Photo by Mitchell Luo on Unsplash

Leonardo da Vinci famously said that simplicity is the ultimate sophistication. A similar concept was proposed by Peter Lynch regarding investment research "Never invest in an idea that you can't illustrate with a crayon".

Alphabet (GOOG) (GOOGL), is a high-quality business with unique competitive advantages, the company is delivering vigorous revenue growth with exceptional profitability, and the stock is very attractively valued at current prices. In very simple terms, fundamental quality, financial performance, and valuation are three basic reasons to own Alphabet stock.

Fundamental Quality

Google is the leading player in search by a wide margin. The brand is so powerful that consumers use the expression "googling" information as opposed to online searching. Only the most valuable brands in the world can replace the name of the product or service with their own name.

Alphabet also benefits from scale advantages and the network effect. The more we use Alphabet's ecosystem of services, the more the company learns from its data, and it leverages on Artificial Intelligence to get exponentially better over time.

Privacy concerns are obviously a key issue in this regard, but it is fair to say that for most consumers the benefits of Google's offerings far outweigh those concerns. We always need to look at what consumers actually do over what they say, and the evidence shows that global consumers are deeply engaged with Alphabet and its wide ecosystem of services and applications.

The network effect provides an additional source of sustained competitive advantage for Alphabet. The more videos are uploaded to YouTube, the more viewers are attracted to the platform. More viewers also provide the incentive for content creators to keep producing more and better content. Creators and viewers attract each other to the leading platform that YouTube is, creating a self-sustaining virtuous cycle for the business.

It is not much of a stretch to say that Alphabet is one of the strongest companies in the world when it comes to competitive advantages, and these advantages can allow the company to continue creating value for investors over the long term.

Financial Performance

Alphabet's numbers for the fourth quarter of 2021 were nothing short of impressive. While rivals such as Meta (FB) are being hurt by changes in the Apple IDFA and competition from TikTok, Google keeps delivering outstanding performance at a large scale.

Total revenue during the fourth quarter of 2021 reached $75.3 billion, an increase of 32% year over year. Operating margin during the full year 2021 came in more than healthy, at 31% of revenue.

YouTube advertising revenue reached $8.63 billion, growing 25% versus the same quarter last year. The platform reached five trillion all-time views during the quarter, and it now has over fifteen billion views each day globally. In the past year, the number of YouTube channels that made at least $10,000 in revenue was up more than 40% year over year

Google is increasingly focusing on commerce for YouTube, making it easier for viewers to buy what they see on the platform and also for advertisers to drive action with new features such as product feeds in Video Action Campaigns and live commerce. The opportunities in this area are certainly compelling.

The cloud business is also firing on all cylinders. Cloud revenue grew 45% year-over-year to $5.5 billion last quarter. Alphabet’s backlog increased more than 70% to $51 billion, most of which is attributed to Google Cloud.

The balance sheet is pristine, Alphabet ended the year with $140 billion in cash and marketable securities versus only $14.8 billion in long-term debt, for a net cash position of $125.2 billion.

On the back of strong cash flow generation plus abundant balance sheet cash, Alphabet has more than enough resources to make all kinds of investments and acquisitions, and perhaps also to reward investors with increasing buybacks in the years ahead.

Attractive Valuation

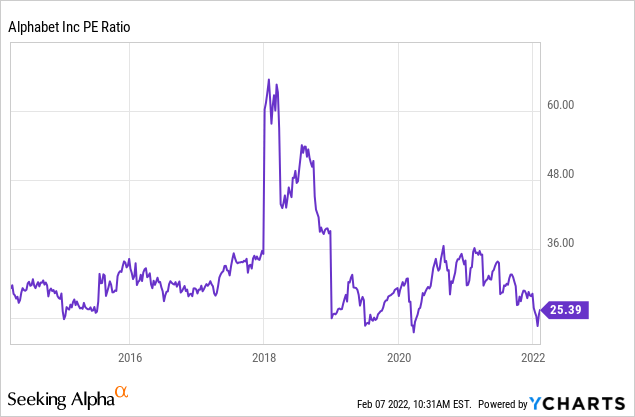

All this comes for an attractive valuation, the price to earnings ratio stands at a very reasonable 25.4. This is quite a cheap price on its own merits, and it is also the low end of the valuation range for Alphabet over the past decade.

Data by YCharts

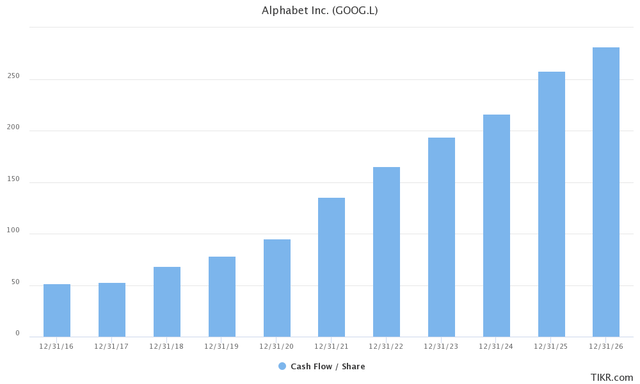

Wall Street analysts are on average expecting Alphabet to make almost $165 in cash flow per share this year. This puts the price to free cash flow ratio at around 17.3 times on a forward basis. The number would represent a 5.8% cash flow yield for investors in Alphabet at current prices.

Alphabet cash flow per share and forward estimates (TIKR Terminal)

Valuation is an art as much as a science, and we also need to incorporate the fact that growth rates will naturally slow down as Alphabet gains scale over the years to come.

Nevertheless, and considering the quality of the business as well as current financial performance, the numbers show that Alphabet stock is quite attractively valued, if not downright undervalued.

Risk And Reward Going Forward

Competition is always a relevant risk in such a dynamic industry. Emerging players such as TikTok have been gaining a lot of ground lately, and it is always important to monitor how the competitive landscape is evolving.

Alphabet has outstanding competitive advantages due to brand recognition, scale, and the power of the network effect. At this point, competition does not seem to be much of an issue for the company. However, it is always important to watch competitive dynamics when investing in tech and growth stocks.

Regulatory pressures are one of the themes that always cause concerns for investors in Alphabet due to the company's dominant position in several key markets and its access to user data. Google has paid some fines and it has been forced to modify some business practices considered anti-competitive in the past, but nothing too damaging to the company's fundamentals. Even if the impact of regulatory pressure has been moderate so far, this factor can be expected to hurt the stock price from time to time.

Over the long term, one key risk factor to watch is how trends such as blockchain technology and decentralization will affect a tech giant such as Google. It is far too early to reach any conclusions, however, it is not too early to be monitoring these trends.

Access to data is crucial for the business model, and new technologies that limit or even eliminate data sharing could be disruptive. Alternatives such as DuckDuckGo, which is a privacy-focused search engine, come to mind, and it makes sense to expect more offerings of this kind in the future.

These kinds of risks can be overstated by investors. A monopoly is typically a company that does not have any relevant competition and uses that power to raise prices excessively, hurting consumers in the process.

Alphabet, on the other hand, charges zero for most of its products, and it uses the data to leverage Artificial Intelligence and to deliver an improving user experience over time. Most consumers love Google and use the company's services regularly, and that is a key differentiation versus what we understand as monopolies in the old industrial era.

Besides, consumers can literally leave Google for a better alternative with a single click, so it is hard to say that those consumers are being held captive. Consumers simply decide to stay with Google, which is a major difference.

I'm not saying that these risks are irrelevant, on the contrary, these are important factors that need to be monitored. Nevertheless, there is a chance that the market could be overstating these factors. Especially at current valuation levels, it seems to me like these risks are already well incorporated into expectations and hence in the stock price.

Risk can never be avoided in the stock market, the key is assuming the right risks, meaning the ones that are well compensated with superior upside potential. When considering business quality, execution, and stock valuation, the risk to reward trade-off in Alphabet looks clearly attractive.

Comments

Log in or sign up to join the conversation.