Market Analysis

The market’s attention has been on this spring’s US planting season, which has been impacted by cold temperatures across the northern growing areas while the southern regions have recently experience excessive rainfall and flooding. These conditions have delayed corn plantings last week and postponed soybean seedings, but soybean yields don’t slip substantially until numerous acres are delayed in late May and June.

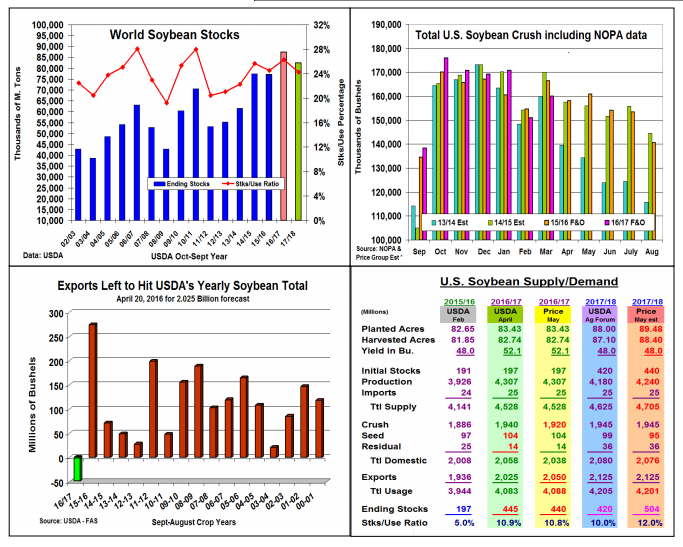

This year’s record S. American crop and earlier US indications that producers were considering planting 6 million more beans than 2016 have left the soy complex on the defensive this spring. However, given the potential for both US and S America’s yields to return back to their recent trend vs. the dramatic yield jumps in both producing regions the past year may reduce the world’s output by 1.5%. Given the strong ongoing demand for protein from Asia, a 2.5% rise in soybean consumption seems appropriate after this year’s projected 5.7% increase in usage. Overall, 2017/18’s ending stocks could decrease by 4.5 mmt to 82.9 mmt, but this carryover still would be the second largest ever.

March’s 2nd consecutive lower than expected monthly Fats & Oils US soybean crush at 160 million bu. has the market expecting a cut in 2016/17’s bean processing estimate by 20 million to 1.92 billion on Wednesday. Countering this trend has been the ongoing strength in overseas sales which are 57.5 million above the USDA’s current forecast. This suggest a 25 million larger export forecast could drop the US old-crop stocks by 5 million to 440 million, These large carryover supplies make it tough to not have larger overall supplies in the upcoming US 2017/18 crop year. With the USDA likely to utilize their new-crop Ag Forum demand outlook given steady to lower 2017/18 prices, US soybean stocks could rise to 504 million, the highest level since 2006/07 crop year.

What’s Ahead

Soybean’s stocks to use ratio isn’t expected to plunge to 2006/07 levels of 18.7% with our world soybean demand now 50% stronger and US soybean consumption also one third larger at 4.2 billion bu. However, a significant production problem will probably needed to surface in the world for a dramatic jump in soy prices in the upcoming crop year since the world’s 2017/18 ratio will be 24.3% with 82.9 mmt of beans.

Comments

Log in or sign up to join the conversation.