My title above may not sound familiar to those under 45 or so. But it is perfect to describe QXO and its chairman, Brad Jacobs! (Whoever first identifies the rest of the quote without looking it up gets…well, bragging rights, anyway.)

QXO: An Overview and an Update

I chose to update my previous analysis of QXO (found here) because this company is today one of the most aggressive yet trial-by-fire "roll-up" opportunities you can still buy at a fair price.

QXO is just the latest in a line of multi-billion-dollar companies founded by Brad Jacobs, a very clever CEO with a reputation for taking "un-sexy," fragmented industries and consolidating them into massive powerhouses.

He did this with United Rentals (URI), XPO Logistics (XPO), and a company he sold to Waste Management (WM), among others. In each case, he acquired numerous smaller businesses that played a specific role in a particular region.

Think of it this way, not that this is exactly how Mr. Jacobs did it: What is more efficient, having one trash collector/sanitation engineer pick up the trash cans on one side of the street and a competitor's employee emptying the ones on the other side of the street, or making the process more rational by covering both sides of the street, saving time, gas, and maintenance, since there was no back and forth through the maze of different firms.

It would be the same with a thousand independent truckers who had to compete to be first in line for a load to go somewhere and then, all too often, had to deadhead back to their starting location, where they were a known and trusted entity with no load. Better to provide that trucker by going from location A to B to drop the load, picking up at B and going to C, ditto to D, then back to A to see his or her family and take a day or two to relax.

Aggregating individuals and small firms under the umbrella of a highly sophisticated, modern organization that can afford the most advanced technology to make life smoother and more profitable is what Brad Jacobs did with XPO, Inc. (XPO), a $26 billion Cargo Ground Transportation company.

The same "Jacobs Playbook" was used with United Rentals (URI). Numerous local or small regional companies were united under a single, very large banner, reducing marketing costs and streamlining the entire rental process.

In these previous cases and in the current case, QXO, the strategy is not just to buy up companies; it is to build a platform that streamlines operations, creates significant manpower savings, often makes employees happier and more successful, and provides a better product for buyers.

QXO is the latest in this line. Its target? The $800 billion building products distribution industry.

This industry is hugely fragmented, with not just hundreds but thousands of small mom-and-pop distributors. Most are, to be kind, behind the times technologically because "that's the way Dad always did it" or because they just don't have the capital to invest in a better way.

When I tell people that there is a company that is important to AI and a whole lot of other industries, I see their eyes open wide. Then, I tell them it is a fast mover in the building products distribution industry, yes, that's correct, the building products distribution industry, and I see their eyes glaze over as their head hits their chest.

Many still think, "Do these people spending zillions of dollars on nuts and bolts realize we are in a New Era? It's all about AI nowadays. You know, the Brave New World where a high school kid with a D- grade point average can write a brilliant piece on quantum mechanics and follow it up with one on string theory!"

Ah, but QXO is on the cutting edge of using the most advanced AI-driven logistics to achieve higher margins, alongside a marketing style that smaller competitors can't match.

But They Do Have Big Competitors, Right?

Yes, but not as many as there were a while ago.

QXO first acquired $11 billion Beacon Roofing (BECN), then the largest roofing company in America. It still is the biggest, just under the "roof" of QXO. After QXO's acquisition of Beacon (a year ago today), it is now the largest publicly traded distributor of roofing, waterproofing, and other building products in the U.S.

Then, earlier this year, QXO acquired Kodiak Building Partners for $2.25 billion. This gave them a massive footprint in lumber, even more in roofing, and other construction supplies. Kodiak, despite its name, was (and still is, as part of QXO) particularly strong in high-growth areas far from Kodiak, like Florida and Texas.

Finally, this month, QXO announced a massive $17 billion deal to acquire TopBuild (BLD), the #1 leader in North American insulation, along with other offerings for the building trades.

How About Even Bigger Competitors Like Home Depot (HD) and Lowe's (LOW)?

Ah, yes. Lowe's and Home Depot have outbid QXO for some prizes. Home Depot and QXO were both bidders for SRS Distribution, but QXO decided it was not worth the price Home Depot ultimately paid (a little more than $18 billion).

Ditto for Home Depot's offer of $110 per share for GMS, significantly higher than QXO's offer of $95.20 per share. Brad Jacobs has never engaged in an ego-fest to claim the prize. A fair price is offered. If not accepted, move on.

Lowe's also bought Foundation Building Materials and Artisan Design Group, both privately held building materials giants.

Why did HD and LOW want to acquire these large firms? They want to build up the "Pro" side of the business, that area where massive amounts of lumber, roofing material, and insulation are sold to contractors, large, huge, and small.

I wish them well. I shop at both HD and Lowe's. But I must say they are not laser-focused on their "customer" like QXO is. QXO is not trying to satisfy little old me coming in to pick up a new tape measure like Lowe's and HD.

Having these two different tracks may work well for these two consumer giants over time as they integrate - and in some ways, must separate - their two primary clients: consumers who buy a little here and there and a much smaller contingent of contractors and other pros who might buy seldom but in large quantities when they do buy.

In fairness, these new subsidiaries will be treated differently. If you are a pro, it isn't like your boss is going to say, "Hey Jim, on your way home tonight, pick up 400,000 drawer clasps and 20 miles of fiber-optic cable, will you?"

Ancillary to this, one other thought. I recently needed to buy studio-quality speakers, so I went online looking for reviews from various experts. When it came time to select a vendor, who should pop up with the same price as Amazon (AMZN)? And the same free delivery, without even being HD's version of a Prime member.

I think at some point Home Depot needs to decide if it wants to be a Costco (COST), a "HOMEowners Depot," or a building materials distributor. Maybe they can be all three. Just saying.

Wait a Minute, the Companies Being Bought by QXO, HD, and LOW Aren't Exactly Mom-and-Pop Distributors

No, they certainly are not. I think that in QXO's case, they wanted to hit the ground running, and the way to do that was to buy companies somewhat like themselves that were already on stage 2 or 3 of the aggregation of smaller businesses.

But Why Now? Nobody is Buying Homes, So What Contractors Et Al is QXO Going to Sell to and Profit From?

Even in a high-mortgage-rate environment, QXO understands its market. The U.S. has a structural housing shortage and aging infrastructure that requires constant maintenance.

And even if fewer homes are being built, there are those condos and apartment buildings, airports and seaports, roadways and highways, office buildings and data centers, defense company needs, etc.

What QXO brings to the party is laser-focused on one group: professionals. And when they bring other companies into the mix, they upgrade to the highest levels of current technology, including AI. Most of these companies still use legacy software. QXO applies AI for demand forecasting, price optimization, and route planning.

By doing so, QXO can upgrade a business with a 3-6% margin to a 10%, 12%, or 15% margin business.

The downside? Because QXO is spending billions on acquisitions and integration, its "reported" earnings can be ugly (or even nonexistent) as it moves toward full integration.

Another downside? The average financial analyst has been trained from the beginning of their internship that when a company is paying partially in cash and partially in stock, to throw their hands in the air and yell, "Dilution! Dilution! Dilution!"

Yes, if the shares are going out and there is no quick return on that investment, dilution can reduce the price of QXO's shares faster than the profits can roll in to negate that loss. That is precisely why QXO moves at the speed of light (see my title) to ensure they do not tarry.

But if the TopBuild acquisition is successful, that will mean that QXO will become the #1 provider of insulation, the #1 or 2 in roofing, #1 in waterproofing, and #1 or 2 in lumber and other building materials.

Valuation

How do we value a company that has dilution from using shares for acquisitions and will increase its debt as well?

Very carefully.

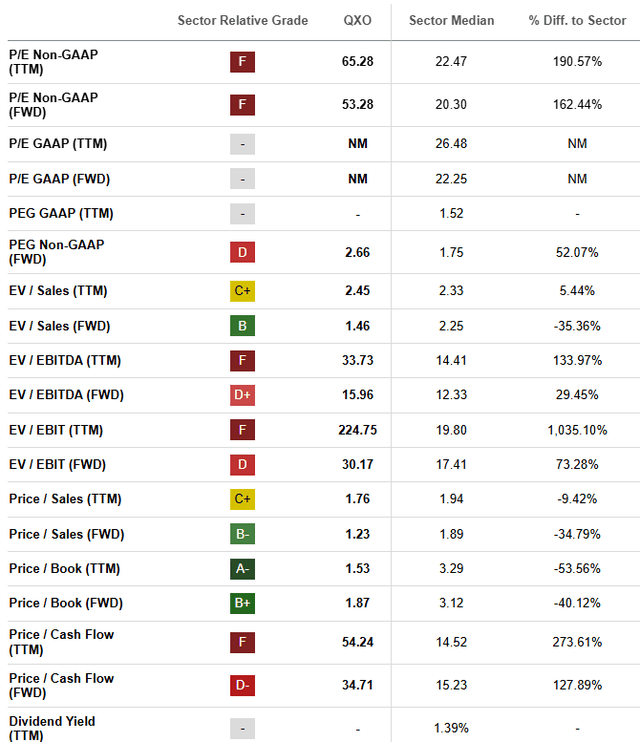

The usual valuation numbers are ug-lee. I have deleted from Seeking Alpha's chart below the "5-year" columns. There is nothing meaningful there since there was no QXO 5 years ago.

There are a couple of things that pleasantly surprised me here - the PEG ratio, one of my favorite indicators, is not nearly as high as I thought it might be. And the Price/Sales and Price/Book are well corralled.

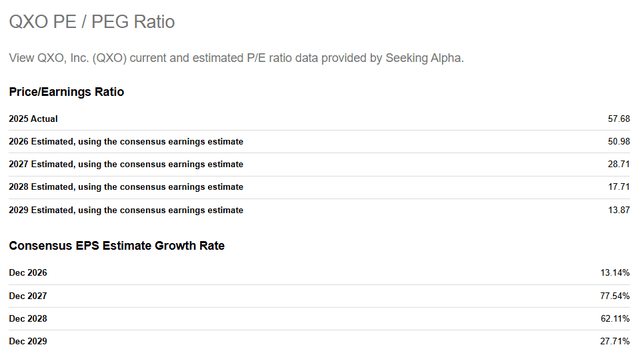

Speaking of the currently out-of-sight PE ratio, SA has compiled analysts' thoughts on what will happen going forward…

…and the estimated growth rates make sense to me as well. By 2027, I see a short runway, with a monster F-35 engine taking off, roaring ahead again in 2028, then slowing down to a still exceptional 2029.

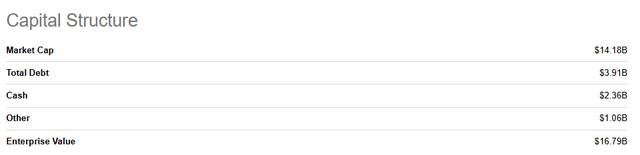

Finally, let's check the current capital structure. This is clearly before the TopBuild acquisition, as it should be, since the deal has not yet closed. Total debt is likely to rise. How quickly QXO can bring this to fruition and how much it can streamline and integrate TopBuild's operations will determine how quickly that debt is paid down.

Here are some notes from the press release issued by QXO on Sunday, April 19, announcing the TopBuild agreement. You can see the entire message here: QXO, Inc. - QXO to Acquire TopBuild for $17 Billion

"TopBuild is the largest distributor and installer of insulation and related building products in North America. The combination will bring together QXO's leading positions in roofing, waterproofing, lumber-related building materials, and associated products with TopBuild's insulation capabilities, creating a higher-margin business with expansive value-added offerings for customers.

"The transaction has been unanimously approved by the boards of directors of both companies and is subject to customary closing conditions, including approval by the shareholders of TopBuild and QXO. The acquisition is expected to close in the third quarter of 2026.

"Following the acquisition of TopBuild, QXO will have approximately 28,000 employees, 1,150 locations across all 50 U.S. states and seven Canadian provinces, and a fleet size of more than 10,000 vehicles."

Risks

I mentioned many already.

Shareholders of QXO will likely see their ownership percentage diluted. But the market has already corrected, either partially or completely; time will tell. The closing price of QXO on Friday, April 17, was $25, with a little over 10 million shares traded. From April 20 forward, with 5+ times the volume on that first day and high volume ever since, QXO declined to its close on April 29 of $19.61.

Clearly, old-time analysts had pulled out their slide rules, while the young analysts had queried AI, trusting it completely. It seems the dilution may already be accounted for in this price decline.

Another risk is that TopBuild, even with both CEOs describing the acquisition as all apple pie and ice cream, could be a tough nut to crack open. It might be a clash of corporate cultures below the glowing affinity each CEO seems to have for the other.

There will be debt to pay off. Again, handling the debt service will depend on how quickly dollars begin flowing into the married couple's bank account. This is not Brad Jacob's first rodeo.

I wrote my previous analysis with a title that tells you how I always look at the numbers, but understand there are some people, like Warren Buffett and Brad Jacobs, who add the right icing to the numbers cake. "QXO: I Am Buying The Company -- And The Man."

Other Risk Elements for the Entire Building Products Industry:

The Heavy Hand of Government. Government giveth and government taketh away. - sometimes in the same month. (Heck, these days sometimes in the same day) forcing or enticing foreign firms to build out massive infrastructure in the US to avoid more massive tariffs is a plus for building materials and building distributors today. Tomorrow is a question mark.

The current US economy. There is no doubt that interest rates and low housing starts have impacted the housing market. But so far, the foreign firms, the race to build data centers, the crumbling infrastructure at the national level, and the need for refurbishment/remodeling at the personal level are providing enough juice to keep QXO et al. moving forward.

I could write about the most popular companies with the greatest number of followers, but what fun is that? I like to find a company early on that is changing not only its outlook but also the way we, as investors, view it. If you are like-minded, take a look at my analysis from a couple of days ago about the company nipping at Bloomberg's heels as a data provider -- it is none other than the up-and-coming hi-tech London Stock Exchange Group!

Comments

Log in or sign up to join the conversation.