Market Analysis

The US planting intentions got the trade’s initial attention last week after 2019’s producer survey showed corn plantings higher and soybean lower than the trade ideas. The USDA won’t utilize this planting data until its first 2019/20 US and World supply/demand outlooks are released on May 10. Its importance, however, justifies a balance sheet creation utilizing Ag Forum trends. The latest quarterly stocks data—plus our domestic processing and US export trends —were utilized to determine if April 9 US old-crop corn, wheat & soybean balance sheets need changes.

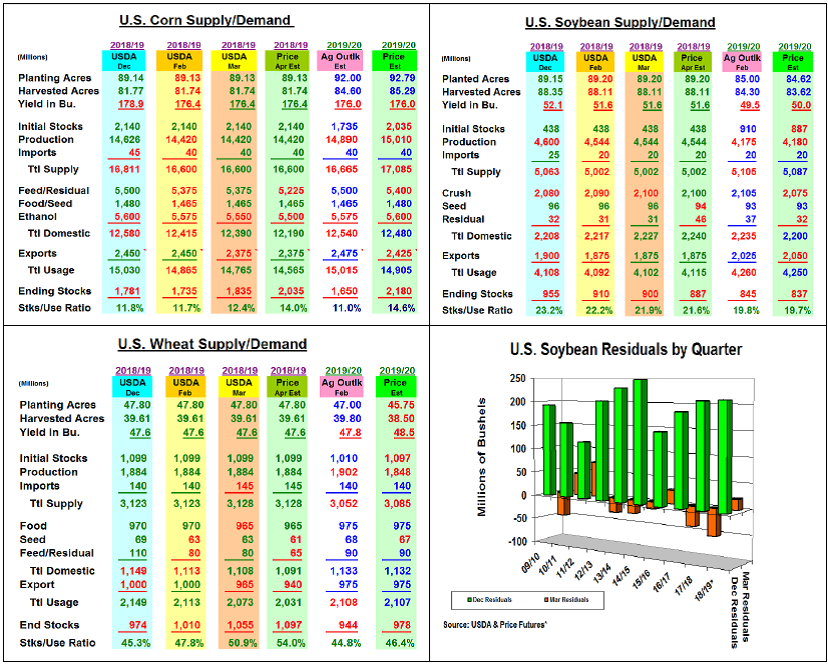

As previously reported, corn’s March 1 stocks were 270 million bu. above expectations. This suggests a possible underestimate of 2018 harvest has occurred. This will be handled as a reduction in corn’s feed & residual demand by a likely 150 million bu. cut in this usage to 5.225 billion. This week’s February US ethanol corn grind was 408 million bu. bringing this year’s 2nd quarter demand to 1.308 billion bu. Weather & low gas prices sliced this bio-fuel demand by 90 million bu. vs. last year, prompting a 50 million bu. 18/19 ethanol drop this month. US export sales are slightly behind their seasonal pace, but this year’s shipments are at their 5-year pace so no change in exports is expected. April’s corn carryover will likely rise 200 million bu. to 2.035 billion. This stock rise and Friday’s 1.46 million higher 2019 US plantings than expected could advance the USDA’s new crop corn carryover to over 2.1 billion bu. next month.

Wheat’s March stocks suggest a 15 million cut in feed demand. Even with a seasonal up in humanitarian aid, this crop’s exports may be cut 25 million & stocks up 42 million.

Soybeans’ 21 million bu. rise in 2nd quarter residual dis-appearance suggests old crop might be overestimated prompting a residual jump this month. With US crush 49 million ahead of last year and recent export sales picking up sharply, no crush or export changes are expected.

(Click on image to enlarge)

What’s Ahead

With US/China trade talks ongoing and the Midwest forecast not encouraging for planting in the next few weeks, prices have rebounded from last week’s reports. However, the latest March’s quarterly stocks suggest more corn & wheat ending stocks limiting price potential unless 2019’s plantings are extended into May. Use May $3.68-.72 range in corn & $4.75-.80 range in wheat to have 70% & 80% sold in each.

Comments

Log in or sign up to join the conversation.