but let’s be clear: this is the pie-in-the-sky super-sunny optimistic scenario valuation and we’re still only getting 4%! The current yield on 10-year treasury bonds is 2.9%. The current yield on the highest rated US corporate bonds is around 3.8%. 4% is terrible for an upside scenario.

The assumptions underlying this valuation are 80% US penetration rate (may not be realistic), 20% international growth for the next 10 years (also may not be realistic), 20% in price increases (could be realistic), and 15% profit margins (almost certainly not realistic). And in spite of that amazing projected growth, you would still only achieve roughly the same returns as you would buying high-grade corporate bonds. That’s a very bad deal.

Backing Into a Fair Value

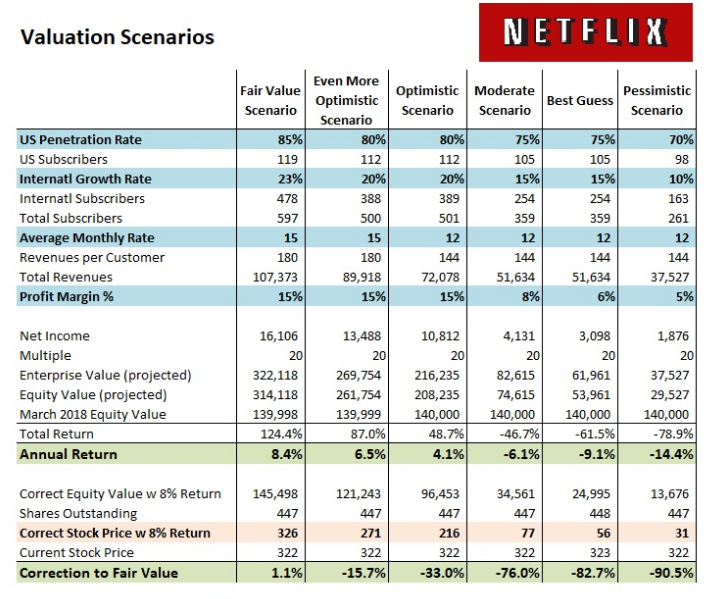

Yet, even with our pie-in-the-sky assumptions, we still came short of fair value with the current stock price. Assuming that investors demand a return of at least 8% on NFLX’s stock, even our optimistic case suggests that the stock is currently 50% overpriced. So how extreme in the assumptions do we have to go for the stock to currently be fairly priced? You can see the data from all 6 valuations scenarios I ran below.

(Click on image to enlarge)

In order to hit “fair value” based on an 8% return, which is still quite low by historical standards, I had to use the following assumptions:

(1) 85% US household penetration rate --- current rate = 46%

(2) 478 million international subscribers by 2027 --- current number = 63 million

(3) 20% cash operating margin (25% taxes) --- current margin = -12% (that’s a negative sign in front)

(4) $15 average revenue per customer --- current average = $9

Nothing about this seems remotely realistic to me and I’m still being pretty conservative in the return assumptions by saying that 8% is the required rate of return. There’s almost no chance that NFLX can achieve these results.

More Realistic Scenarios

Now that we’ve gotten the extremely optimistic scenarios out of the way, let’s look at some more realistic scenarios. A 75% US penetration rate seems reasonable. I’m optimistic about Netflix’s international growth, but 15% annual growth seems more reasonable over a 10-year timeframe. While I’m pessimistic about the cost picture, let’s assume NFLX can generate a reasonable 8% profit margin by 2027. Though, in my opinion, 3% - 6% is more realistic.

With these assumptions, and assuming an 8% required rate of return, NFLX’s stock price should be at $77. That’s a 76% haircut from its current price of $322. If we use a more conservative 6% profit margin, that drops down to $56. In a pessimistic scenario where revenue growth is also lower than expected, I come up with a valuation of $31 per share.

Netflix is insanely overvalued.

Why the Future Could Have More Competition for Netflix

While it’s reasonable to be optimistic about NFLX’s business prospects, I do think there are also some potentially bad events on that front, as well. Let’s start out by pointing out that NFLX is having an increasingly difficult time holding onto content. You can visually see this by hopping on over to Flixable and looking at the stats. NFLX had 7,300 movies available for streaming in 2010, but only 5,600 in 2018. The number of TV shows has grown to somewhat offset that, but the overall trend is that NFLX is selling a smaller amount of content at higher prices.

Disney is the 800 pound gorilla in the content world. Consider all the assets Disney owns right now including Walt Disney studios, ABC, ESPN, and A&E. Disney also recently acquired Fox studios and owns Marvel Entertainment. Out of the top 300 revenue generating movies of all-time, Disney owns the rights to a respectable percentage of them. A Disney streaming service could be a major competitor to Netflix. Netflix has dismissed the Disney threat as ‘no bigger than Hulu’, but this strikes me as naïve as believing that Netflix wasn’t a threat to Blockbuster. Content is king and Disney is the king of content.

Then there’s also the issue of whether people will become more selective in their subscriptions. Netflix and Hulu were the first on the scene in streaming so the early adopters flocked to them, but with dozens of streaming services out there, it’s not unreasonable to suggest people might get more selective. The whole point of “cutting the cord”, after all, was to save money and not simply pay for a bunch of stuff you didn’t want (as you were with cable). I don’t think the majority of Americans are going to be willing to shell out $100 for 5-6 streaming services. And Netflix will be on the chopping block for some American consumers at some point.

None of this is to suggest that Netflix isn’t well-managed and can’t adapt to the market. If anything, Reed Hastings has proven himself to be one of the best CEOs in the country, but he’s a great CEO in an increasingly competitive industry with negative cash flow margins.

It’s also difficult to project Netflix’s international prospects. They appear to be doing quite well now, but every country is a bit different when it comes to content rights, and they will likely find some markets where they can’t be that competitive. Like the US market, Netflix also has to hit a saturation point eventually internationally. I don’t think there’s a realistic scenario where NFLX is in 50% of households internationally. Even 300 to 400 million international households may prove to be unrealistic when all is said and done.

Overall, I’m not arguing that NFLX doesn’t have great prospects, but rather, the current stock price basically assumes that it will march unopposed with little competition globally, that NFLX can raise prices significantly and consumers won’t bat an eyelash, and that NFLX’s content costs will decline over time. I don’t view any of this as particularly realistic. Netflix is a great company, but the content creators still have the most power in this industry.

Conclusions

To be a great investor, you must always focus on risk and reward. You don’t need to predict the future. You merely need to take what is known from data, examine risk and reward, invest accordingly, and stand by your decision regardless of how irrational the market becomes.

Netflix’s stock price is irrational. There’s no scenario where a NFLX stockholder could hold the company over the long-term and receive an adequate return given the risk. You’re better off buying US treasuries or investment grade US corporate bonds than NFLX stock.

I don’t short-sell these days, but if I did, I’d find a way to bet against NFLX, and I’d probably utilize long-dated put options to do it. Buy small amounts of deep out of the money long-dated put options and buy more if the stock continues to rise. At some point, the reckoning for NFLX’s stock is going to come and those put options will have a shot at astronomical returns, so long as the strategy is implemented well.

For the vast majority of investors who are long-only, however, I’d simply say “don’t buy Netflix.” If you own it right now, sell it, and be ecstatic you just got paid 12 times revenues for a company that is losing $2 billion in cash annually.

Comments

Log in or sign up to join the conversation.