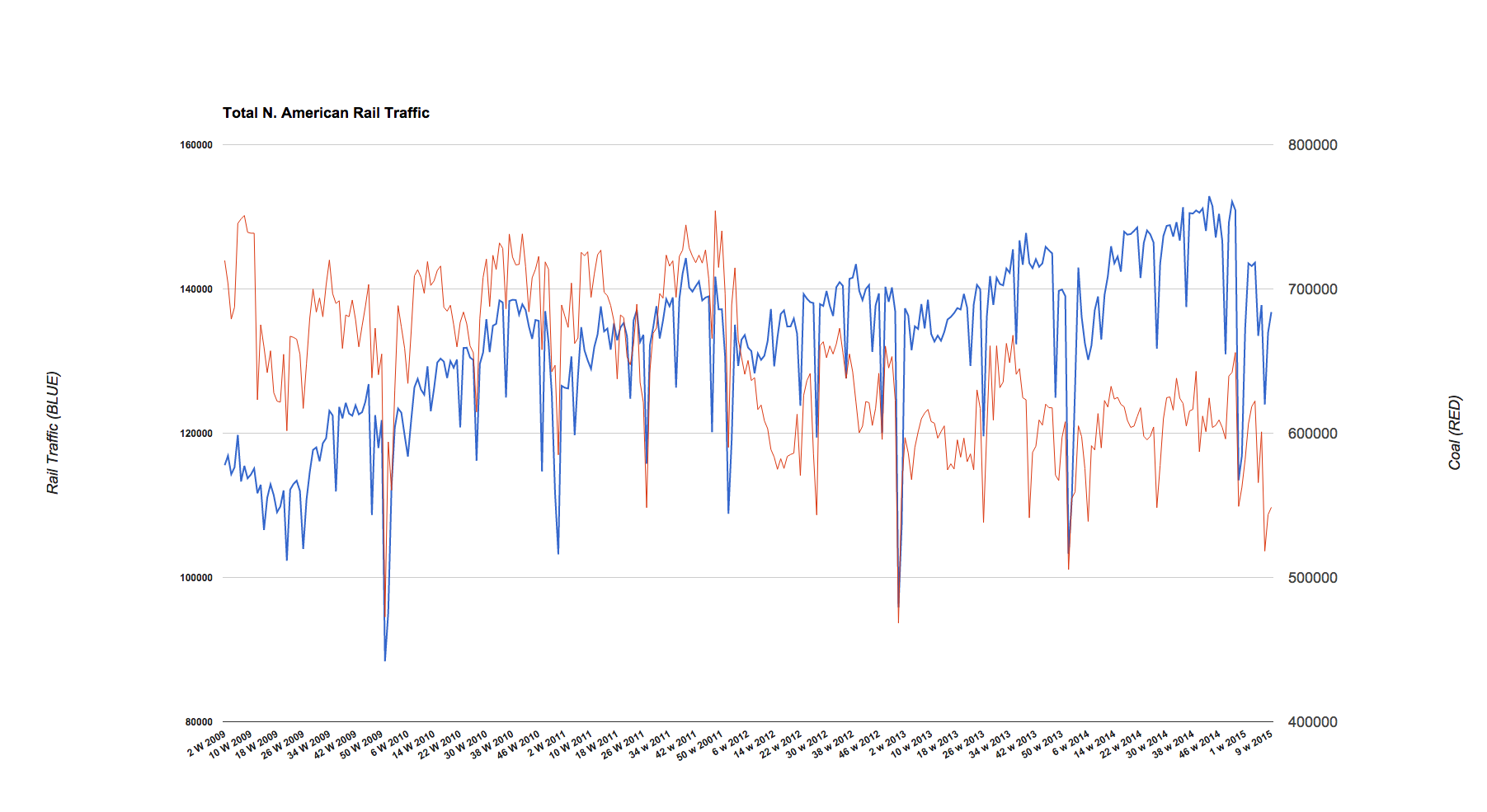

Total N. American rail traffic ran a bit behind 2014 for the month of February (marginally, not materially):

Click on picture to enlarge

So, now the question we need to ask is: “Is this a sign of an economic slowdown or just a slight dip in what has been a 5 year improvement?”

I am going with a slight and temporary dip. Why?

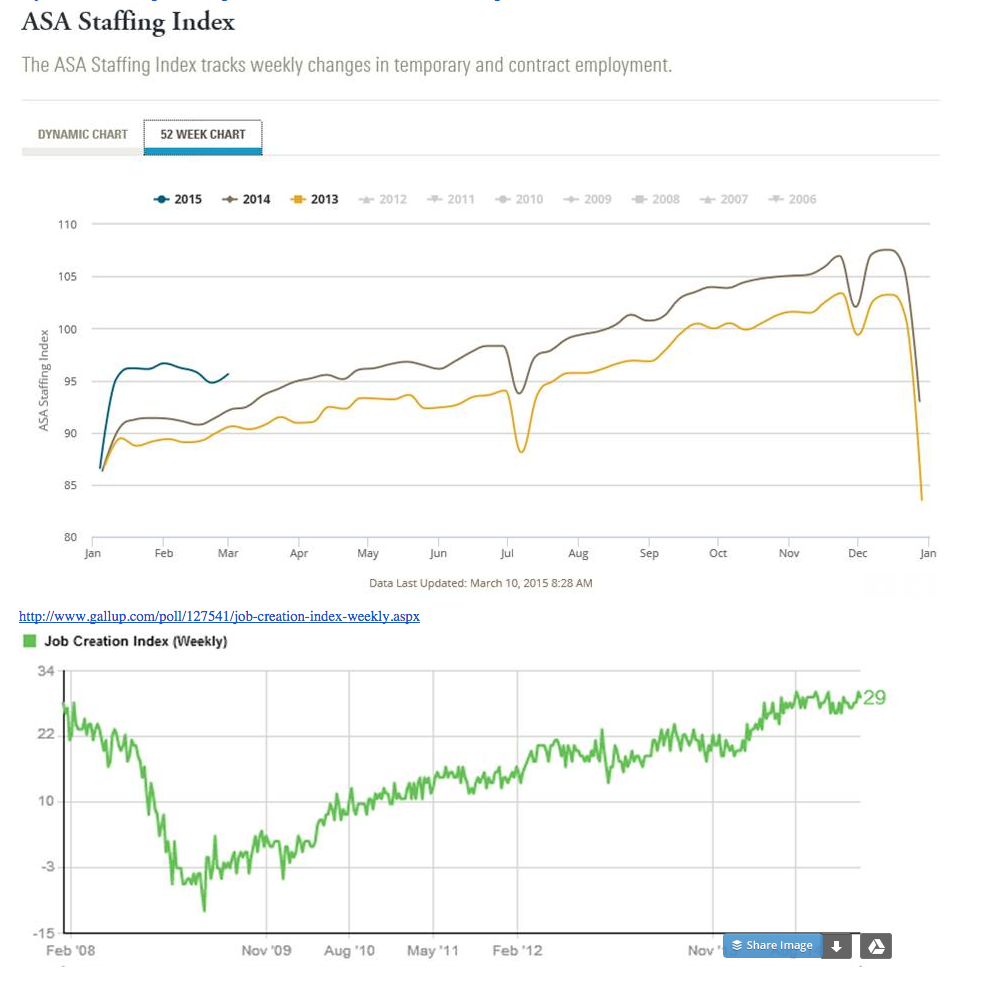

Other major indicators continue to improve, especially employment and as employment goes, so goes everything else:

“Davidson” submits:

The American Staffing Assoc Staffing Index and Gallup’s Job Creation Index are called ‘high frequency’ because they are released weekly rather than the monthly release of most other economic indicators. This week’s releases are shown below. The uptrends in these employment indicators continue with both remaining at all time highs for each series. (The ASA Staffing Index has significant seasonality and current readings are at their highest vs. prior readings at this point of the seasonal variation.)

Click on picture to enlarge

The long term directionality of equity markets is in the economic data. It is not how good investors feel at the moment. The correlation is actually the reverse of consensus opinion. If the economy continues to rise, then market psychology will catch up and drive equity markets higher no matter the valuation. This occurs in my opinion primarily because there exists a considerable fraction of investors who believe in “The Invisible Hand” concept. In other words if the market moves higher on positive economic news which many did not expect, investors come to believe than valuation levels are justified. The same is true during economic contractions. This is what drives stocks to be priced at 10x-30x revenue and 100x+ earnings when no Value Investor would ever pay such a price. Most investors chase what they perceive is ‘growth’ by chasing headlines with the belief that the ‘market knows best’. As a Value Investor, I have seen countless number of investors lose using this approach. The worst approach in my opinion is in believing that one needs to actively trade one’s account. The value of companies change slowly. Net/net corporations which create real increases in returns do this over several years not the weeks and days we so often hear exclaimed by the trading community crowding the media. It takes time for investors to recognize this before they climb on board.

The equity market’s general direction as forecasted by economics is in one word “HIGHER”!

The forecast is not higher tomorrow or next week, but at least the next couple of years and if housing comes on stream as expected as long as 5yrs-7yrs.

Further we are seeing the effect of lower gas prices on the consumer. Despite the brutal January and February most of the North and East coast saw, restaurant sales seem to have grown YOY. This is a primary “discretionary” expenditure and consumers seeing their fill-up bill cut almost in half from 2014 are now spending that extra cash which will further boost the economy. Speaking for myself, seeing my bill to fill up the suburban cut from >$100 to ~$55-$60 has meant a few more meals out for the family. . … Again, I operate under the “we aren’t really any different from most other families” mantra (except maybe we have more numbers) so if we are spending it, so are millions of other families.

Back to rail traffic. In the North and East Coast, especially in February, rail traffic was undoubtedly affected by the snow. States of emergencies were declared up and down the east coast from the Mid-Atlantic states into New England and rail traffic here in MA was ground to a halt. That clearly affected shipments. In fact through January 2015 we were comfortably ahead of 2014 in total rail traffic until the second and third weeks of Feb when storm after storm hit and rail traffic plummeted. Now, some might be inclined to think the culprit in oil due to rig count decreases but the “chemical/petroleum” category is actually up slightly YOY. What is it then? Coal. The decline in coal shipments in February almost to the car load matches the overall decline in total traffic for Feb. We can assume the unusually harsh winter also affect coal mining operations.

Where do we go from here? I am thinking we see a steady increase in rail traffic and begin to see the YOY increases this spring we were seeing in January.

Comments

Log in or sign up to join the conversation.