Stanphyl Capital’s letter to investors for the month of March, 2020 discussing that Tesla Inc. (Nasdaq:TSLA) isn’t a hypergrowth company.

Stanphy Capital On Tesla Bet

We remain short Tesla Inc. (TSLA), which I still consider to be the biggest single stock bubble in this whole bubble market. The core points of our Tesla short thesis are:

- Tesla has no “moat” of any kind; i.e., nothing meaningfully proprietary in terms of electric car technology, while existing automakers—unlike Tesla—have a decades-long “experience moat” of knowing how to mass-produce, distribute and service high-quality cars consistently and profitably, as well as the ability to subsidize losses on electric cars with profits from their conventional cars.

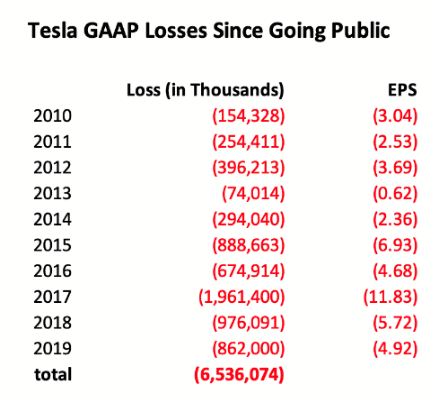

- In 2020 Tesla will again lose money, as it has every year in its 17-year existence.

- Tesla is now a “busted growth story”; revenue growth is flatlining while unit demand for its cars is only being maintained via price cutting.

- Elon Musk is untrustworthy

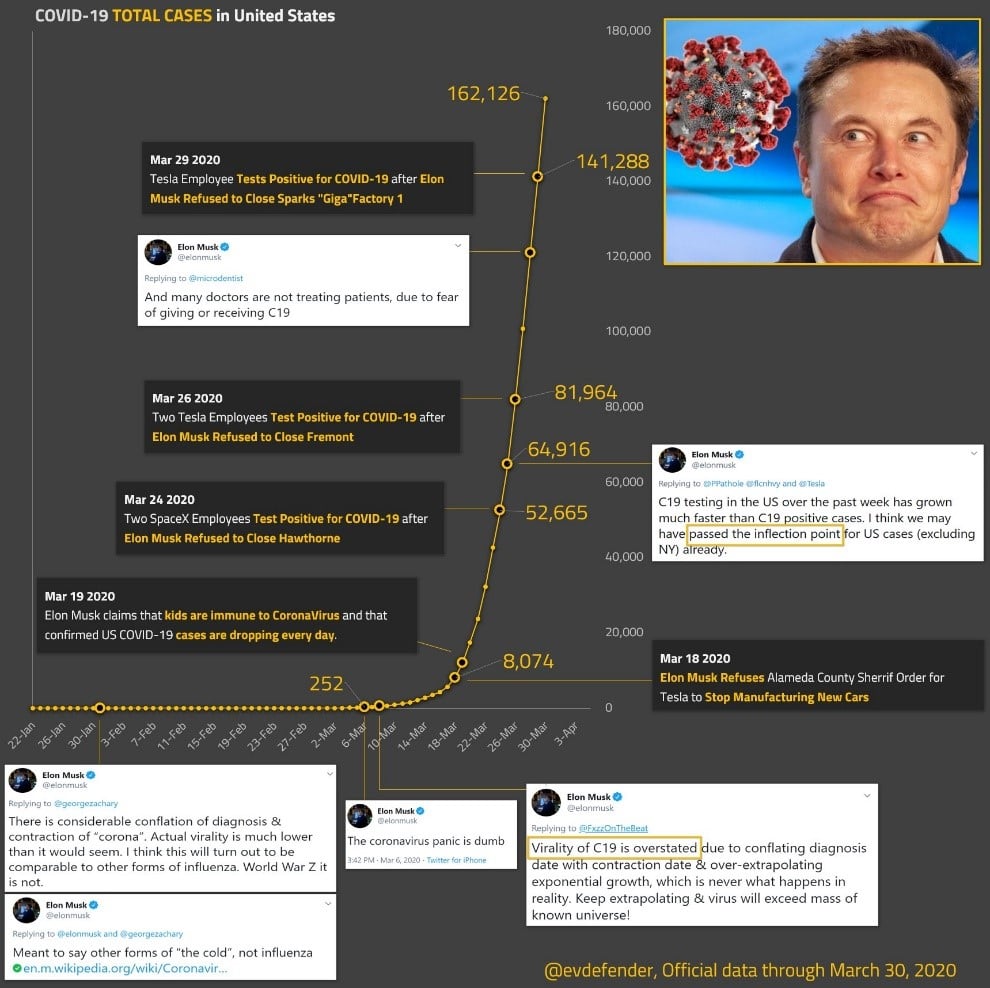

After keeping his California factory open a week beyond an Alameda County-imposed coronavirus shutdown date (and then partially open even later), thereby exposing thousands of Tesla employees to this potentially deadly disease with the full cooperation of California’s filthy state and local politicians, Elon Musk officially earned the title of “America’s Most Sociopathic CEO.” His public statements and actions regarding COVID-19 have been absolutely vile; he’s truly one of the world’s most despicable human beings. Here’s an abbreviated timeline of his comments, courtesy of Twitter user @evdefender…

(Click on image to enlarge)

Tesla Isn’t A Hypergrowth Company

With much of the world now shut down and auto sales at depression-era levels, on the back of my envelope I’d guess Tesla is currently burning around $100 million a week, and considering that its cash balance is likely far below the prettified number presented at the end of Q4 (even with a subsequent $2 billion capital raise), the company will clearly need to raise yet more capital in Q2 or Q3, perhaps into a fiercely unforgiving market.

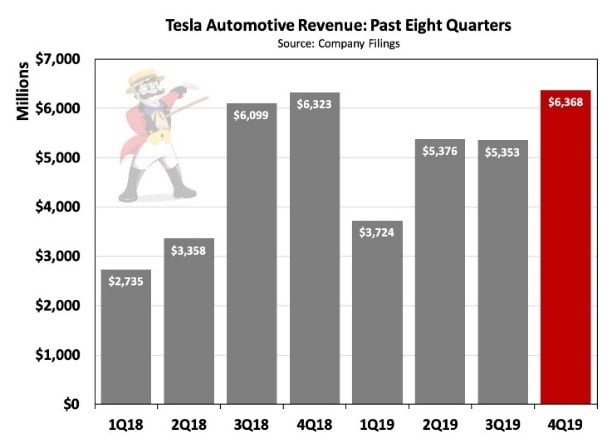

In January Tesla reported $105 million in earnings for the fourth quarter of 2019 (entirely from the sale of regulatory emissions credits, not from a self-sustaining auto business), which was down 25% from Q4 2018, while revenue was up just 2% and the full-year loss was $862 million. If we compare the second half of 2019 to the second half of 2018, Tesla revenue fell 3% and net income fell 45%, and in Q4 U.S. revenue fell 34%. Yet somewhere out there is a mass of idiots still grotesquely overpaying for this stock because they think it’s a “hypergrowth” company. Liam Denning at Bloomberg did an excellent job of pondering that absurdity.

Additionally, Tesla’s “earnings” are typically inflated by at least $200 million per quarter due its massive ongoing warranty fraud, so in reality the company likely lost money in Q4; here’s an excellent Seeking Alpha article and another one in Fortune explaining some of this.

Yet even with all that fraud, here (courtesy of my friend, Twitter user @Montana_Skeptic) is a great historical chart of Tesla’s earnings track record despite billions of dollars in public subsidies:

And courtesy of Twitter user @TeslaCharts, here’s a chart of Tesla’s revenue “hypergrowth”:

What “Autopilot Will Be Feature Complete” Means

As for the nonsensical Q4 earnings conference call, this quote from Musk about when so-called “Autopilot” will be “feature complete” may have been the highlight:

“feature complete just means like it has some chance of going from your home to work let’s say with no interventions. So, that’s — it doesn’t mean the features are working well, but it means it has above zero chance. So I think that’s looking like maybe it’s going to be a couple of months from now.”

That insane statement prefaces Musk’s desire to recognize approximately $500 million of non-cash (it’s already on the balance sheet) deferred revenue from its fraudulently named “Full Self-Driving” (the capabilities of which offer nothing of the kind), thereby turning a future money-losing quarter (likely Q2 2020) into one showing paper profits. Meanwhile, God only knows how many more people this monstrosity unleashed on public roads will kill, despite February’s NTSB hearing condemning it as dangerous.

For those of you looking for a resumption of growth from Tesla’s upcoming Model Y, demand for that car is reportedly disastrous. This is unsurprising, as it will both massively cannibalize sales of the Model 3 sedan and (later this year and in 2021) face superior competition from the much nicer electric Audi Q4 e-tron, BMW iX3 (in Europe & China), Mercedes EQB, Volvo XC40 and Volkswagen ID.4, while less expensive and available now are the excellent new all-electric Hyundai Kona and Kia Niro, extremely well reviewed small crossovers with an EPA range of 258 miles for the Hyundai and 238 miles for the Kia, at prices of under $30,000 inclusive of the $7500 U.S. tax credit. Meanwhile, the Model 3 will have terrific direct “sedan competition” later this year from Volvo’s beautiful new Polestar 2, the BMW i4 and the premium version of Volkswagen’s ID.3.

And if you think China is the secret to the resumption of Tesla’s growth, let’s put that market in perspective even without the coronavirus problems: prior to a recent 10% VAT exemption Tesla was selling around 30,000 Model 3s a year there, and “the story” is that avoiding the 15% tariff and 10% VAT, plus a $3600 EV incentive will allow it to sell a lot more. However, the rule of thumb for the elasticity of auto pricing is that every 1% price cut results in a sales increase of up to 2.4%. If we assume a 2.4x “elasticity multiplier,” domestically produced Model 3s that are 33% cheaper would result in annual sales of just 54,000 (33% x 2.4 = 79% more than the previous 30,000), meaning Tesla’s new Chinese factory would be a massive money-loser by running at just slightly more than 1/3 of its initial 150,000-unit annual capacity and 1/10th of the capacity it will have two years from now. This guarantees hugely missed growth targets and it is “growth” (or more accurately, the fantasy of growth) that drives Tesla’s stock price. And here’s a great overview of what a dogfight the Chinese EV market has become.

Tesla’s Car Sales

Meanwhile, sales of Tesla’s highest-margin cars (the Models S&X) will be down by roughly 50% worldwide this year vs. their 2018 peak, thanks to cannibalization from the less expensive Model 3 and direct high-end competition (especially in Europe and China) from the Audi e-tron, Jaguar I-Pace, Mercedes EQC and Porsche Taycan, with multiple additional electric Audis, Mercedes and Porsches to follow, many at starting prices considerably below those of the high-end Teslas. (See the links below for more details.)

And oh, the joke of a “pickup truck” Tesla introduced in November won’t be any kind of “growth engine” either, especially as if it’s ever built it will enter a dogfight of a market.

Meanwhile, Tesla has the most executive departures I’ve ever seen from any company; here’s the astounding full list of escapees. These people aren’t leaving because things are going great (or even passably) at Tesla; rather, they’re likely leaving because Musk is either an outright crook or the world’s biggest jerk to work for (or both). And in January Aaron Greenspan of @PlainSite published a terrific treatise on the long history of Tesla fraud; please read it!

In May Consumer Reports completely eviscerated the safety of Tesla’s so-called “Autopilot” system; in fact, Teslas have far more pro rata (i.e., relative to the number sold) deadly incidents than other comparable new luxury cars; here’s a link to those that have been made public. Meanwhile Consumer Report’s annual auto reliability survey ranks Tesla 23rd out of 30 brands (and that’s with many stockholder/owners undoubtedly underreporting their problems—the real number is almost certainly much worse), and the number of lawsuits of all types against the company continues to escalate– there are now over 800 including one proving blatant fraud by Musk in the SolarCity buyout (if you want to be really entertained, read his deposition!).

So in summary, Tesla is about to face a huge onslaught of competition with a market cap larger than Ford, GM and Fiat Chrysler combined, despite selling a bit over 400,000 cars a year while Ford, GM and Fiat-Chrysler sell 5.4 million, 7.7 million and 4.4 million vehicles respectively, generating billions of dollars in annual profit. Thus, this cash-burning Elon Musk vanity project is worth vastly less than its roughly $110 billion enterprise value and—thanks to nearly $30 billion in debt, purchase and lease obligations—may eventually be worth “zero.”

Comments

Log in or sign up to join the conversation.