NOTE: The following views, opinions, comparisons, and reported facts are entirely those of Epstein Research [ER], not that of Troilus Mining’s management team, board or advisors. Please see disclaimers/disclosures at bottom of article.

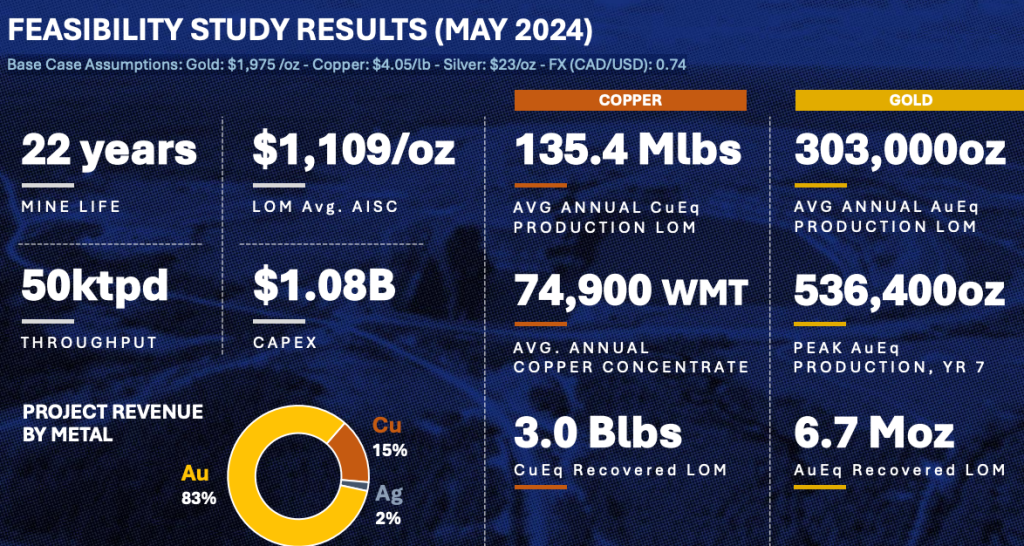

Troilus Mining (TSX: TLG) / (OTC: CHXMF) has a world class, growing, 13.0M oz gold (“Au”) / copper (“Cu”) project in Quebec with a May-2024 Feasibility Study on it. Funding news, a new resource estimate, and final permitting could be important investment catalysts.

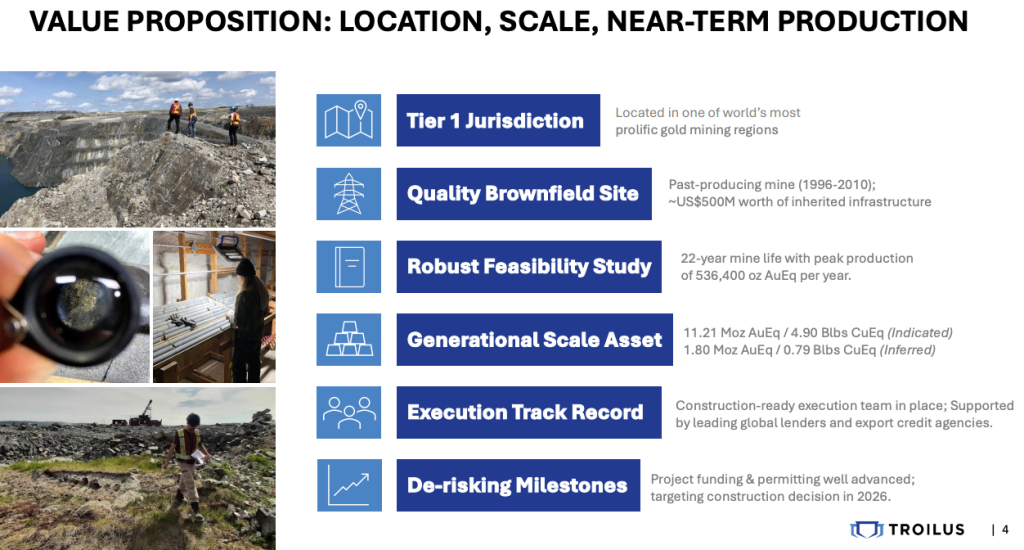

The flagship Troilus project is on a past-producing site with reportedly over US$500M of legacy infrastructure in place. Low-cost, clean, hydroelectric power has been secured. In addition to ample Au production, Troilus will be a meaningful source of future Cu supply for Canada. For more details on the project, see images, tables, maps, below.

I’m asked why it’s taking so long for Troilus to nail down the final details of a fully-funded project package (incl. coverage of possible cost overruns & working capital needs).

I don’t agree that it’s taking too long simply because the Company, led by CEO Justin Reid, is engaged in a methodical, prudent approach. This expanding, highly-talented team is weighing all options with the help of third-party financial professionals as needed.

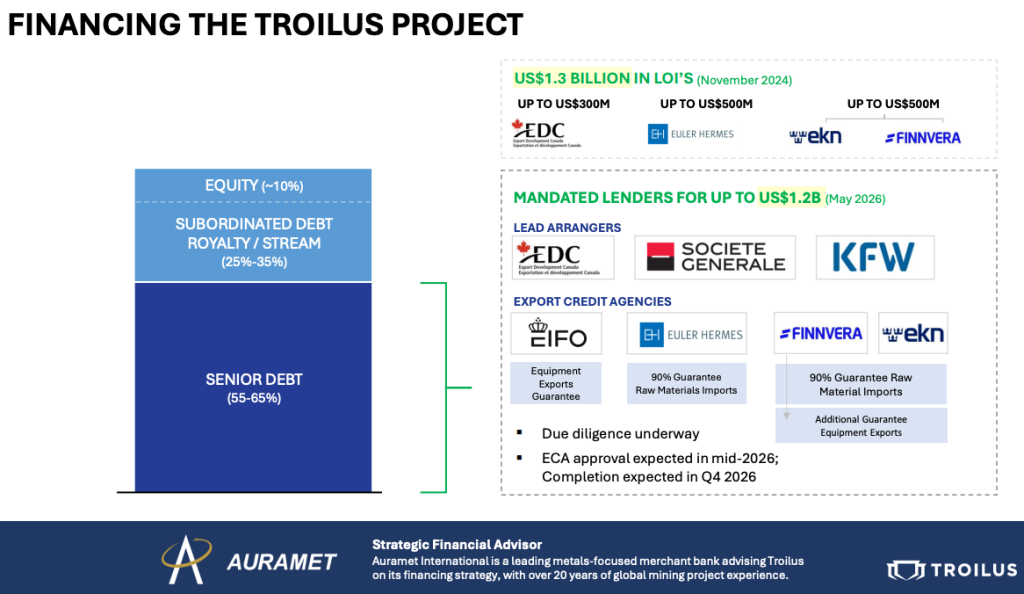

Options on the table are debt, streaming and equity, with the possibility of partially pre-paid forward sales via off-take agreements, and the potential for government grants (neither pre-paid off-takes nor grants are a sure thing).

In my view, Troilus likely needs to raise ~US$1.5B (including a cash cushion). For those who think that’s a lot, it really is not that bad. Consider that management announced that up to US$1.2B could come from debt funding.

Yes, more equity is required, but it need not be issued all at once. Having said that, if strong investment groups (institutions, prominent investors, pension funds, natural resource groups, PE, etc.) want in, (on good terms for the Company), I imagine management would consider it. Lately, the Company has raised equity without warrants — a trend it hopes to continue.

Bottom line, Troilus is evaluating a range of financing alternatives, including debt, equity, streaming and off-take-linked structures, with the objective of securing an efficient and executable financing package, with targeted decisions expected this quarter.

Turning back to the debt component, management upsized its debt capacity estimate to US$1.2B due mostly to global inflationary pressures across all industrial sectors & jurisdictions. Presumably higher oil/gas/diesel prices for example.

As an aside, the weaker C$ vs. the US$ (from C$1.35 in the May 2024 Feasibility Study to C$1.415), is a modest tailwind.

In May 2024, Au/Cu prices were well below current levels, AND the Company’s market cap was far smaller. Investors understandably worried about debt funding. And, if enough debt capacity, at what price? I distinctly remember commentary from investors fearing 12%-15% debt with a large slug of equity warrants, when the share price was under C$0.35 vs. today’s C$1.67. Now, I believe sub-10% debt is likely.

In prior articles, I mentioned Skeena Gold & Silver refinancing its debt before producing a commercial ounce. Skeena’s bonds were priced at par ($100) with an 8.5% coupon. They now trade at $105, yielding 7.0%. Skeena’s valued at ~C$5 billion.

If Troilus were to follow Skeena’s timeline, it could possibly be in a position to issue corporate bonds (if it wanted to) in 18-24 months. I’m not suggesting this is the plan, but it speaks to the range of financing alternatives.

Finally, on streaming, I get asked if management is looking at streaming Au, silver or Cu. The answer is all of the above, or none. CEO Reid has financial experts continually assessing all streaming options.

Troilus would rather stream Au and/or silver if it can get a better deal than streaming Cu. It’s just math. If the proposed cost of capital for streaming comes in at an attractive level, management would likely monetize a small portion of metal(s) this way.

Investment pundits believe competition for metal streams from safe jurisdictions is high. It’s been widely reported for the past year that smelters are very interested in securing Cu concentrate. Notice that the Cu price has held up far better than Au, down just -5% from its ATH vs. Au -27%.

Spreading total cap-ex needs (+ cost overruns & working capital) across debt, streaming & equity (with possible off-takes and/or grants) is a wise move to maximize financial flexibility and lower risk.

Management has several initiatives underway to move the project forward in tandem with ongoing funding steps. Things like robust mine optimization studies, ordering long-lead time equipment, hiring new executives.

It has completed basic engineering, and mobilized detailed engineering/procurement teams with BBA (incl. 3D modeling, vendor selection, and infrastructure planning).

Management is advancing geotechnical work, site characterization, and early earthworks such as road relocations, deforestation, mobile crushers for aggregate, and pit de-watering. The company is expanding on-site infrastructure (increasing camp from 100 to 250 people, plus a septic system/kitchen for a 1,000-person peak workforce).

Now a word on drilling. Readers are typically not overly excited by infill drilling, but checks with industry players and comments from large shareholders suggest that drilling has been successful. And, management is doing more than just infill work, in my view there could be new discoveries down the road (but no guarantees).

Wide widths at under 1.0 g/t Au Eq. might not be SEXY, but the 13.0M oz existing resource is at 0.69 g/t Au Eq. So, the 150+ meters in two recent holes @ 0.95 g/t Au Eq. should (subject to more drilling) lead to a meaningful increase in the number of ounces.

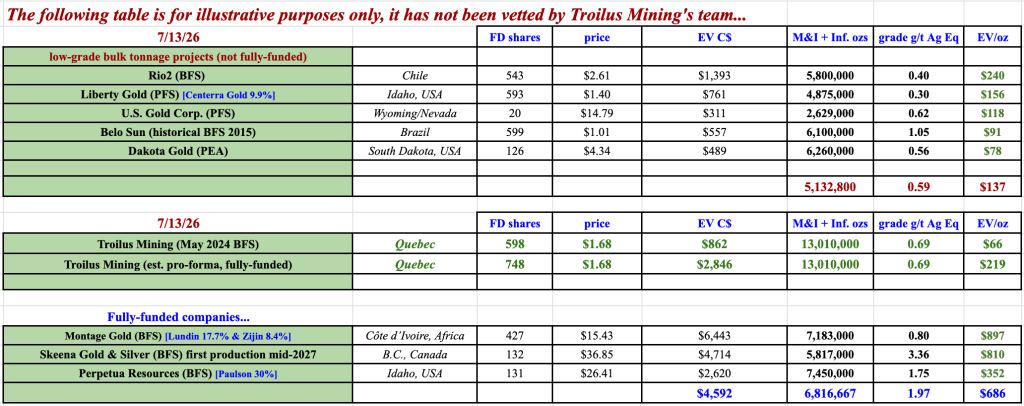

How much might a fully-funded, fully-permitted Troilus Mining be worth? In my view, a lot more than today’s roughly C$860M. Compare Troilus to new producer Artemis Gold. Artemis is expected to produce ~280,000 very low-cost ounces this year. It’s valued at nearly C$8 billion.

If a producer is looking to acquire Troilus, it could presumably increase production above 300,000 oz/yr. As it stands, maximum production in year 7 is 536K Au Eq.

Importantly, I believe a C$10B+ producer (of which there are a few dozen, not incl. Chinese/Russian names) were to acquire Troilus, it could self-fund cap-ex (deployed over 2-3 years), allowing for a strong takeout price to be paid.

G2 Goldfields & Rupert Resources were recently acquired for over C$550/oz. I do not include them in the following table as they’re not low-grade, bulk tonnage plays. Note, they were earlier-stage then Troilus Mining (PEA/PFS, respectively) and were not fully-funded.

At the bottom of the table are three fully-funded juniors with an average EV/Au Eq. oz ratio of C$686/oz. By contrast, I estimate a pro forma, fully-funded Troilus might be valued at ~C$219/oz.

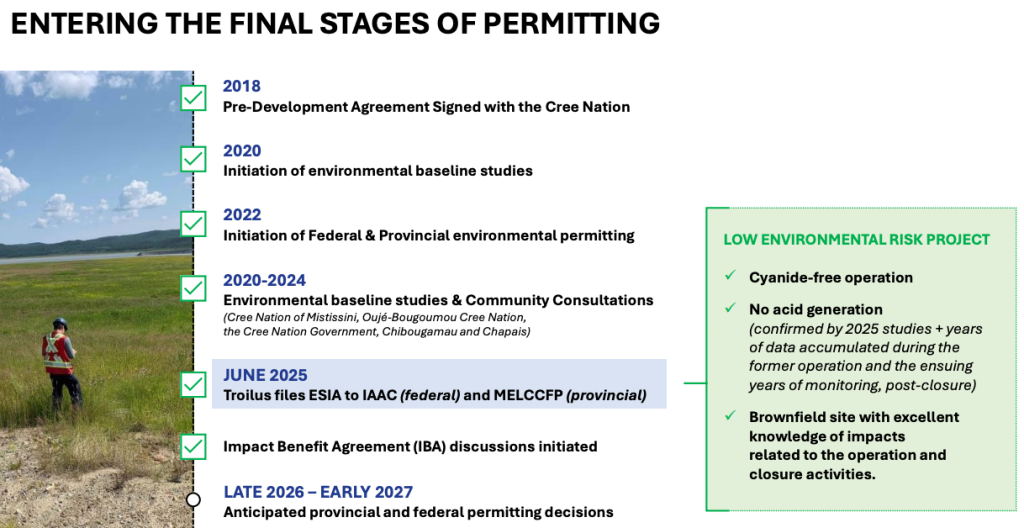

Although I remain bullish on Troilus Mining, there are plenty of risk factors to consider; permitting delays, lower metal prices, social license to operate, funding, construction delays, etc.

I believe the Company has made good progress since its May 2024 Feasibility Study, and that many risk factors appear to be under control. However, things can change. Metals/mining juniors, even in safe jurisdictions, are high-risk investment propositions.

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Troilus Mining, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of Troilus Mining are highly speculative and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. Readers assume and agree that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Troilus Mining was an advertiser on [ER], and Peter Epstein owned shares in the Company bought in the open market.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors, including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector, or investment topic.

Comments

Log in or sign up to join the conversation.