Valeant (VRX) stays in the news. First of all, it keeps getting sued. In addition to customer and shareholder lawsuits and investigations of fraud at Philidor, prosecutors are investigating whether former Valeant executives were complicit in Philidor's fraud. Former Sprout Pharmaceuticals investors recently sued the company for botching the marketing of Addyi, the female libido pill. Valeant acquired Sprout for $1 billion last year; the lawsuit claims Valeant failed to make promised investments in marketing the drug which shortchanged Sprout investors on royalty payments.

Just as more lawsuits came to light, news leaked that the company was in talks to sell its Salix operations to Takeda (TKPYY), (TKPHF) for $10 billion. VRX soared 33% on the news. According to Barrons, Takeda is valuing Salix at 10x - 12x EBITDA:

WSJ is reporting that Salix could fetch $8.5-10B for Valeant … and supposedly there are 2 bidders involved.

From our perspective, the real question is: how does this $8.5-10B price compare to what market is assigning to this business today.

Again, I am not talking about the $16B+ that Valeant paid to acquire this biz … they clearly overpaid (relative to where the Salix biz is tracking currently).

Based on our math, a sale price of $8.5-10B is likely 10-12x EBITDA - which is reads better than what market is assigning to this business within Valeant currently. More importantly, if this sale materializes, it takes care of 2 issues: ((i)) whether Valeant can sell assets for >10x EBITDA; ((ii)) that Xifaxan TRx have stalled and patent litigation is a long-term overhang.

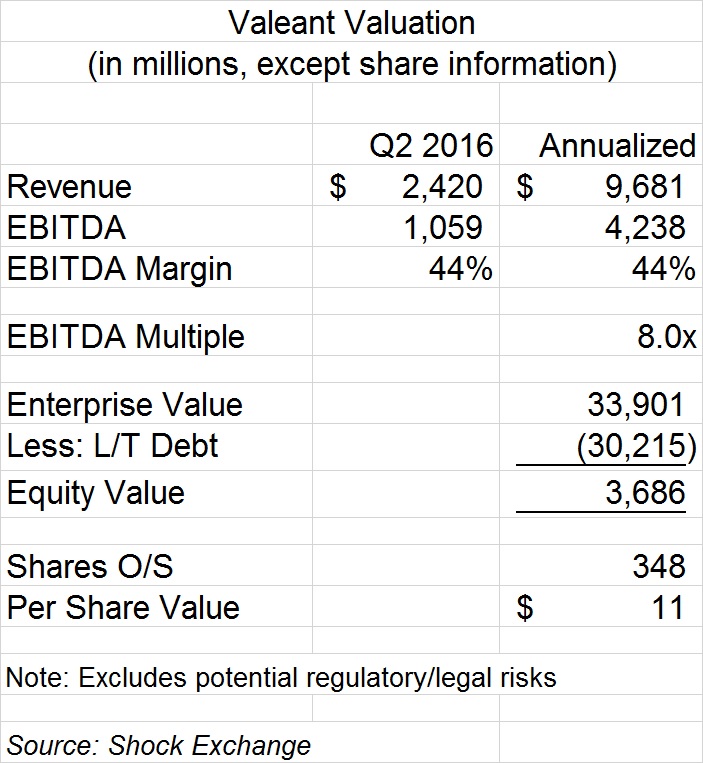

VRX bulls rejoiced over the news. However, Takeda's valuation of Salix is bad news. It actually justifies my $11 valuation of VRX.

Takeda Confirms VRX Is Worth $11

To entice sellers to the bargaining table buyers usual have to offer a takeover premium for properties. The typical takeover premium is 25% to 30% of a property's standalone value. Takeda's talks to acquire Salix at 10x - 12x EBITDA implies that Salix is worth less standalone. A built in takeover premium of 25% would imply a fair value of 8.0x - 9.6x as is. Ironically, I recently valued VRX at 8.0x EBITDA or $11 and VRX bulls were apoplectic.

The rationale for the 8.0x multiple is that Valeant should be awarded a multiple consistent with biotech companies. It is not a biotech company in the traditional sense. It has little R&D to speak of and developing new products is not its forte. As a serial acquirer of brands, Valeant acts more like a hedge fund. Since its ability to pass along price increases has been hampered, Valeant's ability to grow revenue and EBITDA will likely be constrained going forward. In my opinion, an 8.0x multiple is more than fair for a no-growth acquirer of brands like Valeant. Apparently, Takeda agrees.

Sans Salix, Valeant's Valuation Could Fall

The majority of Valeant's $34 billion enterprise value is tied up in the company's $30 billion debt load. While revenue and EBITDA might decline going forward, the debt stays constant; this could hurt VRX's valuation going forward. Secondly, of Valeant's portfolio companies, Salix is considered to be the crown jewel; its revenue and earnings are considered the most stable. If Salix is ever sold, the remaining parts could be less stable and less valuable.

In a recent Seeking Alpha article Starfish Investing suggested that after Valeant's sale of Salix at 10x EBITDA, the remaining parts should deserve an even higher multiple:

The 10X multiple is a significant discount from the 14X industry average, but I gave Valeant this low multiple because of its massive amount of debt. Valeant's debt will reduce by $10 billion, one-third of its current $30 billion if the Salix sale is successful ... As a result of the sale, Valeant would have a lowered EBITDA, but deserve a higher EBITDA multiple to match the rest of the industry. The result will be an overall increase in value for shareholders.

Again, I advise the opposite. Valeant is not a biotech company so it should not be rewarded the 14x multiple awarded biotech participants. After the Salix sale, the remaining parts could be even less attractive, so valuing the remaining parts at 8x would be kind.

The Salix sale is a key milestone for Valeant. The company needs to prove there is a market for its underlying assets and it can sell them for at least 10x EBITDA. In Q4 2015 it intimated it would sell contact lens maker, Paragon. However, no sale has occurred and the sale of Salix is still just market chatter. The fact that Valeant has not executed any asset sales in nearly a year is telling. Either the market for such assets is limited or 10x EBITDA is a pipe dream.

Conclusion

VRX soared on news that Salix could be sold for 10x - 12x EBITDA. It's actually bad news. It portends that VRX -- sans a takeover premium -- is worth 8x EBITDA or $11/share. VRX remains a sell.

Comments

Log in or sign up to join the conversation.