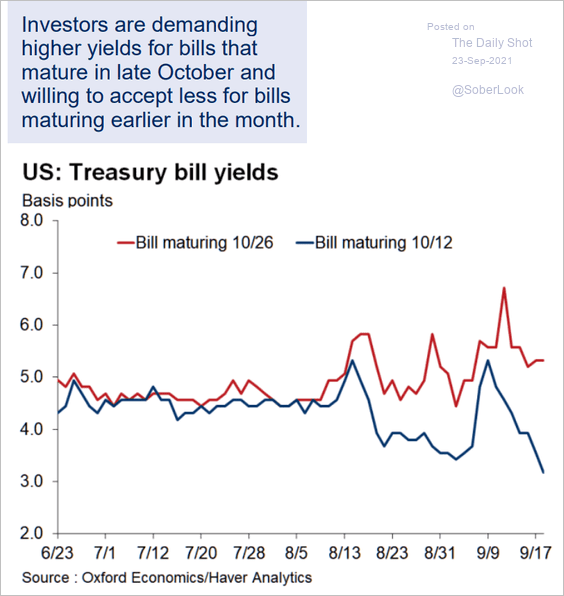

Greetings,

Let's start with the US employment report which beat consensus on Friday: 242K new jobs were created vs. 190K expected. This should, at least for now, alleviate any concerns about the US slipping into a recession. Here are some notable trends from Friday's Department of Labor report.

1. US labor force participation seems to be stabilizing. The second chart below shows US employment-to-population ratio.

There is clear evidence of more people entering the workforce and fewer dropping out.

2. The average duration of unemployment no longer seems to be declining and remains significantly above the pre-recession highs. Other data suggest that those who recently became unemployed quickly find a job but those who have been unemployed for a while are struggling.

3. US youth unemployment is at pre-recession levels although participation remains relatively low.

4. African American youth unemployment is the lowest in 16 years, although still unacceptably high.

5. US wage growth remains anchored around 2% per year. One explanation for the persistently tepid wage growth is the new entrants into labor force (#1 above). Whatever the case, there is still no significant evidence of wage pressures on a national level.

The Atlanta Fed GDP tracker rose in response to the jobs report (the index is quite sensitive to labor markets). It is now roughly in line with analysts' forecasts of just over 2%.

Treasuries got hit twice last week: once with the better-than-expected ISM manufacturing report and then again after the payrolls report. Chart shows the 5-yr note futures.

Fed Funds futures declined as well, with the market now expecting the next rate hike in November.

In other US economic developments, US exports have been the weakest since 2011. The chart shows exports vs. the US dollar index (DXY). Note that the dollar is the reason behind falling US exports. Politicians can debate trade all they want, but its the dollar strength that often determines American firms' ability to compete.

According to the Atlanta Fed, so far there doesn't seem to be a credit crunch for US small business. It could of course be a matter of falling demand.

We now shift to a few developments in emerging markets.

1. Russian CPI declines more than expected as the effects of the ruble collapse wane and domestic demand weakens.

2. Brazil's industrial production continues to contract. Auto production and new car registrations are hitting new cycle lows. This is just devastating ...

Of course that's not what everyone is focused on in Brazil. Instead, the nation's markets are betting that Dilma Rousseff will not serve the full term (triggered by former President Luiz Inacio Lula da Silva being detained). As a result, Brazil's stock market, currency are up sharply. This seems overdone as Dilma Rousseff's impeachment is anything but certain.

This has been the biggest weekly stock market jump in at least 20 years (30%).

3. Here are the historical and projected growth rates for select Asian economies.

Now let's take a look at some developments in China.

1. Here is one reason Moody's is starting to have some (slight) concerns about China's credit. The nation's government deficit is expected to widen further as Beijing expands fiscal stimulus and at some point could be forced to recapitalize some banks.

Source: Credit Suisse

2. China also has to deal with the ongoing growth in the so-called wealth management products (WMP). WMPs have been pushing corporate yields lower, as demand for higher yielding "deposits" expands the nation's shadow banking. One reason the PBoC has been reluctant to lower the benchmark rate (targeting the bank reserve ratio instead) is that lower rates will generate more leverage in the system by exacerbating "reach for yield". More on the topic here.

3. Iron ore futures on the DaLian Commodity Exchange continue to rally. Steel coil futures in Shanghai are also waking up. This is baffling some economists (given the glut in these commodities) but the markets are clearly pricing in higher demand. Is China's fiscal stimulus kicking in?

Related to the above, here are copper futures on Comex in what seems to be a short squeeze (the second chart shows the net exposure of speculative accounts). Industrial metals' multi-year slide seems to have been halted.

By the way, China is now clearly the global copper hub, as inventories in Shanghai exceed those in London.

Even the broad commodity indices (such as the Continuous Commodity Index) are starting to turn higher.

Here is what the commodities screen looked like on Friday.

As a result, the S&P mining shares are up 32% on the year. Amazing ...

Staying with the equity markets, shares of pharmaceuticals continue to underperform. What does this tell us about markets' expectations of who will be in the White House next year?

According to Morgan Stanley, corporate margin expansion has been concentrated at the largest firms.

Crude oil markets remain resilient (WTI crude holding firmly above $36/bbl) in spite of near-record inventory build in the US.

Also, US rig count is now below 400, the lowest level since 2009.

In the currency markets speculative accounts continue to increase net long yen positions. Given this, it's worth asking the question: is the yen's recent rally overdone?

Finally we have one item on asset management. According to Morgan Stanley, equity hedge funds are basically net long the S&P500 but running a negative alpha due to fees. This is a horrible trend for the industry which has lost its edge. Are institutional investors paying attention or just paying fees?

Turning to Food for Thought, we have 5 items this morning:

1. Here is what the betting markets are telling us about the US elections. Once again, if you disagree with these, you are free to place your own bets (debating these is arguing with the market).

2016 GOP nomination odds:

2016 general elections odds:

2. A philosophical divide between Americans and the Europeans.

3. According to Vox, America's lead poisoning problem isn't limited to Flint.

Source: @voxdotcom

4. Americans' views on free trade deals.

Source: @pewresearch

5. America's middle class is no longer the majority.

Comments

Log in or sign up to join the conversation.