Market Analysis

After May’s 2019/20 major US and World new-crop supply/demand updates, the upcoming June 11 monthly balance sheet changes traditionally are modest. The USDA normally waits to see the upcoming June 28 US acreage & 3rd-quarter-grain stocks levels to help determine 2019’s crop sizes and old-crop feed demand during the 3rd quarter of the current crop years. However, 2019’s record slow planting paces prompted the USDA’s Chief Economist Johansson to state that the USDA would “use as much information as possible” to determine the current sizes of major crops in the upcoming June report.

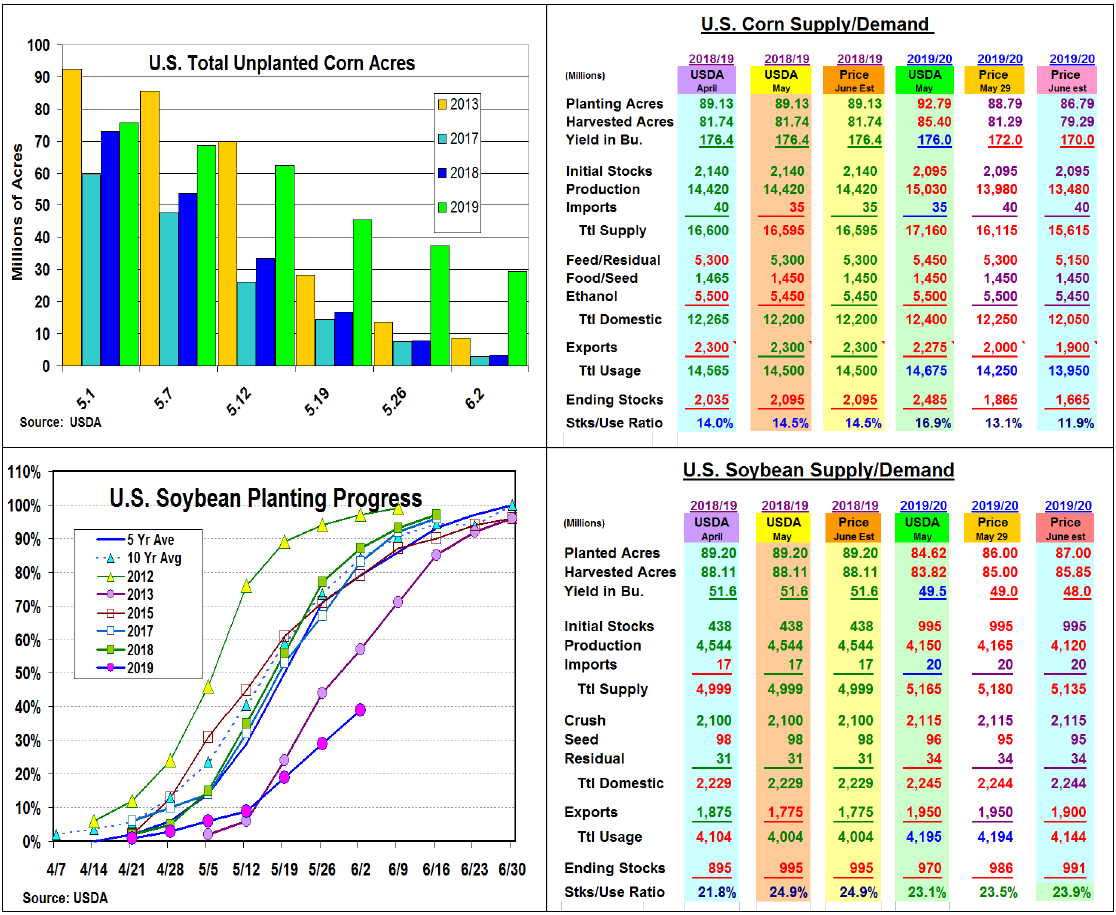

This will be a tough assignment. Only 67% of US corn was planted thru June 2. This leaves 29-30 million acres yet to plant vs the normal 2-4 million in early June & the 8.7 million unplanted in 2013. This suggests a possible 6 million or more cut in acres on next week’s report. Given the yield loss of late planted corn, the USDA may project a 13.5 billion bu. crop-based on 170 bu. US yield. No changes in old-crop corn demands are expected, but 2019’s reduced supplies & higher prices may slash 725 million from the USDA’s 2019/20 demand and cut stocks to 1.66 billion bu.

In soybeans, 2019’s saturated Midwest soils have also delayed plantings to just 39% by June 2. This leaves a record 53-55 million acres to plant. Producers decisions to either utilize corn’s prevent plant (PP) alternative in their insurance or a switch to beans will impact US seedings the most. Land & fertilizer costs suggest PP may be used more in the West while the East may look to beans. A potential of a 2.5 million rise in beans exists, but a reduced yield (1.5 bu.) may keep 2019’s output at 4.12 billion bu. Overall, minimal old-crop demand changes, but maybe a minor 2019/20 export loss will leave bean’s stocks below 1 billion bu.

S Plains yield losses may trim US W. Wheat output by 10 mil. bu. A late old-crop export surge & this minor crop loss may slice 2019/20 stocks. Black Sea still the big price factor.

(Click on image to enlarge)

What’s Ahead

A wide-open upcoming June crop report and indications of improving weather prospects could turn prices sluggish. Recent price strength to 2016 highs in corn & near $9 for spot beans should have cut old-crop supplies to gamble levels (10%) at this time. The producer should have 25-30% of a conservative 2019 corn and bean output sold in the $4.38-$4.48 and $9.00-$9.15 ranges if you have seeds planted.

Comments

Log in or sign up to join the conversation.