Market Analysis

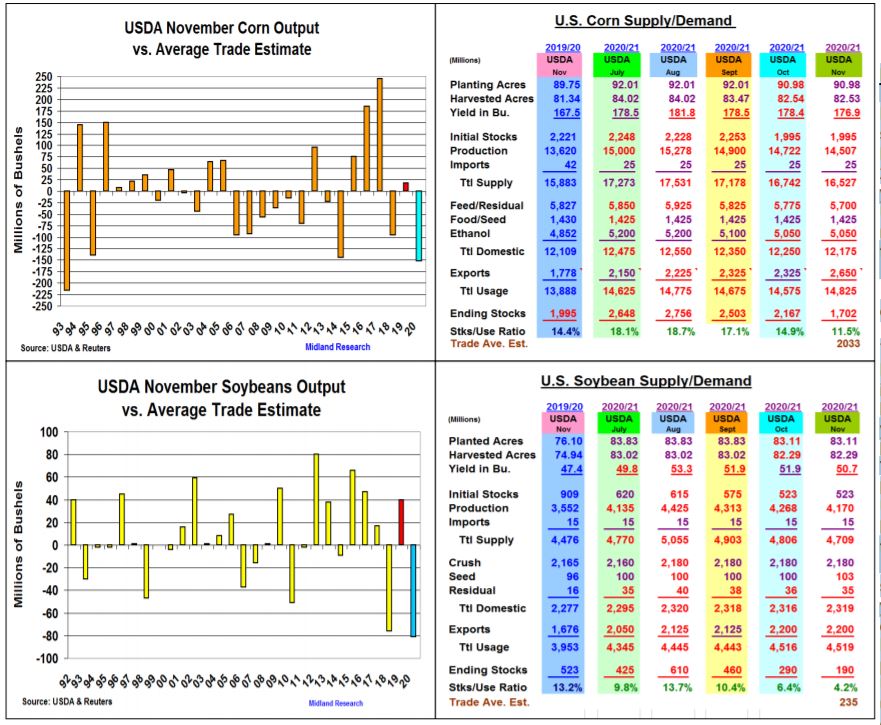

The USDA stunned the ag markets when they slashed their November US corn & soybean yields by their highest amounts since the early 1990s in their monthly crop updates this week. Keeping their US soybean demand strong and jumping corn’s 2020/21 total demand by 250 million bu helped tighten this year’s ending stocks to their lowest forecasted levels since the US 2014/15 crop years. 2020’s late summer dryness & above normal fall temperatures were the factors that cut yields further than the trade & producers were expecting.

In corn, this month’s sharp 2.6 bu drop in the US corn yield to 175.8 bu vs October was also 1.9 bu lower than the trade average guess & the largest trade miss in output (-152 mil) since 1993. Yields were off across the Corn Belt with ND (-15), MI (- 7), IL (-5), OH (-5) and KS (-5 bu) leading the way and IA, NE, MO & WI also slipping 2 bu in yields this month. Steady yields in MN, IN & SD and parts of the SE provided some stability, but disappointing corn on corn results were 2020’s the major yield factor to produce a 14.5 billion bu crop. Adding to today’s bullish was the USDA upping corn’s exports by 325 million bu. Their cut of Ukraine’s crop by 22% (-8.0 mmt) to 28.5 mmt because of summer heat & dryness was the reason. The USDA shaved 75 million off of feed demand because lower hog farrowing ideas, but this month’s 465 million cut in stocks to 1.7 billion is the largest Nov stock drop ever.

In soybeans, the US yield was cut by 1.2 bu to 50.7 bu. resulting in 4.17 bil bu crop. (down 98 million from Oct) This year’s dryness cut seed size and low harvest moisture reduced yields by 2 bu across the Midwest (OH, IN, IL, IA, WI & NE). Overall, this month’s output was 81 million bu, below expectations and the lowest difference since the 1990’s. The USDA didn’t change its US exports or crush outlooks, but upped seed demand for 2021 producing 100 million smaller ending stocks of 190 million bu. In wheat (WEAT), the USDA upped food demand by 5 mil bu which slipped US stocks to 877 million bu this month.

What’s Ahead

Overseas demand and the need to source and ship US corn (CORN) and beans (SOYB) before the US barge system is curtailed in early Dec remains a post harvest price factor along with S America’s growing conditions.

We are looking to advance corn & soybean sales to 65-70% on price advances to corn’s 2019 $4.45-60 highs and soybeans’ 2016 $11.90-12.10 highs that could occur later this month.

Comments

Log in or sign up to join the conversation.