Market Analysis

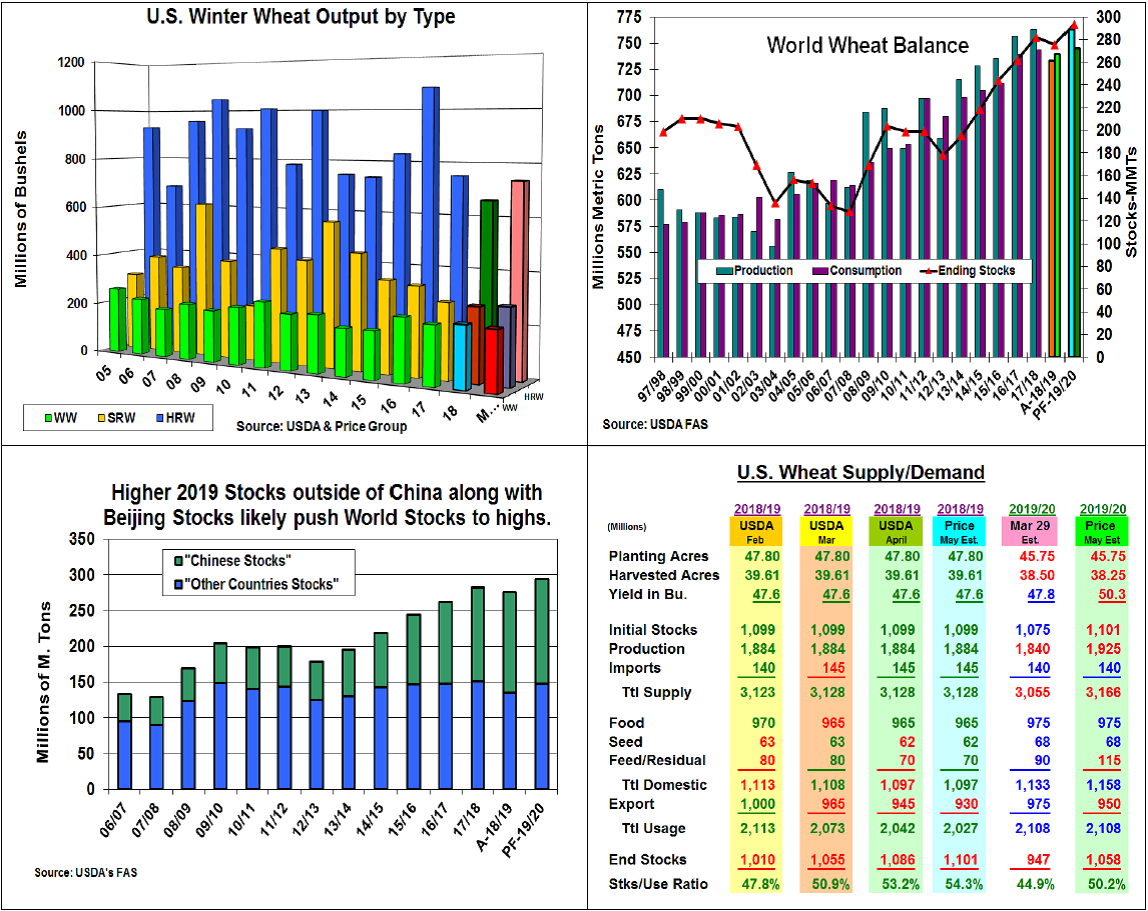

This year’s dramatic jump in rainfall across the US Plains prompted the trade to focus on last week’s 3-day annual Kansas wheat tour. The first day covered northern Kansas. Despite cold temperatures reducing plant growth, the tour’s field counts were strong projecting a 46.9 bu. yield vs. the region’s 5-year average of 39.5 bu. average. In Colby, groups from CO and NE also reported strong state yields of 46.5 and 44 bu. The Kansas crop scouts then traveled south into SW Kansas and then eastward to Wichita. Similar to the first day, improved moisture boosted the SW’s average yield to 47.6 bu. vs. the past 5-year‘s 39.3 average. In Wichita, an OK group also reported a large state jump in 2019’s yield to 37.4 bu. vs. last year’s 28 bu. average. The KS group returned to Manhattan to issue its overall state yield of 47.2 bu. vs. the 5-year Kansas yield of 40.2 bu. 2019’s 700,000 drop in Kansas seedings and hard red’s 1.031 million less plantings will temper this variety’s size advance to 737 million bu. vs. 2018’s 662 million. We expect soft red wheat’s output to be up slightly to 293 million while PNW’s white wheat maybe off slightly to 230 million bu. Overall, a 1.26 billion bu. winter crop and total US wheat output of 1.925 billion will be used in 2019/20’s S&Ds.

After last year’s first pullback in world wheat output in five years, a rebound to 2017/18’s 763 mmt of supply seems possible. Sharp recoveries in EU and Russian crops and slightly larger US, Canadian, Indian and Australian crops are behind this bounce back. Even with a 1% increase in world demand, wheat’s stocks are likely to expand to 292 mmt, a new record. The USDA will separate China’s stocks out of the world’s balance sheet to help clarify the actual tradable supplies being available, This will show that a sizable portion of world’s stocks remain outside wheat’s tradable supplies, but this year’s stock rise will likely be in exporting countries, too.

(Click on image to enlarge)

What’s Ahead

With US export shipments faltering, 2018/19’s ending stocks could be raised by 15-20 million bu to 1.101 billion on May 10. This year’s stronger US winter wheat crop will keep ending stocks high even if low prices promote stronger feed demand while the Black Sea battles for our exports. Time to clean out old-crop bushels, but hold new–crop sales for production scare in the world.

Comments

Log in or sign up to join the conversation.