Market Analysis

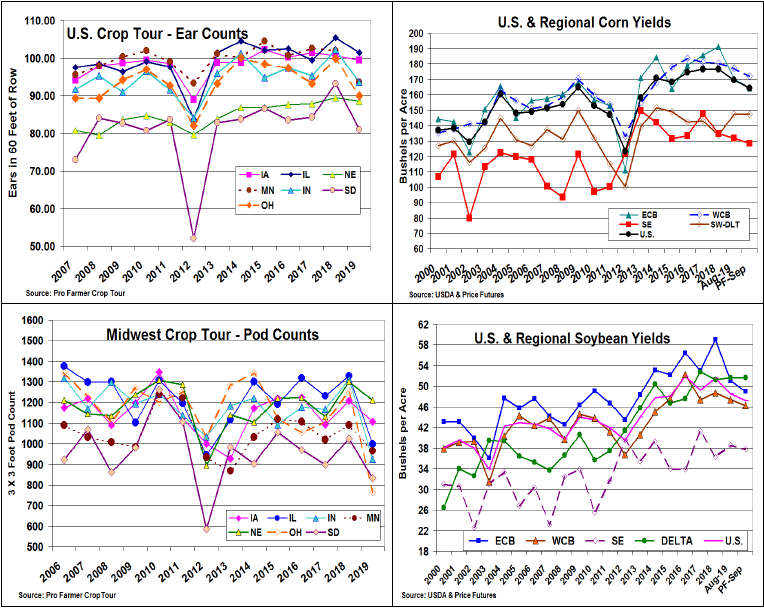

The expectations for the upcoming September 12 US corn and soybean crop production reports have become muddled given the current strains in the US/China trade talks. However, the potential for smaller crops began during last month’s Pro Farmer Crop Tour. The group’s cornfield checks didn’t seem to support the USDA’s 169.5 bu. yield estimate while soybeans 20% average drop in pod counts across the tour’s 7 states vs. the USDA’s 6% yearly drop in yield raised some eyebrows.

In corn, 2019’s tour field checks seem to verify the USDA’s August yields in 4 states (IA, NE, OH & IN). However, IL, MN and SD’s state adjusted tour yields of 173, 161, & 149 because of the tour sampling a higher portion of these states better yielding fields don’t seem to match the USDA’s 181, 173 & 157 state yields. Because of these past historical tour relationships, no enumerator plot data (ear counts) and some Central US dryness occurring during August, this month’s Midwest yields could drop by 6.3 bu. in ECB & 5.1 bu. in WCB. Only modest (SE) to no (SW-DLT) yield changes are expected. Over-all, the US corn yield could decline to 164.4 bu. With no change in harvested area, 2019’s corn output could be 13.48 billion bu. Some sluggish old crop demand (-75 million bu.) adds to beginning stocks, but 2019/20’s end-ing could slip to 1.835 billion bu. this month.

In soybeans, 2019’s hefty tour drop in pods counts be-cause this year’s late seeding & cool temperatures slow-ing crop development should cut US bean yields. Some last half August rains may boost seed size, but adding many more pods to up the US bean yield seems limited. Because of beans’ adaptability, our Sept yield est. is 47.2 bu. vs. Aug’s 48.5 bu. However, this fall’s growing season length (normal freeze dates could impact yields) keeps 2019/20’s output fluid vs. our 3.58 billion bu. crop. Late exports/crush bumps may cut 55 mil bu O/C stocks.

(Click on image to enlarge)

What’s Ahead

This year’s late seedings & below-average temperatures in the WCB and the Plains reducing 2019’s growing degree days and maturity leaves both US corn & bean crops vulnerable to weather for the next 6-7 weeks. This situation keeps output open, but we don’t need bad trade news to cloud the skies. No US wheat update until the 9.30 Small Grain Report. The market’s eye will be on the Central US early morning temps.

Comments

Log in or sign up to join the conversation.