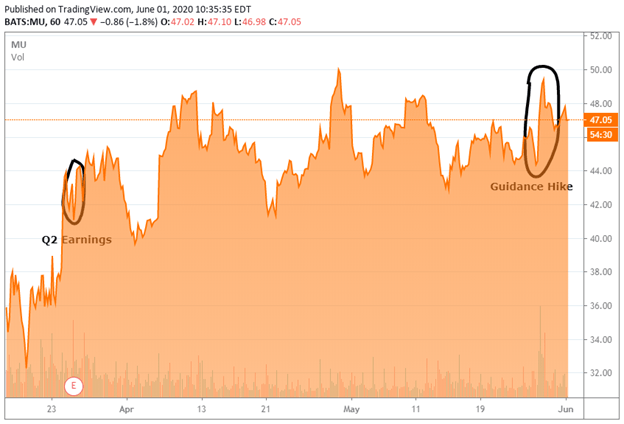

Last week, Micron (Nasdaq: MU) upped their guidance, which caused the stock to rally. We believe the company can have a nice run in the next couple of weeks, but there are potential risks, mainly related to Huawei. That keeps us from getting too bullish. Further, our model suggests there is a slight downside for 2021, so we don't have enough conviction to get big on Micron.

Recent Action

Source: Seeking Alpha - MU

In March, Micron reported earnings. We were neutral at the time, but still bought some in our model portfolio for subscribers. We wrote:

"With OEM customers stocking up with supply concerns that should boost Micron's business shorter term". "We expect the stock to be up on earnings".

Last week, the company upped guidance, causing the stock to pop. Given the positive news surrounding the stock at the moment, we think there can be some shorter term follow-through to the upside on the good news about pricing.

DRAM and NAND Pricing Trends

Micron's revenue comes from DRAM and NAND. According to their 10-Q, last quarter DRAM represented 64% of revenue, while NAND accounted for 32%. Since DRAM revenue is twice NAND's, we believe its pricing is the most important metric for the company's results. Earnings leverage is heavily influenced by pricing.

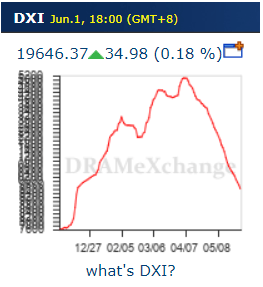

In the chart below, you can see that since April, spot pricing has been on a downtrend. Right now, the price is very similar to the one we saw at the end of 2019. Weak pricing could mean that the extra demand from inventory buildup is starting to fade, which, of course, wouldn't be good for Micron. It may be that, in the first few months of the year, OEMs rushed to secure inventory for the year, and once they secured it, demand fell. At least that's what the price trend would suggest. On top of that, if OEM's perception about their future sales change, that would also further impact pricing.

Source: DRAMeXchange

However, that chart tells us only about spot prices. Micron benefits from value-added products which are more advanced than the spot market. That's why the DXI can be down and Micron upped their guidance anyway. Their CEO was very positive on pricing last week at the 2020 Bernstein Strategic Decisions Conference. Regarding pricing, here's what CEO Sanjay Mehrotra said:

The demand, as I have shared with you, of course, has been impacted by the COVID environment. But certainly, the pricing compared to the assumptions we had baked into the guidance, has been more favorable in the industry. So, our -- the guidance that we just provided, the revised guidance that we have just provided for FQ3 really points to our continuing strong execution on the supply front compared to the conservatism we had built in the guidance at the time, as well as healthy pricing environment in the industry.

Those comments were bullish. It sounds like they were expecting a far more challenging environment with NAND and DRAM than what really happened.

Since DRAM is the largest source of revenue for Micron, its pricing affects how we think about the company. If spot prices started turning around, that would give us even more conviction on the stock.

Over a month ago, on April 30, Western Digital (Nasdaq: WDC) reported earnings and Executive VP & CFO Robert Eulau had similar upbeat tone regarding NAND pricing:

As we look into the fiscal fourth quarter demand for our flash-based solutions remains strong, and we anticipate that flash prices will rise on a sequential basis.

When taking both executives' comments, memory pricing is strong. Micron executives rarely speak about pricing which gives Mehrotra's comments more weight and is very positive.

China Tensions and Huawei Concerns

One of Micron's largest customers, Huawei, has a dark cloud over it at the moment. The tensions between the US and China could weigh on Micron's stock at some point this year.

In 2019, Huawei accounted for 12% of Micron's total revenue. Needless to say, Huawei is a very important customer for Micron. In May of last year, the U.S. Department of Commerce added Huawei to the list of companies that have limitations on the supply of certain US items and products. Micron managed to get a license that enabled them to sell products anyway not subject to the Export Administration regulations.

However, if tensions were to escalate, the license could be revoked and further measures against Huawei and China could be taken. If so, it's a risk for Micron.

Gaming Upside

Another important near-term driver CEO Sanjay Mehrotra talked about at the Bernstein conference is the demand coming from gaming consoles. He said:

So, new game consoles definitely have higher content. Certainly, higher DRM opportunity, as well as they're shifting from HDD to SSDs which bodes well for the overall industry as another growth driver for the NAND industry. So, yes, I mean, new game console is -- again, I think, the point is that there is need for more memory, more storage in the new applications, in the new game consoles, our GDDR6 memory is well positioned.

Since both the PlayStation 5 and the new Xbox One Series X are slated for release at the back end of the year, this should be a Micron catalyst.

Model and Price Target

Based on current business and doing some backing into the current guide (see full model: paywall), we couldn't get much upside to the stock price. Our projected EPS for 2021 are at around $5.00 per share. Using a PE ratio of 8.5, our current price target is $42, implying the stock is about fair value. We usually require large EPS upside for us to be bullish on any company, so we don't have medium-term conviction in MU at the moment, despite the positive pricing trends. But because of the near-term pricing benefits, we still think there could be some shorter-term upside.

Conclusion

As I mentioned before, the risk reward ratio for Micron is not very good at the moment. Our model suggests there is some downside for 2021, and the tensions between the US and China skew the risk reward ratio in an unfavorable way. However, given the recent hike in guidance as well as optimism regarding pricing, we believe the stock can see some gains in the short term.

Comments

Log in or sign up to join the conversation.