Risks abound on UBS's balance sheet, off the balance sheet, and across the pond. Yet, UBS trades at an astonishing premium to its peers. We are initiating a SELL rating.

INVESTMENT THESIS

Despite its de-risked balance sheet, UBS faces significant credit exposure to troubled assets, along with associated counterparty risk on insured and hedged products.

UBS trades at a huge premium to its peers when comparing earnings and book multiples. We expect its multiple to contract as further losses and write-downs mount in the face of a weakening global economy.

Our price target is based both on historical and peer group price-to-book multiples, from which UBS currently trades at an 81% premium.

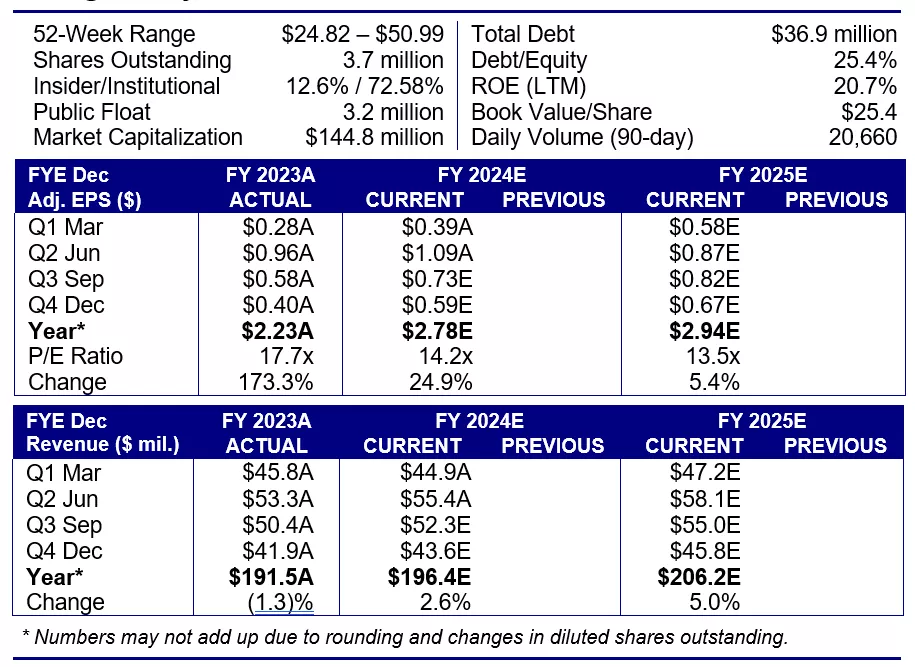

Our forecast for 2009 is below the current consensus. With sustained profitability in question for 2009, even our bearish forecast could prove to be too positive.

RISKS TO OUR SHORT CALL

Like many governments around the world, the Swiss National Bank intervened on UBS's behalf last year, and could step in to assist UBS in the future if needed.

There is an all out blitz on short positions, including changes to up-tick rules, mark-to-market accounting, and speculation of government purchases of troubled assets. Whether perception or reality, headline risks are a plenty.

SUMMARY

Without question, the biggest banks in the world made some hideous decisions over the last few years. Even when they made seemingly good decisions, such as buying insurance on questionable securities, they lost money since many of these hedged and insured positions proved worthless themselves. By far the worst example of insurance gone wrong is AIG.

Reading through AIG's SEC filings is like watching a spoof on a horror movie – the blood is real, but it's hard not to laugh. In some instances, AIG could not even estimate its loss exposure to some of its special purpose entities. When AIG could estimate its potential losses, the numbers were often in the hundreds of billions. Unfortunately for many European banks, UBS included, AIG ventured across the pond to sell similar faux insurance as it did to US banks. As Chairman Bernanke illustrated last Sunday on 60 Minutes, bailing out AIG was a global necessity, despite the bitter after taste that is left after using tax payer money to attempt to fix asinine decisions.

This past Sunday, AIG released a document that detailed where the bailout money was going in the 4th quarter. Many of the expected names were on the list, including Goldman Sachs (NYSE:GS), Bank of America (NYSE:BAC), Merrill Lynch, and Citigroup (NYSE:C). Yet, some of the biggest payouts (from September to December of 2008) went to non-US banks. Barclays (NYSE:BCS) received over $8 billion; Societe Generale (OTCPK:SCGLY) received over $12 billion; and Deutsche Bank (NYSE:DB) received over $13 billion. UBS, while not as extreme, received $5 billion from AIG over this period. Nevertheless, in UBS's recently filed 20-F (annual filing), the company specifically mentions continued risks and potential further writedowns related to unreliable credit protection and deteriorating creditworthiness of monoline and other providers of credit protection.

While many US banks have been hit hard with writedowns, losses, and resulting drops in stock prices, many European banks continue to trade at premium multiples despite facing similar if not more extreme credit risks and losses. Despite losing over 20 billion CHF last year, issuing a cautious forecast for 2009, and facing existing exposure to credit losses and revaluations, UBS trades at a 105% premium to its peers' average price-to-book multiple (P/B), and a 18% premium to the group's average price-to-earnings multiple (P/E) for 2009. Furthermore, we believe UBS' core businesses will continue to struggle in the year ahead, particularly given the company's current cost structure, which does not match UBS's assets under management (AUM) or business activity.

We are issuing a 2009 earnings forecast well below the current consensus of $1.22. We are issuing a price target based on a lowered P/B multiple, decreasing consensus earnings expectations, and a reflection of the company's existing exposure to toxic assets in Europe and the US.

Comments

Log in or sign up to join the conversation.