Source: Dmitry Schemelev

Despite the lower-than-expected earnings report in April 2017, Starbucks (SBUX) is still the largest coffee shop chain in the world, with more than 23,000 outlets. Global expansion in the Asian market, fueled in part by China's ballooning economy, has boosted its revenue stream. China has become the company's second largest and second fastest growing market. Digital innovations, such as the membership and rewards mobile apps, as well as the recent U.S. tax cut have benefited the company.

In 2018, Starbucks will concentrate on its core business: the coffee shop. According to its forward-looking statement, it will close Teavana stores and streamline other activities. To increase its profit margin, as well as improve the customer experience through in-store, third-place experience and digital innovations, Starbucks plans to gain 100% control of all stores in the East China region that have been jointly owned by Starbucks, UPEC, and PSCS.

Recently, Starbucks' financials have had some flopping numbers, most likely because of streamlining other branches and the partnership buyout in the East China region, which have exhausted its budget. However, in comparison to the industry and its rival, McDonald's (MCD), Starbucks takes better care of its shareholders. This is reflected in dividend yields that have more than doubled in the past four years, even when the return-on-assets have slipped.

Considering Starbucks' financial strengths in some areas and weaknesses in others, there is a good chance that Starbucks is undervalued.

The Intrinsic Value

Warren Buffett, a disciple of Ben Graham's value-investing theory, has shown the world that long-term sustainable profits come from picking undervalued stocks and holding them. There are many ways to determine a company's intrinsic value; most of them involve fundamental analysis. One popular method is discounted cash flow (DCF).

There are three major types of DCF you can use to evaluate a stock: EBITDA exit, growth exit, and revenue exit. Because Starbucks is a mature and profitable company, a suitable DCF method should measure the terminal earnings growth for the next five years.

Starbucks' annual growth rate for the past five years has been 17.14%. This number is a bit aggressive to use as a projection for the growth rate for the next five years. A more conservative - and perhaps more realistic rate - can be obtained by reducing this number by 10%, or a growth rate of 15.426%.

It is advisable to use an industry group's P/E to determine the current year's EPS, as well as to project an industry group's future P/E. The 2018 P/E for Starbucks' industry group is an aggressive 25.23%. To obtain a more realistic future rate, a further reduction is necessary. Reducing the 25.23% P/E by 15% results in a projected P/E of 21.4455%.

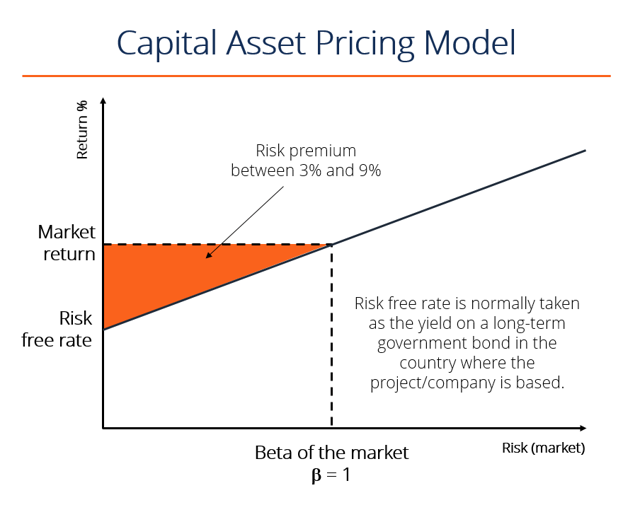

Evaluating return on investment (ROE) is crucial because it involves estimating an expected annualized rate of return. Some investors use their gut feelings, some use analysts' estimations, and others use mathematical models. For this example, the mathematical model of capital asset pricing model (CAPM) is used.

Source: CFI

The formula behind this model is simple and straightforward. It uses a linear function. The actual equation is:

Where:

Ra = expected return

Rrf = risk-free rate

Ba = beta of the stock

Rm = market risk premium

For the market risk premium, $VIX.X (or the CBOE Volatility Index) will be used. For the risk-free asset, either $TNX or $TYX can be used. These indicate that the Treasury bill rate will mature in 10 years or 30 years, respectively. For this example, $TYX will be used.

At the time of writing, we used the following numbers (taken from TD Ameritrade):

- Price of SBUX: 57.37

- Beta of SBUX: 0.6

- $VIX.X: 14.75

- $TYX: 3.124

- EPS (TTM): 3.15

Keep in mind; the $VIX.X value directly cannot be used directly for CAPM. As a rule of thumb, the market risk premium (MRP) can be found from ranges listed below:

- If VIX.X is < 13, MRP will be 5

- If VIX.X is 13-18, MRP will be 6

- If VIX.X is 18-30, MRP will be 7

- If VIX.X is 30-45, MRP will be 8

- If VIX.X is >45, MRP will be 9

The VIX.X falls in the range of 13-18, so that indicates our MRP is 6. Put all the numbers into the CAPM equation we would have an expected annualized return of 6.724%.

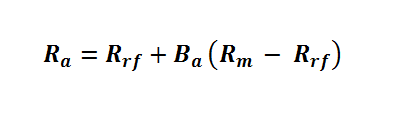

To construct the DCF model, use the cash flow (the trailing EPS, or 3.15) to project the future cash flow and model it with the projected growth rate of 15.426%. To estimate a terminal value after five years, multiply the result of the projected growth rate 5 times. Use an appropriate exit multiple (in this example, the industry average projected P/E ratio), which results in 21.4455%. The equation is set up as:

Insert the calculated values into the equation to obtain:

Finally, we need to discount this number by the rate of return calculated from our CAPM model, or 6.724%:

At the time of this writing, the calculations yield an intrinsic value of 99.97, which, compared with the current price, gives a margin of safety of 42.611%. In general, a margin of safety that is larger than 25% would make the stock a good candidate for value investing.

Investors should not rely solely on numbers derived from the CAPM model. Because it assumes a rational market, which is not true in the real world, the CAPM model is being criticized as being too "idealistic." There are other fundamental characteristics that should be examined to further confirm any conclusions. Also, it would be pertinent to identify Starbucks' competitors, so a broader scope of an industry can be obtained.

Further Examinations

In his magnum opus, The Intelligent Investor, Ben Graham laid out several instructions for different types of value investors on what to look when picking stocks. When looking for a long-term investment, these are his criteria for defensive investors.

According to Ben Graham, a good undervalued company should have:

- Not less than $100 million of annual sales (or $500 million in today's term adjusted for inflation).

- Current assets should be at least twice current liabilities.

- Long-term debt should not exceed the net current assets.

- Some earnings for the common stock in each of the past 10 years.

- Uninterrupted dividend payments for at least the past 20 years.

- A minimum increase of at least one-third in per-share earnings in the past 10 years.

- Current price should not be more than 15 times average earnings.

- Current price should not be more than 1.5 times the book value.

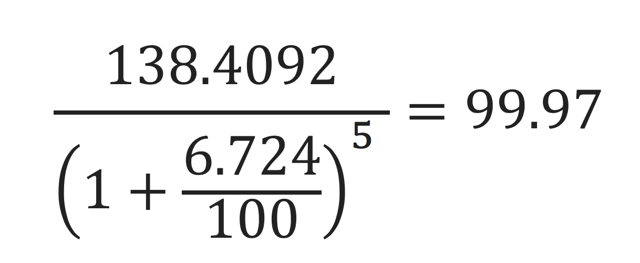

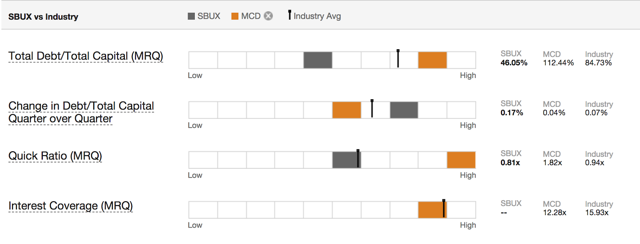

We can then evaluate Starbucks based on these terms. Starbucks has a revenue to common of $4741.8 million. The quick ratio shows that Starbucks' current asset is even less than its liabilities. However, given an industry average of 0.5 (see image below), Starbucks is not in a devastated state that would disqualify it from being a good company. By contrast, McDonald's outperforms Starbucks in this aspect, which is somewhat of a threat to Starbucks. Nevertheless, Starbucks has more capital to absorb debts than McDonald's (see "Total Debt/Total Capital" from the image below).

Source: GAAP SEC filing

The long-term debt makes up 65% of the total assets, which qualifies for the "long-term debt should not exceed the net current assets" criterion.

Source: GAAP SEC filing

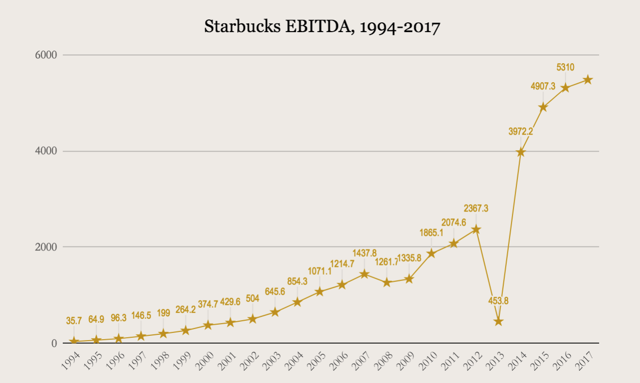

Throughout its history, Starbucks has shown an increase in the growth of its EBITDA despite the financial slump in 2013.

Source: ADVFN

Although Starbucks yields lower dividends than McDonald's, its dividend growth rate outperforms its competitor. At this rate, it is only a matter of time before Starbucks catches up to and outpaces McDonald's in annual dividend yield.

Source: GAAP SEC filing

Starbucks achieved an EPS of 1.99 in 2017. Compared with 0.9 in 2007, the company's earnings per share has more than doubled.

Source: GAAP SEC filing

Starbucks has a trailing P/E of 19.77, which is above Graham's suggested rate. However, his criteria were posited in the last century and are therefore somewhat outdated because the overall trend of average P/E in many industries has risen.

Price/book is high, however. The rate of 14.54x is much higher than the recommended 1.5x, and it is even higher than the industry average. This might explain why Starbucks is struggling to overcome its "price ceiling."

Source: GAAP SEC filing

Strengths and Weaknesses

To get a more holistic view, Starbucks' position within its industry should be identified. The retail coffee and snack industry is sensitive to its business cycle. For example, the growth within this industry stalled and experienced negative revenue during the financial meltdown ten years ago as the aggregate demand for goods and services decreased, reducing each company's sales. This created a growth opportunity for Starbucks to "globalize" by 1) attracting customers before its rivals, and 2) diversifying the risk that their entire operation would be exposed to a single bad economy.

Starbucks' leading position in China has helped it climb to the top of its industry worldwide. While McDonald's expanded its business in China before Starbucks, it faced fierce competition from KFC and other local Chinese restaurants. There are fewer coffee shops to compete with Starbucks. Dunkin Donuts has started opening stores in China, but they are less well-known than Starbucks. It is perhaps already too late for Dunkin Donuts to compete in a market that Starbucks dominates by 55%.

Nonetheless, Starbucks has weaknesses. It is a prevalent belief that products from Starbucks are exorbitantly priced. Competitors could exploit this vulnerability, especially when the economy slumps. At that point, consumers might shift to more affordable coffee shops rather than pay a premium for the "Starbucks Experience."

Aggressive expansion has caused problems. It is not surprising to read that one Starbucks shop has closed because another one has opened across the street. To fuel the expansion machine, Starbucks has had to self-cannibalize, closing some stores while openings others. Moreover, with the Starbucks' market in the United States saturated, more stores mean additional operating costs.

Over-reliance on coffee products gives Starbucks less control over pricing. There has been volatility in the global high-quality coffee bean market, which Starbucks cannot control unless it initiates vertical integration. This is unlikely to happen because of monopoly laws and the associated high costs. Another problem is the growing awareness of coffee's cancerous side effects that has been featured in recent news releases. California is considering passing a law that requires coffee shops to display labels that warn consumers of the risk. In this case, consumers might shift their purchases to other substitutes like juice, water, etc.

However, weaknesses create opportunities to mitigate or even eradicate those weaknesses. To soften its reliance on coffee, Starbucks has already begun to diversify its menu to cater to the tastes of different age groups. The self-cannibalization could be obviated by devising more prudent location-picking plans. Meanwhile, technological innovation and new distribution channels could allow Starbucks to augment its profits in a saturated market.

Given its strengths and weaknesses, opportunities are available for Starbucks. The Seattle-based company plans to do "something" in 2018, which suggests that it is trying to eliminate several of its existing financial weaknesses and is seizing the opportunities inherent in globalization and technological innovation. The actions Starbucks is planning to take will undoubtedly increase its intrinsic value.

Final Words

The ominous-looking numbers from Starbucks' financial reports might have resulted from major mergers, new production lines, and higher operational costs. For instance, the mergers in the East China region are partly responsible for the low P/B value, although the potential earnings that could be harvested from the Chinese market are promising. Starbucks' advantageous global allocation of its retail stores helps to attract loyal customers before the arrival of its rivals. The DCF model suggests that Starbucks is indeed undervalued. Combine these analyses and Starbucks should be financially competent enough to make it on to your value investing candidate list.

Comments

Log in or sign up to join the conversation.