Market Analysis

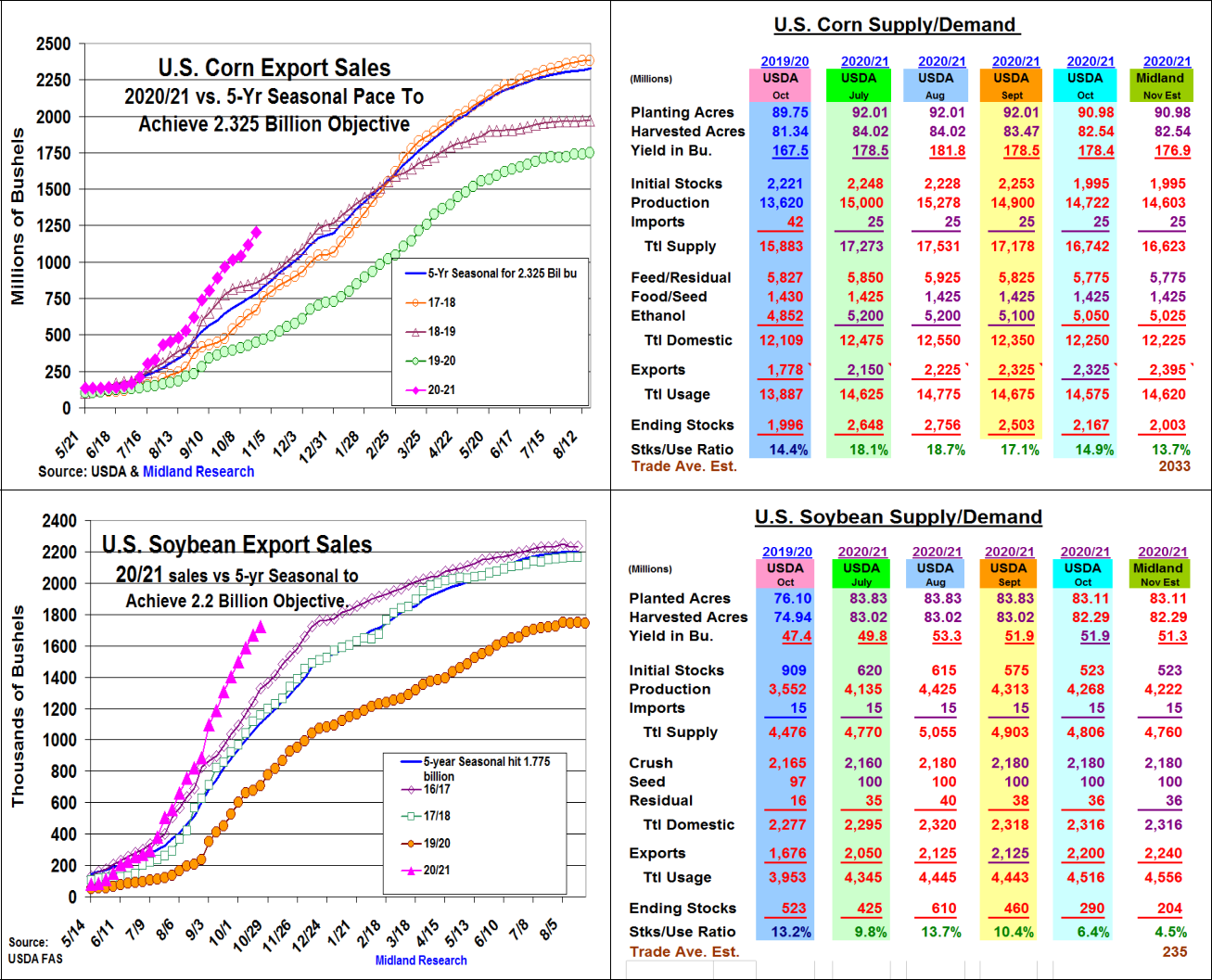

The upcoming USDA’s crop report has the trade anticipating slightly lower US corn (CORN) & soybean (SOYB) outputs resulting in declines in both crops 2020/21 balance sheets on Novem-ber 10. This fall’s strong overseas demand lead by China’s Phrase1 purchases have pushed both corn and soybean US export sales to record levels for the first 2 months of the US crop years. Smaller ending stocks are expected with this year’s S American growing conditions being closely watched because of 2020’s La Nina weather regime.

Except for last week’s cool & damp conditions, the US harvest has been proceeding at a rapid pace. This past summer’s dryness in the WCB & cold, wet planting conditions in the ECB reducing plant and ear counts have taken the top end of corn’s yield potential. Continued reports of corn on corn yield problems suggest that USDA will likely reduce the US yield by 1.5 bu. to 176.9 this month. This will be a hefty bounce back from 2019’s 167.5 bu yield, but the size of the crop could drop 119 million to 14.6 billion bu. with no likely change in the US harvested acres this month. Given the Black Sea & Argentina dryness, the USDA could increase corn’s exports by 70-100 million bu. This would cut US 2020/21 stocks to 2.003 billion bu & tighten corn’s stocks/use ratio to 13.7%, the lowest since 2015/16.

In soybeans, US late-season dryness & low moisture content of the 2020 harvest could slip the US yield by 0.6 bu to 51.3 bu on the next update. With US soybean exports 600 million ahead of its seasonal pace to hit the USDA’s 2.2 billion forecasts (81%), a 40-50 million bu increase is likely. This demand increase & a 46 million smaller crop could tighten the US 2020/21 stocks to 204 million bu, the smallest bean carryover since the 2015/16 crop year.

Dryness in the US SW, the Black Sea and Argentina potentially cutting these 2021/22 seedings & output has been wheat’s driving force. However, the USDA isn’t expected to change its US current 883 million bu ending stocks.

(Click on image to enlarge)

What’s Ahead:

November’s crop report & global weather are the CBOT’s major price factors. However, the trade’s need to source & move sizable corn & bean supplies into US export channels through the Mississippi river system before it closes in early December is also very supportive of CBOT prices this month. Hold corn & soybean sales, but advance Chicago & KC wheat sales to 60-65% at $6.55 and $6.10-15 price levels.

Comments

Log in or sign up to join the conversation.