Market Analysis

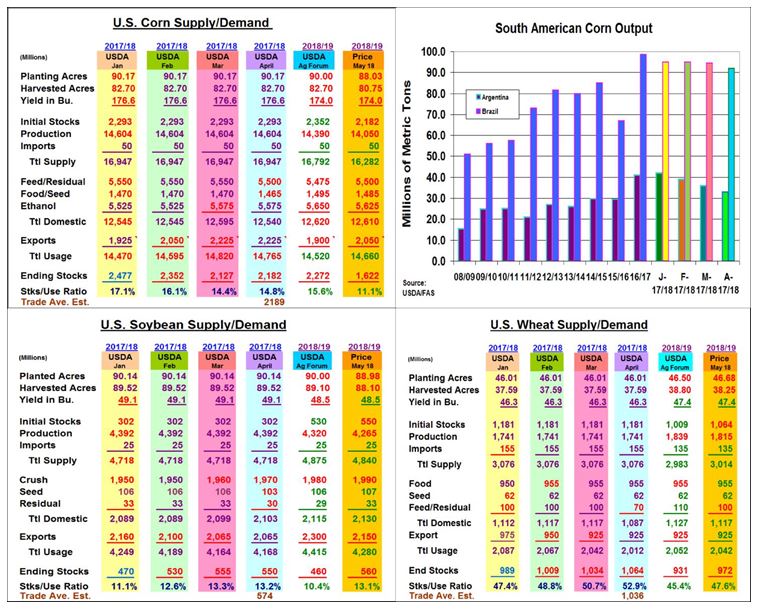

The USDA’s smaller South American corn and soybean outputs and their tightening of these world carryover levels lent support to the markets after the release of this week’s April report. As expected, both of Argentina’s corn and bean crops were lowered because of their ongoing drought while Brazil’s two outputs were mixed - beans up (+2 mmt) and corn down (-2.5 mmt). These changes and recent softening of the rhetoric in the US/China tariff scuffle may have prompted the USDA to limit changes in its US corn and soybean balance sheets this month.

In corn, March’s larger quarterly stocks did prompt the USDA to lower its feed demand, but by just 50 million bu. vs. ideas of 100 million decline. Corn exports were also left unchanged despite hefty overseas sales and both Argentina (-3 mmt to 33 mmt) and Brazil (2.5 mmt to 92 mmt) crop sizes being cut. The World Board did shave 10 million bu from food demand, which prompted a 60 million rise in stocks to 2.182 billion bu.-- near the trade’s average estimate. The smaller S American crops lowered the USDA’s world corn stocks by 1.37 mmt to 197.8 mmt.

In soybeans, the USDA raised the US crush by 10 million bu. to 1.97 billion because of our strong domestic and over-seas meal demand. Despite the 5 mmt drop in S. American (Arg -7 mmt & Brz+2 mmt) output, US exports were left unchanged given the cloud of 25% tariff being proposed on US bean imports in China. Small residual and seed usage declines left bean’s old-crop stocks 5 million lower at 550 million bu. South America’s smaller crops impacted the USDA’s world stocks by 3.6 mmt drop to 90.8 mmt.

In wheat, the USDA sliced US feed demand by 30 million bu because of its price relationship vs. other course grains in the US. This raised wheat’s old-crop stock level to 1.064 billion. World stocks were also raised 2.33 to 271.22 mmt due to a multi-year change in Iran’s wheat demand boost-ing April’s beginning stocks & a jump in Morocco’s crop.

(Click on image to enlarge)

What’s Ahead

The market has digested the latest S. American crop numbers and modest USDA old-crop balance sheet changes. Given 2018’s smaller US corn and soybean planting intentions, the focus is likely switching to the US planting season and its yield implications. With smaller seedings, US yields have become the main price factor along with the current Chinese trade conflict. Look to add to sales on price strength.

Comments

Log in or sign up to join the conversation.