Image: Bigstock

High-yield dividend stocks often attract investors when share prices retreat, creating opportunities to lock in higher income streams.

That has become the case for telecom and communications giants Comcast (CMCSA - Free Report) and AT&T (T - Free Report), both of which have recently traded near their 52-week lows of around $22 a share.

For income investors seeking reliable cash flow from established companies, the recent weakness in Comcast and AT&T stock raises an important question: Are these quality dividend payers trading at bargain prices, or are their declines signaling deeper concerns?

Why Comcast and AT&T Stock Have Declined

While both companies operate in communications and connectivity, the reasons for their stock weakness are somewhat different.

Comcast has struggled with persistent broadband internet subscriber losses as consumers increasingly turn to fixed wireless alternatives offered by telecom competitors. Despite posting solid earnings results, investors have remained concerned about slowing growth in the company's core cable broadband business as well and ongoing pressures in its media operations. The market has questioned the long-term growth outlook for traditional cable providers as competition from digital streaming services intensifies.

AT&T, meanwhile, has faced investor concerns related to its substantial debt burden, competitive wireless pricing pressures, and occasional free cash flow disappointments. Although AT&T continues to add fiber and wireless subscribers, investors remain cautious about whether this growth will be sufficient enough to offset heavy capital spending requirements and ongoing debt reduction efforts.

The result is that both stocks have drifted lower despite generating significant cash flow and maintaining their dividends.

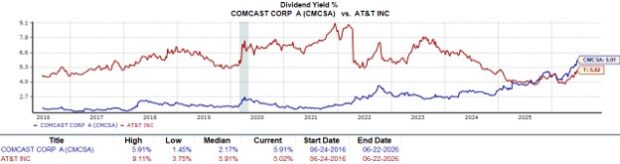

Comcast and AT&T Dividend Comparison

Following its recent selloff, Comcast's dividend yield has climbed to nearly 6%, making it one of the more compelling income opportunities in the communications space. The company continues to generate substantial free cash flow from its broadband, business services, media, and entertainment operations, supporting both its dividend and long-term capital allocation strategy.

AT&T also remains an appealing income stock with a dividend yield around 5%. The telecom giant benefits from recurring wireless and broadband subscription revenue, which provides a stable cash flow base to support shareholder payouts. Plus, management has continued to emphasize free cash flow generation and debt reduction while maintaining its dividend.

Image Source: Zacks Investment Research

That said, Comcast currently offers both the higher yield and stronger dividend-growth profile. To that point, Comcast has increased its dividend for 18 consecutive years, with annual dividend increases dating back to 2008.

On the other hand, AT&T was once a Dividend Aristocrat with 36 consecutive years of dividend increases, but that streak ended when management cut the dividend by roughly 47% in 2022 following the WarnerMedia spinoff. Since then, AT&T has maintained its dividend at approximately $1.11 per share annually rather than increasing it.

It's also noteworthy that Comcast has the more attractive payout ratio of 33% compared to AT&T's 51%, indicating a wider margin of safety for future dividend hikes, although both companies appear to have well-covered payouts.

Image Source: Zacks Investment Research

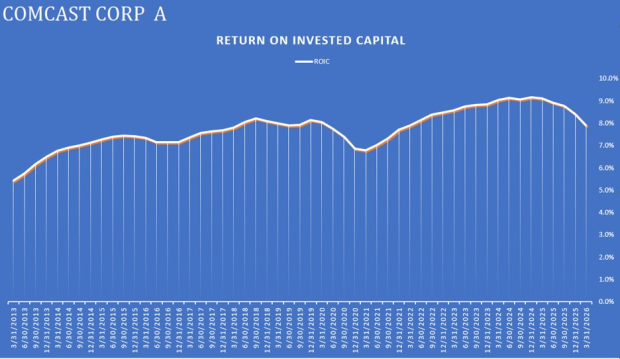

Looking Beyond Yield: Debt and Return on Invested Capital

Income investors should never evaluate dividend stocks based solely on yield. Long-term dividend sustainability often depends on balance-sheet strength and the ability to generate attractive returns on invested capital (ROIC).

Comcast's Financial Position

Comcast maintains a sizable debt load, but its financial profile remains manageable given the company's strong cash generation capabilities. Comcast continues to produce billions in annual operating cash flow and free cash flow, allowing it to support dividends, repurchase shares, and gradually manage debt obligations.

From an efficiency standpoint, Comcast's ROIC recently stood near 8%, reflecting a business that continues to generate returns above many traditional telecom peers despite competitive pressures.

Comcast currently has $272 billion in total assets compared to $175 billion in total liabilities, which includes $93 billion in long-term debt.

Image Source: Zacks Investment Research

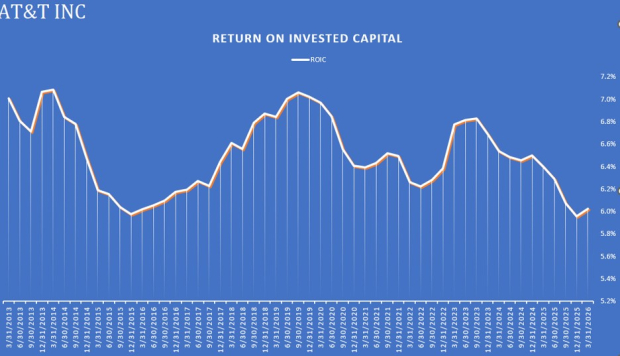

AT&T's Financial Position

AT&T's balance sheet remains the larger concern. Although AT&T has significantly reduced debt since its media divestitures, leverage remains elevated compared to many dividend-paying blue chips. Management continues to prioritize debt reduction while simultaneously investing heavily in fiber expansion and 5G infrastructure.

The positive news is that AT&T's recurring revenue model generates predictable cash flow, helping support both its dividend and deleveraging plans. However, investors should recognize that the company's capital-intensive business model leaves less flexibility than Comcast's in the event of an economic slowdown or increased competition, with AT&T’s ROIC at around 6% at the moment.

AT&T currently has $420 billion in total assets but has roughly $294 billion in total liabilities, which includes $127 billion in long-term debt.

Image Source: Zacks Investment Research

Comcast and AT&T’s Cheap Valuations

Of course, what may be most compelling to investors is that both stocks are trading under 10X forward earnings and are beneath the often preferred level of less than 2X forward sales.

Image Source: Zacks Investment Research

Conclusion & Strategic Thoughts

Comcast and AT&T offer attractive income opportunities for investors willing to tolerate moderate business and industry risks.

For long-term income investors looking to add positions in established, cash-generating companies that are trading near 52-week lows, both stocks warrant consideration. Still, investors should balance the attractive yields against the competitive and operational challenges facing each company.

For now, Comcast and AT&T stock both land a Zacks Rank #3 (Hold), suggesting investors who already hold positions may want to maintain them while monitoring future improvements in business fundamentals and earnings trends. In regard to adding positions, there could still be better buying opportunities ahead, although it's getting hard to overlook these top blue-chip dividend stocks at their current levels.

Comments

Log in or sign up to join the conversation.