The S&P 500 (Index: SPX) ended the final trading week of October 2019 on a very high note, setting a new record high closing value of 3,066.91 on Friday, 1 November 2019.

The week carried quite a lot of positive news, including much better than expected U.S. jobs numbers, a third quarter-point rate cut from the Federal Reserve, and reports the U.S. and China are getting closer to sealing a 'Phase 1' trade deal. All of that was enough to keep the trajectory of the S&P 500 tracking along at the upper edge of the redzone forecast indicated on our alternate futures spaghetti forecast chart:

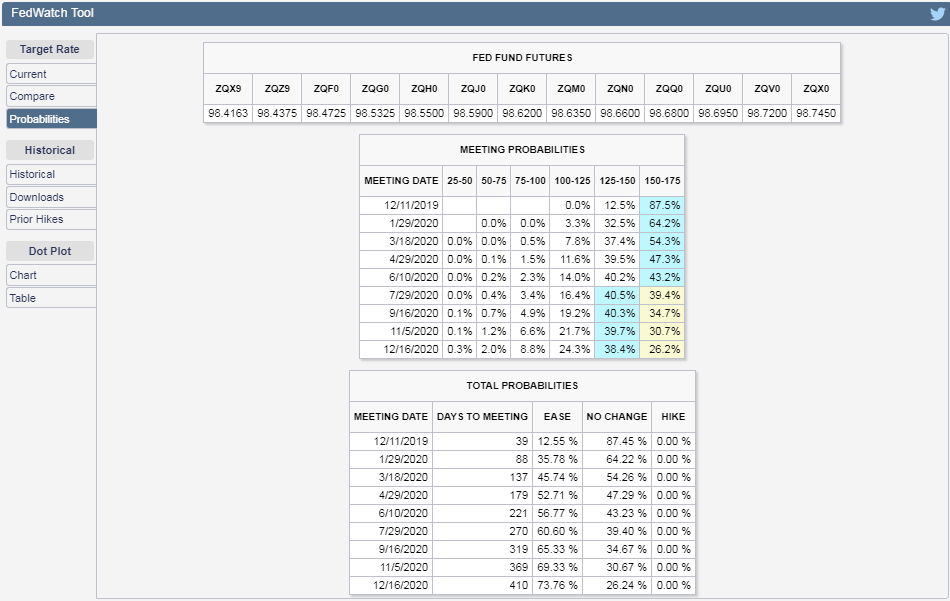

By far, the biggest news of the week was the Fed's third rate cut, which largely closed the door on the likelihood of any additional rate cuts in the remainder of 2019. The other positive economic data that came out during the week was such that investors appear to have pushed back their expected timing of the Fed's next change in the Federal Funds Rate, which the CME Group's FedWatch Tool now projects will most likely involve a quarter point rate cut in the third quarter of 2020:

Given the relatively close correspondence of our redzone forecast range with the projected trajectory associated with investors focusing upon this distant future quarter in our alternate futures chart, we've been paying close attention to the news stream over the last several weeks for any evidence investors might shift their attention to this particular point of time in the future. The probabilities indicated by the FedWatch tool above are the first confirmation that this quarter is now in the mix for shaping investor expectations of the future, with changes in the amount of dividends expected to be paid out in that distant future quarter taking place shortly afterward. Those changes have boosted the trajectory associated with investors focusing primarily on 2020-Q3 to nearly coincide with the trajectory associated with 2020-Q1 in the S&P 500 alternate futures chart during this past week.

But that's not all the new information investors encountered during the week that was. Here are the headlines we flagged for their potential market-moving potential during the past week.

Monday, 28 October 2019

- Oil falls on weak Chinese data, forecasts for U.S. crude stock build

- Bigger trouble developing in the Eurozone:

- Bigger stimulus developing in China in Brazil:

- Trump: 'ahead of schedule' on China trade deal

- S&P 500 hits record on trade optimism, Fed rate-cut expectations

Tuesday, 29 October 2019

- Oil mixed on forecast of falling U.S. fuel stockpiles

- U.S. Treasury's Mnuchin open to bank liquidity relief following overnight funding crunch: Bloomberg

- Bigger trouble developing in China:

- U.S.-China trade deal developments:

- Fed minions meeting on future for U.S. interest rates:

- Three-peat? Fed copies 1990s playbook in bid to avert a downturn

- Trump blasts Fed as policymakers meet on rates - In addition to rate cuts, President Trump is also arguing for the Fed to consider adopting negative rates in the future

- S&P warns of blow to Japan regional banks if negative rates deepen

- Wall St dips after S&P notes record, Fed on deck - referring to an intraday record!

Wednesday, 30 October 2019

- Oil extends losses as U.S. stockpiles jump

- U.S. Fed lowers interest rates, signals it is on hold

- Chile cancels APEC trade summit and major climate gathering after riots

- Bigger trouble developing in the Eurozone:

- S&P closes at record on Fed bump

Thursday, 31 October 2019

- Oil prices decline on weak Chinese data, U.S. pipeline problems

- Trade deal developments:

- Bigger trouble developing in China... and Canada:

- Trump says Fed hurting U.S. competitiveness, needs to cut rates more

- Wall Street retreats from record on trade cloudiness

Friday, 1 November 2019

- Oil rises nearly 4% on U.S.-China trade hopes, but sets weekly decline

- Positive jobs and trade news for U.S.:

- Bigger trouble developing all over:

- Bigger stimulus developing in China all over:

- Low, lower, lowest: Emerging central banks deliver more rate cuts

- Previous stimulus gaining traction? - China Oct. factory activity expands at fastest pace in over two years: Caixin PMI

- Fed minions speak after cutting rates for third time in last four months:

- Wall Street rallies to highs after upbeat U.S. jobs data

Elsewhere, Barry Ritholtz listed seven positives and seven negatives in the past week's economics and market-related news, in his weekly exercise aimed at maintaining an objective assessment of market-driving news events.

Comments

Log in or sign up to join the conversation.