Image: Bigstock

Key Takeaways

Realty Income posted 2025 AFFO of $4.28 per share and guided 2026 AFFO in the range of $4.38-$4.42.

The company deployed $6.3 billion in 2025 and targets $8 billion in 2026, banking on favorable investment spreads.

Realty Income maintains 98.9% occupancy, 104% rent recapture, and strong liquidity of $4.1 billion.

Realty Income (Free Report) closed out 2025 with another steady quarter, reinforcing its reputation as one of the most consistent net-lease REITs in the market. The company’s focus remains clear: scale its global real estate platform, protect the balance sheet and deliver dependable monthly dividends backed by recurring cash flow.

From a stock performance standpoint, shares have remained sensitive to interest rate expectations over the past year, as is typical for net-lease REITs. While volatility persisted through 2025, the stock stabilized into year-end as investors responded positively to improving capital markets access, active investment deployment, and a clearly defined 2026 growth plan.

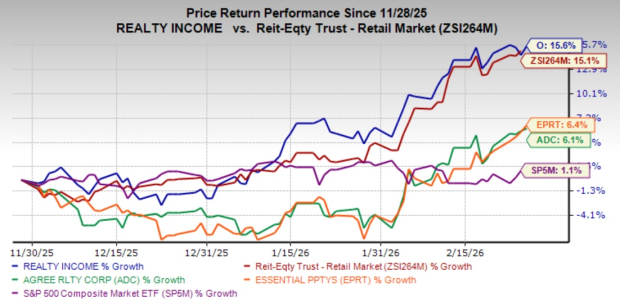

In the past three months, Realty Income has seen its stock move higher, with shares gaining 15.6%. Realty Income stock has not only outpaced its close peers, such as the free-standing REITs, Agree Realty Corporation (Free Report) and Essential Properties Realty Trust, Inc. (Free Report), but it also outperformed the Zacks REIT and Equity Trust - Retail industry and the S&P 500 Composite.

Image Source: Zacks Investment Research

While the company’s strategic investments augur well for long-term growth and a dividend hike gives a boost to investors’ sentiment, its investment thesis presents both compelling growth drivers and legitimate concerns. Let’s explore them to ultimately arrive at the decision of whether to hold the stock for now, buy shares, or sell and book profits.

Earnings Stability Supports the Thesis for Realty Income

The core story remains cash-flow durability. Full-year 2025 adjusted funds from operations (AFFO) of $4.28 per share represent continued earnings stability despite a higher interest rate backdrop. Fourth-quarter AFFO of $1.08 per share reflects consistent rent collection and strong portfolio occupancy.

Importantly, 2026 guidance of $4.38-$4.42 per share implies modest year-over-year growth. While not aggressive, this outlook reflects a realistic approach to capital deployment and underwriting spreads. For a company primarily owned for income stability rather than rapid growth, this steady trajectory is meaningful.

Aggressive But Disciplined Investment Activity of Realty Income

Realty Income deployed $6.3 billion (its pro-rata share was $6.2 billion) in 2025 investments at a weighted average initial cash yield of approximately 7.3%. Fourth-quarter activity alone totaled about $2.4 billion. The 2026 target of $8 billion signals confidence in sourcing opportunities across the United States and Europe.

The company continues to leverage multiple channels, including direct acquisitions, sale-leasebacks, and partnerships. Management highlighted a strong investment pipeline and the ability to transact across different structures, which helps maintain pricing discipline. If spreads remain favorable, this scale can drive incremental AFFO growth over the next several years.

Balance Sheet and Liquidity Remain Strengths for Realty Income

Liquidity stood at more than $4.1 billion at 2025-end, providing flexibility to fund the 2026 investment pipeline. Net debt to adjusted EBITDA remains within management’s targeted range, supporting its strong investment-grade credit ratings.

Following the year-end, the company also issued convertible senior notes and used proceeds to refinance debt and repurchase shares, optimizing its capital stack. The weighted average cost of capital remains competitive relative to many peers, an important advantage when underwriting large-scale transactions in a competitive market.

Portfolio Metrics Show Resilience for Realty Income

Portfolio fundamentals continue to look solid. Occupancy stood at 98.9% at year-end 2025, reflecting the defensive nature of its tenant base. The company reported rent recapture rates of roughly 104% on properties re-leased during the year, indicating pricing power on turnover.

The portfolio spans thousands of properties across the United States and Europe, with a long weighted average remaining lease term. Tenant diversification remains broad, with exposure to service-oriented and non-discretionary retail categories that tend to perform relatively well during economic slowdowns.

The Key Risk for Realty Income: Growth Depends on Spread Environment

The main area of caution is execution risk tied to its $8 billion 2026 investment plan. Sustaining AFFO growth depends on maintaining attractive investment spreads over its cost of capital. If interest rates remain elevated or cap rate competition intensifies, incremental earnings growth could moderate.

Management also incorporated conservative credit-loss assumptions for 2026, acknowledging that certain tenants remain on the watch list. While current occupancy is high, any meaningful tenant disruption could weigh on near-term earnings momentum.

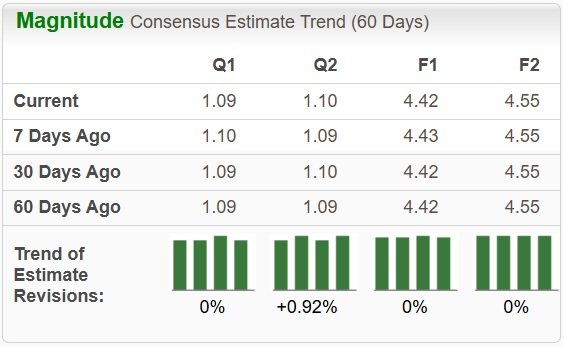

Realty Income’s Estimate Revisions and Valuation

Estimate revisions reflect a somewhat mixed trend. Over the past seven days, estimates for the company’s 2026 FFO have been revised modestly downward, while the estimate for 2027 FFO per share has remained unchanged, indicating a balanced view of growth and cost pressures.

Image Source: Zacks Investment Research

Valuation-wise, Realty Income stock has been trading at a forward 12-month price-to-FFO of 14.97X, below the retail REIT industry average of 16.54X but ahead of its three-year median. The stock has also been trading at a reasonable discount compared with its industry peers, Agree Realty Corporation and Essential Properties Realty Trust.

This valuation disparity might not be as favorable as it seems, however. Agree Realty has been trading at a forward 12-month price-to-FFO of 17.47X, while Essential Properties Realty Trust has been trading at 16.35X.

Additionally, the Value Score of D suggests that Realty Income may not be a bargain at recent levels. Still, the company’s strategic investments, consistent dividend growth, underpinned by predictable rental income, keep it appealing for long-term income-oriented investors.

Image Source: Zacks Investment Research

Wrapping Up on Realty Income

Realty Income delivered another predictable quarter with solid AFFO, high occupancy, and a clear 2026 growth roadmap. The balance sheet is well positioned, liquidity is ample, and the dividend remains well covered by cash flow. At the same time, growth expectations are moderate and depend on maintaining favorable investment spreads in a competitive market.

For income-focused investors seeking stability and monthly dividends, the stock has continued to serve its purpose. However, with modest projected growth and macro sensitivity to rates, the risk-reward appears balanced at recent levels. Based on the latest results and outlook, as well as estimate revisions and valuation, holding on to shares could be a sensible approach, given the company's strong history of monthly dividend growth and its strategic focus on high-quality property sectors.

At present, Realty Income carries a Zacks Rank #3 (Hold) rating. Note that anything related to earnings presented in this write-up represents funds from operations (FFO) — a widely used metric to gauge the performance of REITs.

Comments

Log in or sign up to join the conversation.