Image Source: Unsplash

According to data from OilPrice.com, the price of West Texas Intermediate (WTI) crude is trading above $60 per barrel, down significantly from the year-ago level. The pricing environment was relatively more favorable a year ago, therefore hurting the upstream business of integrated energy players like Exxon Mobil Corporation (XOM - Free Report).

EIA projects the spot average West Texas Intermediate price for 2026 at $52.21 per barrel, lower than $65.40 for 2025. With XOM generating a king's size of its earnings from upstream operations, can it combat the prevailing softness in oil prices?

The advantageous assets where XOM is operating include the Permian, the most prolific basin in the United States and offshore Guyana resources. Although the assets have cost advantages, lower oil prices are likely to hurt profits. However, unlike many other companies, ExxonMobil can rely on its strong balance sheet.

XOM’s exposure to debt capital is significantly lower than that of the composite stocks belonging to the industry. The integrated energy giant can lean on its robust financials to navigate the low pricing environment, such as securing debt capital on favorable terms when the business scenario turns unfavorable.

CVX & EOG Can Also Brave Business Uncertainty

Chevron Corporation (CVX - Free Report) and EOG Resources Inc (EOG - Free Report) are two leading energy companies with a strong presence in exploration and production activities. The softness in crude prices is also hurting the bottom line of both CVX and EOG.

Like XOM, CVX and EOG have strong balance sheets. Debt to capitalization of Chevron and EOG is relatively lower than the industry, suggesting a considerably lower exposure to debt capital. Hence, they can brave the uncertainty of the business environment.

XOM’s Price Performance, Valuation & Estimates

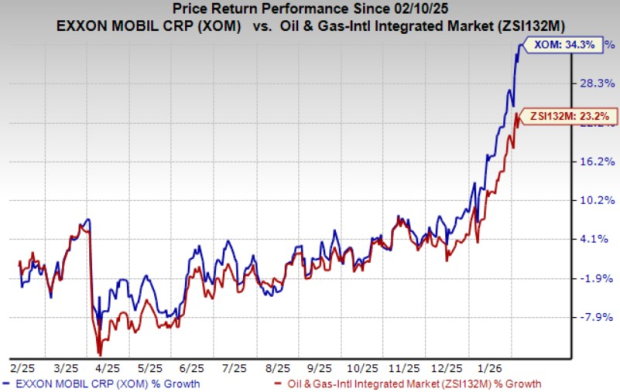

Shares of XOM have gained 34.3% over the past year compared with the 23.2% improvement of the composite stocks belonging to the industry.

Image Source: Zacks Investment Research

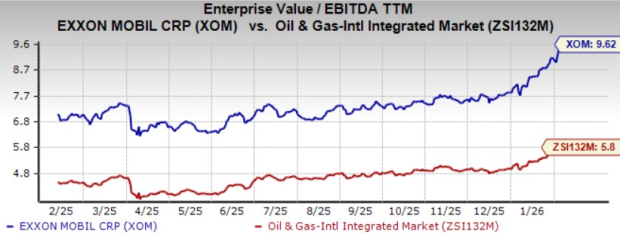

From a valuation standpoint, XOM trades at a trailing 12-month enterprise value to EBITDA (EV/EBITDA) of 9.62X. This is above the broader industry average of 5.80X.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for XOM’s 2026 earnings has seen upward revisions over the past seven days.

Image Source: Zacks Investment Research

ExxonMobil currently carries a Zacks Rank #3 (Hold).

More By This Author:

5 Securities & Exchanges Stocks To Watch Amid Increased Volatility

Should You Buy, Sell Or Hold Caterpillar Stock Post Q4 Earnings?

Quantum Computing 2026 Outlook: 2 Stocks For Long-Term Upside

Comments

Log in or sign up to join the conversation.