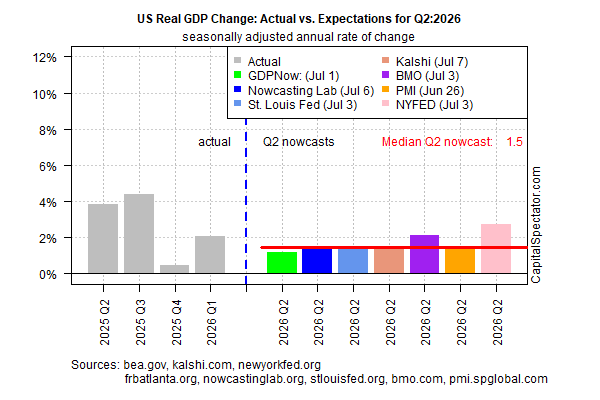

US economic growth estimates for the second quarter have weakened, according to recent nowcasts. The downturn suggests that output will slow in the upcoming Q2 GDP report, based on the median for a set of nowcasts compiled by The Capital Spectator.

Growth for Q2 is currently estimated at a sluggish 1.5% (real annualized rate). The new median nowcast marks a material slowdown from the 2.1% increase reported for Q1.

Today’s revised Q2 estimate marks a significant downshift from the 2.5% estimate in our previous update (June 22).

The softer nowcast reflects three factors in recent data: lower exports, a decline in expectations for consumer spending, and cooler forecasts for domestic investment. The combination of these changes has weighed on some nowcasts, including the Atlanta Fed’s GDPNow model, which is currently nowcasting Q2 growth at just 1.2% (July 1) — down sharply from 3%-plus a few weeks earlier.

But some economists say the downshift is less worrisome than it appears and is mostly an accounting-based adjustment rather than a genuine decline in economic activity. Renaissance Macro Research, citing the softer GDPNow estimate, last week noted:

We wouldn’t get too carried away with this. While Q2 GDPNow is lower, the bulk of the recent drop stems from a wider trade gap. Excluding net exports and inventory investment, private domestic demand is tracking close to 2.5 percent, which is respectable.

The strongest nowcast in the chart above is the New York Fed’s 2.74% estimate (July 3) — essentially unchanged in recent weeks and well above GDPNow’s 1.2%, the weakest of the group.

The government’s official Q2 report is scheduled for July 30, leaving the possibility that incoming data could revive the weaker estimates. As for The Capital Spectator’s view, our standard practice is to use the median as the best real‑time guesstimate.

If the optimists are right and Q2 activity is stronger than some nowcasts suggest, the median will move higher in the weeks ahead of the official data.

Comments

Log in or sign up to join the conversation.